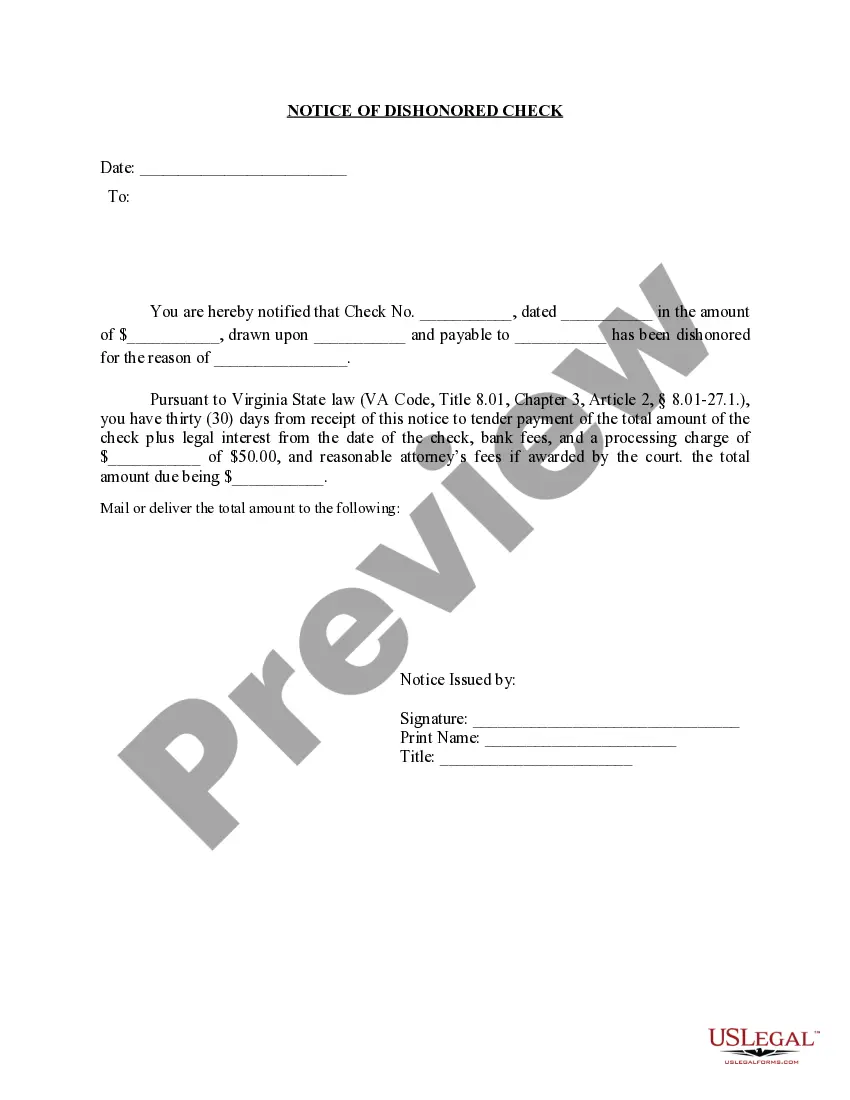

Virginia Notice of Dishonored Check - Criminal - Keywords: bad check, bounced check

