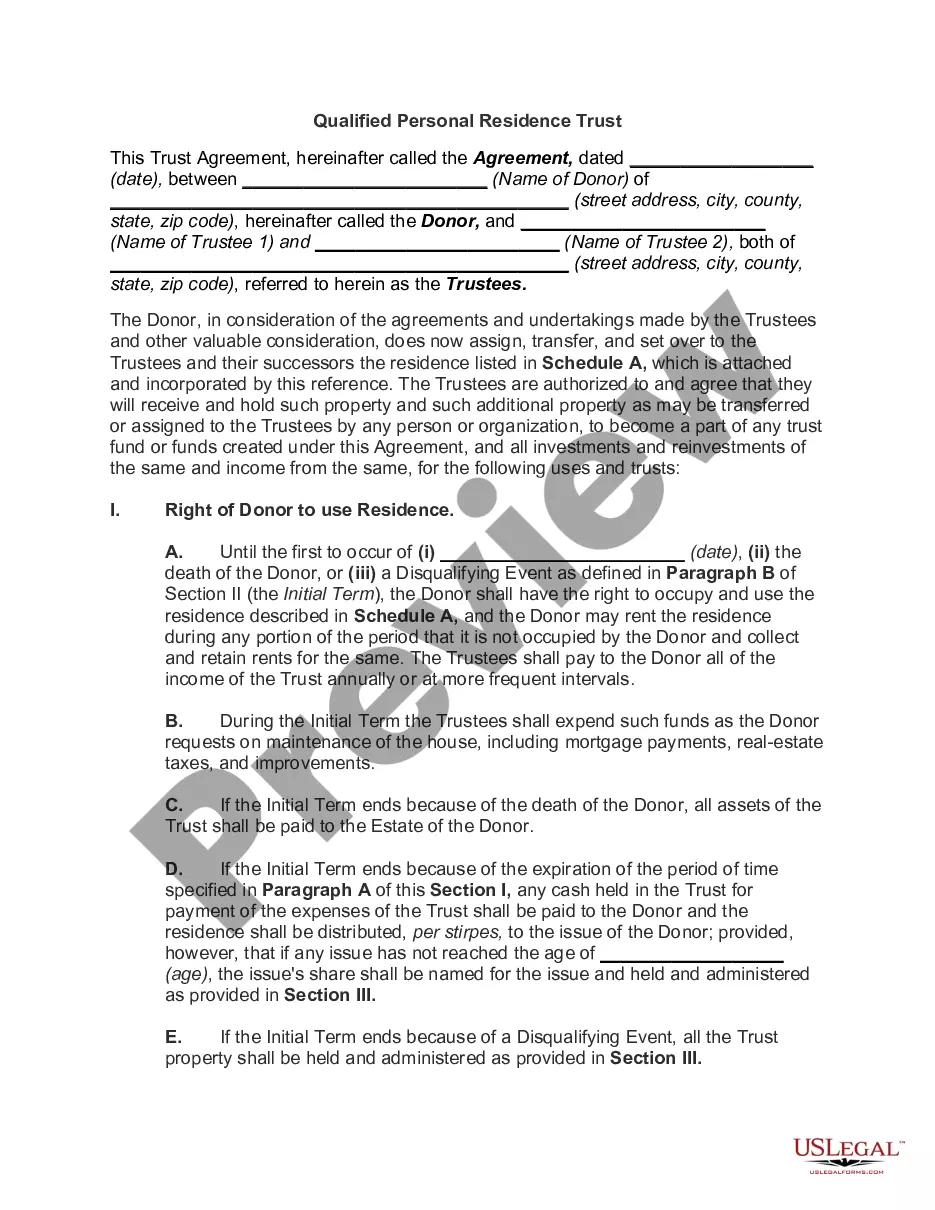

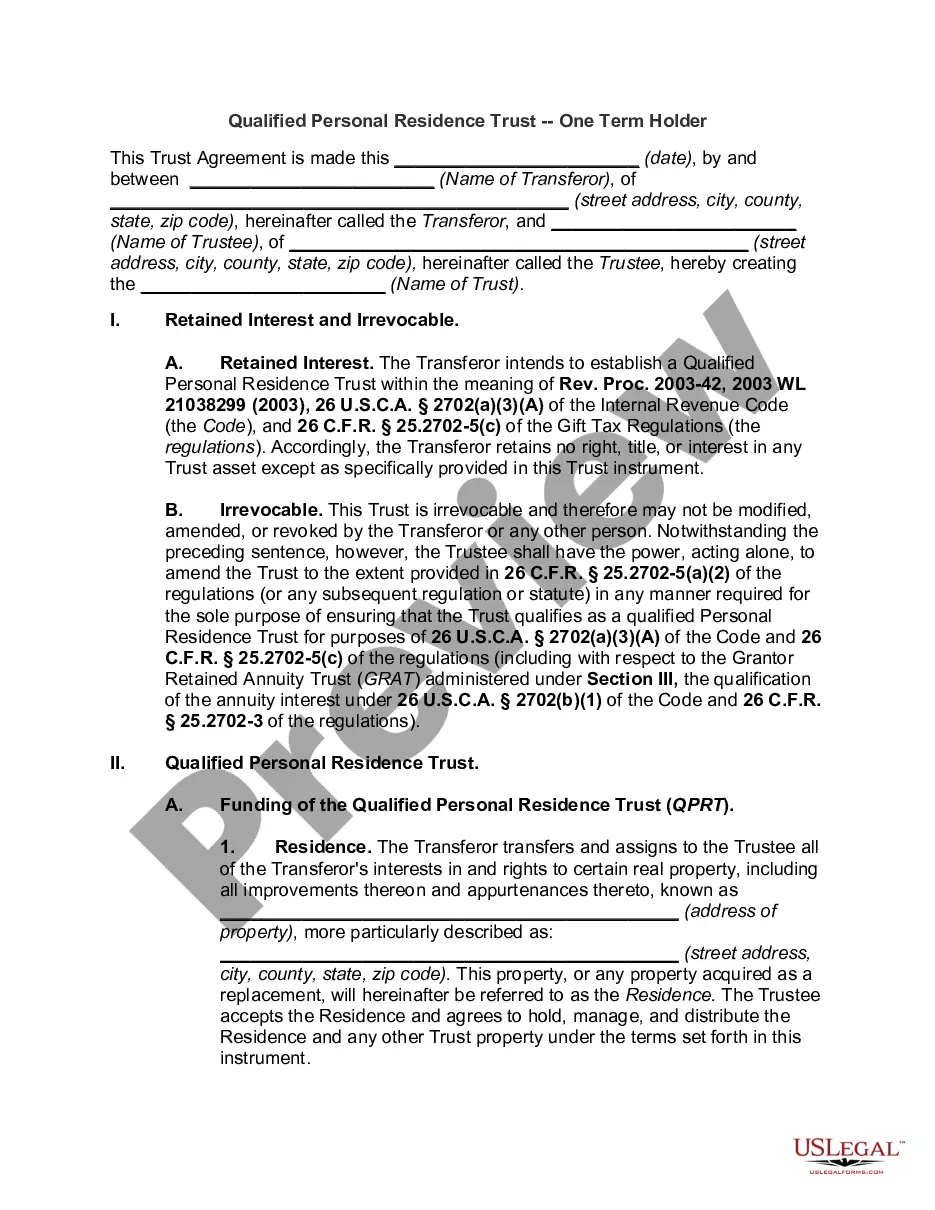

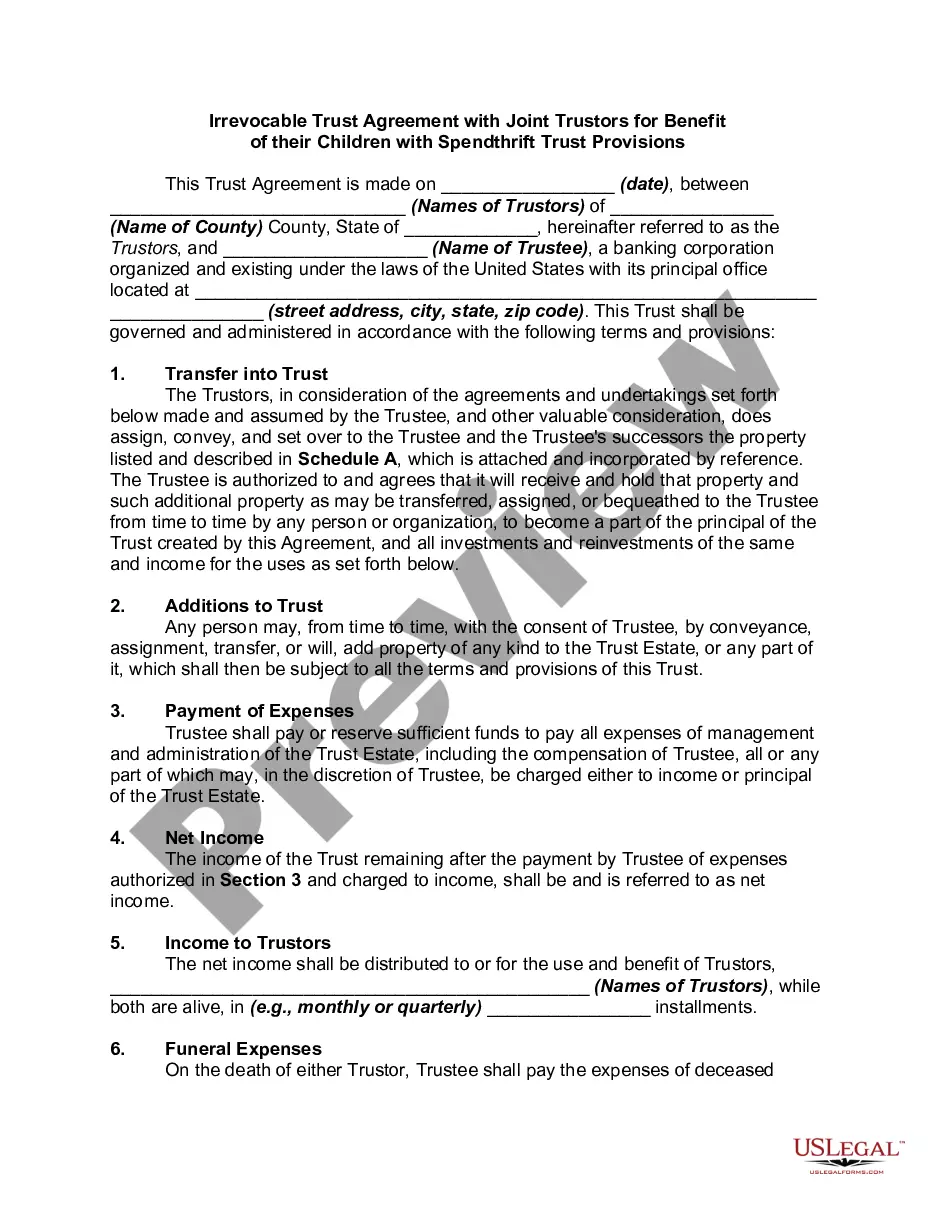

Personal Residence Real Withdrawal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Personal Residence Trust?

It is well-known that becoming a legal professional does not happen instantly, and you cannot learn to efficiently draft a Personal Residence Real Withdrawal without possessing a unique skill set.

The process of creating legal documents demands extensive training and expertise.

So why not entrust the creation of the Personal Residence Real Withdrawal to experts.

You can view it (if this option is available) and read the accompanying description to confirm whether the Personal Residence Real Withdrawal is what you seek.

If you need a different form, you can restart your search.

- With US Legal Forms, one of the largest libraries of legal templates, you can locate anything from court papers to templates for office correspondence.

- We understand the significance of compliance with federal and state regulations.

- That’s why, on our platform, all documents are tailored to specific locations and are current.

- Let’s get started with our platform and obtain the form you need in just a few minutes.

- Find the form you require using the search functionality at the top of the page.

Form popularity

FAQ

Generally, you do not have to report the sale of your primary residence to the IRS if you meet certain criteria, specifically if you qualify for the capital gains exclusion. You can exclude up to $250,000 of gain for single individuals and $500,000 for married couples filing jointly. However, if your gain exceeds these limits, or if you do not meet the residency requirements, you will need to report the sale and the associated tax implications. For a smoother process, consider using uslegalforms to access tailored legal resources related to personal residence real withdrawal.

