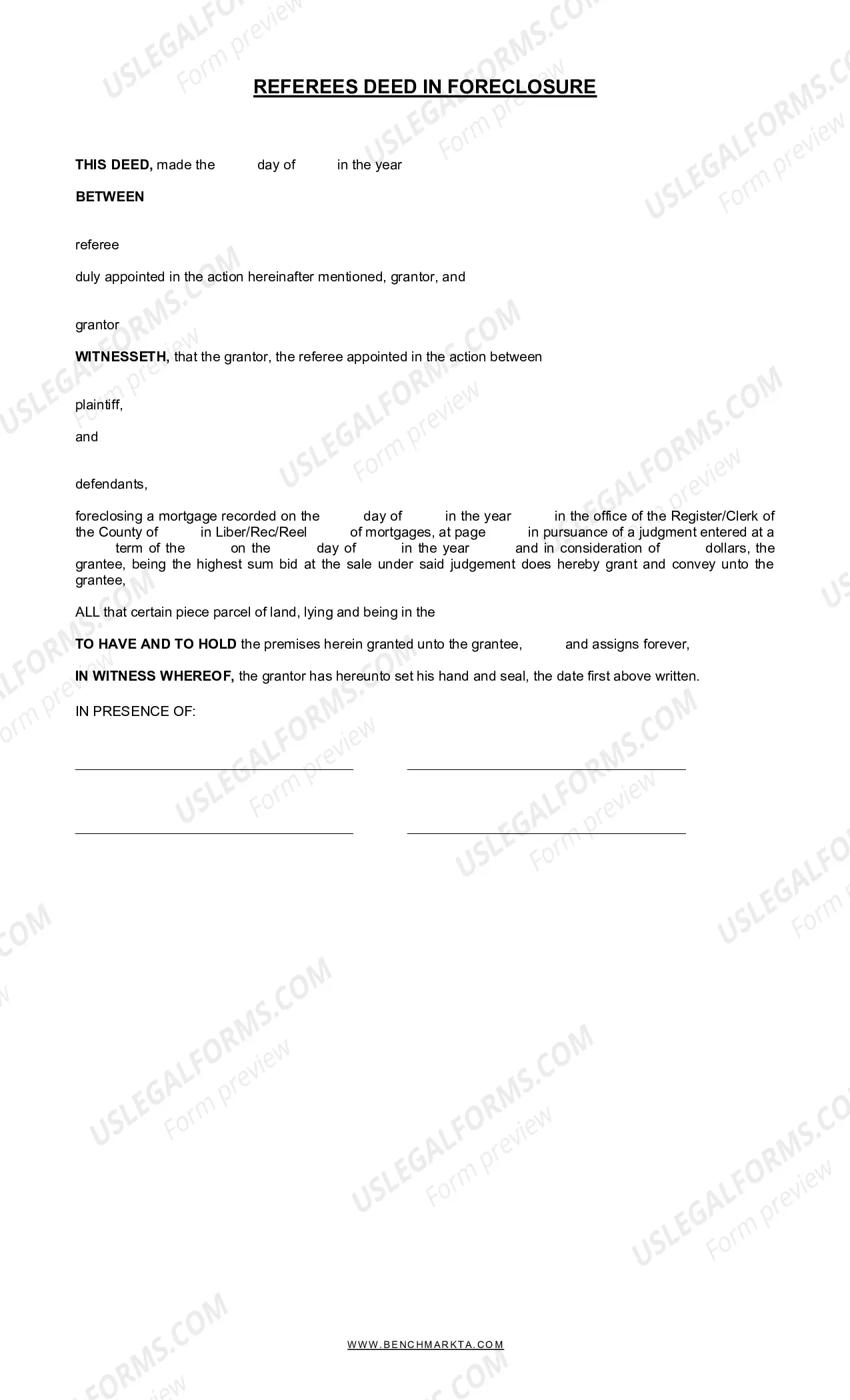

New York Referee's Deed in Foreclosure

Overview of this form

The Referee's Deed in Foreclosure is a legal document used to transfer property ownership when a foreclosure sale takes place. This form is specifically designed to reflect the completion of a foreclosure process, facilitating the formal transfer of property from the debtor to the highest bidder at the foreclosure sale. Unlike other deeds, this deed applies exclusively to properties involved in foreclosure proceedings, ensuring clarity and legal compliance in property transfers due to default on mortgage obligations.

Key parts of this document

- Date of execution: Specifies when the deed is officially signed and executed.

- Parties involved: Identifies the referee (grantor) and the grantee (new property owner).

- Details of the foreclosure action: Includes information about the plaintiffs, defendants, and the mortgage being foreclosed.

- Consideration amount: States the price the grantee has paid for the property.

- Property description: Provides a legal description of the property being transferred.

- Signatures and notary acknowledgment: Required to validate the deed and its compliance with legal standards.

Situations where this form applies

This form is typically used during the completion of a foreclosure process. You should utilize the Referee's Deed in Foreclosure if you are the referee appointed by the court to oversee the sale of a foreclosed property, or if you are the highest bidder who has won the property at the foreclosure auction. It solidifies the legal transfer of ownership and is necessary for updating public records.

Who this form is for

- Referees appointed by the court in foreclosure actions.

- Bidders who successfully purchase property at a foreclosure auction.

- Legal professionals facilitating property transfers related to foreclosure sales.

- Anyone involved in the foreclosure process needing to document the transfer of ownership.

How to complete this form

- Identify the date when the deed will be executed.

- Fill in the names and addresses of the grantor (referee) and grantee (new owner).

- Insert the details of the foreclosure case, including the names of plaintiffs, defendants, and mortgage details.

- Specify the amount paid by the grantee as consideration for the property.

- Provide a thorough description of the property, including the address and legal description.

- Have the grantor and a notary public sign the document to validate its legality.

Does this form need to be notarized?

Yes, this form must be notarized to be legally valid. It requires signatures from both the grantor and a notary public to ensure proper authentication and compliance with state laws. US Legal Forms offers integrated online notarization, making it easy to complete the process securely and conveniently through a video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all necessary parties involved in the foreclosure action.

- Leaving the consideration amount blank or incorrect.

- Not providing a complete and precise property description.

- Omitting signatures or acknowledgments from the notary public.

- Incorrectly filling in dates, which can lead to legal issues.

Benefits of completing this form online

- Easy accessibility: Download and complete the form from anywhere, anytime.

- Customizable: Tailor the form to fit your specific circumstances.

- Reliability: Ensure compliance with legal requirements with professionally drafted templates.

- Convenience: Save time with a straightforward process to generate legally binding documents.

Legal use & context

- This deed serves as official proof of the transfer of ownership post-foreclosure.

- It must be filed with the appropriate county clerkâs office to be enforceable.

- Proper completion and notarization are crucial for legal recognition.

What to keep in mind

- The Referee's Deed in Foreclosure is essential for documenting property transfer after foreclosure.

- Ensure all parties understand their roles in completing this deed.

- Notarization is a required step before the deed can be recorded.

Looking for another form?

Form popularity

FAQ

If the court grants summary judgment in favor of the bank, typically after a hearing, the bank wins the case, and your home will be sold at a foreclosure sale.order the foreclosure sale, or. dismiss the case, usually without prejudice. (Without prejudice means the bank can refile the foreclosure.)

In a non-judicial foreclosure, the lender is proceeding on the basis that the mortgage or deed of trust provides for its right of foreclosure. This means that your lawsuit will ask the judge to stop the foreclosure proceeding until they can review your argument against the foreclosure.

The Referee is an individual, usually an attorney, who has been appointed by the Court to conduct the auction and transfer the property after a judgment of foreclosure has been obtained by the lender, who is the plaintiff in the foreclosure lawsuit.

If the court grants summary judgment in favor of the bank, typically after a hearing, the bank wins the case, and your home will be sold at a foreclosure sale. If the court denies the bank's motion for summary judgment, though, litigation will continue, including discovery and trial.

The term used for the direction of a court to appoint a refer in order to decide a case.

Once a foreclosure case has successfully been through court proceedings, a judge signs the final judgement. This provides the lender with the legal right to sell the property to regain any losses accrued from nonpayment.

The referee is a judicial officer whose job is to be fair, diligent, and essentially act as an auctioneer in the process of selling the real estate. All of the referee's powers will be exercised under the supervision of the court and with full opportunity for the owners to be heard during the process.

In rare circumstances, you can get a court to set aside (invalidate) a foreclosure sale. Sometimes homeowners aren't aware that a foreclosure sale has been scheduled until after it's already been completed. Even if your home has been sold, you might, in rare circumstances, be able to invalidate the sale.