To prove residency and avoid capital gains taxes on the sale of your home, you should gather documentation that shows you lived there as your primary residence for at least two of the last five years. This can include utility bills, voter registration, and tax records. It is essential to keep all records organized and accurate, as these will support your claim when seeking a personal residence real withdrawal benefit. Using a reliable platform like uslegalforms can help you access the necessary forms and guides to ensure you meet all requirements.

To rescind your principal residence in Michigan, you need to submit a request to your local assessor's office. This typically involves completing specific forms and providing necessary documentation. It's essential to follow local guidelines to ensure a smooth process. If you need help, platforms like uslegalforms can provide the templates and assistance required for your request.

Yes, you can withdraw from your 401k as a hardship withdrawal for your primary residence. This is especially useful if you face financial challenges that threaten your home. Check with your plan administrator to ensure that this option is available for you. Utilizing the personal residence real withdrawal can give you the financial support you need to stay in your home.

A 401k hardship withdrawal is permitted under specific circumstances. Common acceptable reasons include medical expenses, purchasing a primary residence, paying for tuition, and preventing eviction or foreclosure. Each plan may have its own rules, so reviewing your plan details is important. Remember, the personal residence real withdrawal option can help you secure your home.

To qualify for the personal residence exclusion, you must meet specific ownership and residency criteria. This includes owning the home for at least two years and using it as your primary residence for the same duration. If you think you may qualify and want to explore your options in depth, the user-friendly services at uslegalforms can assist you in understanding how personal residence real withdrawal fits into your financial strategy.

To avoid capital gains tax on the sale of your home, you must live in the house as your primary residence for at least two of the five years preceding the sale. This residency period qualifies you for the personal residence exclusion, which can significantly reduce or eliminate taxes on your profit. By understanding this timeline, you can effectively plan your real estate decisions while leveraging personal residence real withdrawal options.

The personal residence gain exclusion rule allows homeowners to exclude certain capital gains from taxes when selling their home. To use this exclusion, you need to meet the ownership and residency requirements, as outlined earlier. This rule serves as a financial advantage for homeowners looking to manage their profits effectively, especially regarding personal residence real withdrawal situations.

Buying a house can qualify as a hardship withdrawal, but it depends on your specific financial circumstances and the type of retirement account involved. Generally, hardship withdrawals allow you to access funds for immediate and pressing financial needs, such as purchasing a primary residence. If you need assistance navigating these options for personal residence real withdrawal, consider exploring the resources available at uslegalforms.

You can use the personal residence exclusion multiple times in your lifetime, but there are specific conditions. You must have owned and lived in the property for the required timeframe each time you claim the exclusion. Furthermore, the last use of this exclusion must be at least two years apart from your previous claim, promoting fair use of the personal residence real withdrawal benefits.