Understanding this form

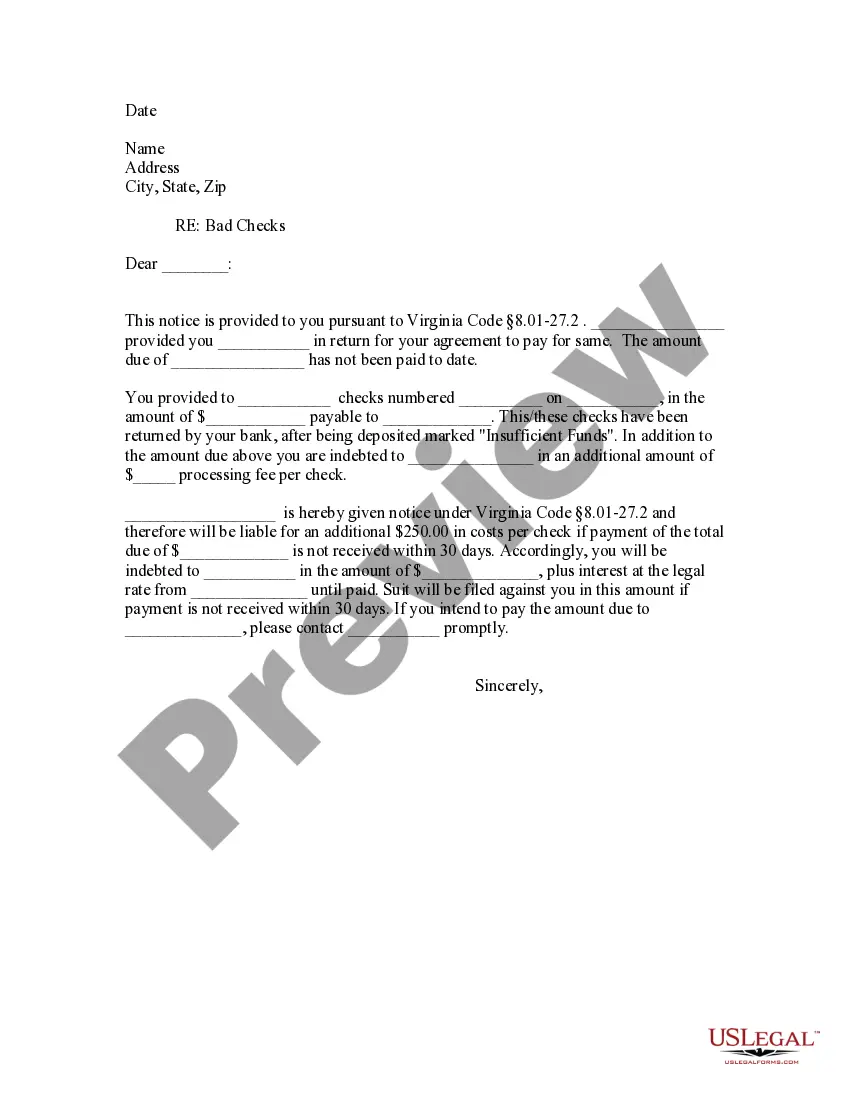

The Notice of Dishonored Check - Criminal is a legal form used to formally notify a debtor that their check has been dishonored, commonly referred to as a bad check or bounced check. This form is essential for initiating legal action and ensures the creditor adheres to state laws regarding the collection of debts associated with dishonored checks. It is specifically distinct from other debt recovery forms as it focuses on checks that have not cleared due to insufficient funds or a non-existent account.

Key parts of this document

- Creditor's information: Name and contact details of the individual or business owed money.

- Debtor's information: Name and contact details of the individual or entity who issued the check.

- Check details: The amount, date, and check number of the dishonored check.

- Notification statement: A declaration indicating that the check has not been honored and the debt remains unpaid.

- Signature line: Space for the creditor or their representative to sign the notice.

When this form is needed

This form should be used when a check has been returned unpaid by a bank, either due to insufficient funds or because the account does not exist. It is typically utilized by businesses or individuals who have received a bad check and need to inform the payer of the dishonored status in order to seek resolution and possible recovery of the funds owed.

Intended users of this form

- Business owners who have received a bad check from a customer.

- Individuals expecting payment for services rendered, who have been issued a bounced check.

- Anyone seeking to document the dishonor of a check for legal purposes.

- Creditors attempting to recover debts after a check has been dishonored.

Steps to complete this form

- Fill in the creditor's information, including name and address.

- Enter the debtor's information, including name and address.

- Provide details of the dishonored check, including the amount, date, and check number.

- State the reason for dishonor, confirming the check was not paid.

- Sign and date the form to validate the notification.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, it is advisable to verify your stateâs specific requirements regarding debt recovery documentation.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to provide complete and accurate information regarding the check and the debtor.

- Not signing the document before sending it, which can invalidate the notice.

- Using incorrect terminology or failing to specify the reason for the dishonor.

- Not keeping a copy of the notice for personal records.

Why use this form online

- Convenient access to an accurate and legally vetted form.

- Easy customization to fit specific situations and debtor details.

- Faster completion and submission process compared to traditional methods.

- Immediate download prevents delays in notifying the debtor.

Legal use & context

- This notice serves as a formal communication and is often a prerequisite for further legal action.

- Failure to send this notice may hinder your ability to recover funds through legal channels.

Main things to remember

- The Notice of Dishonored Check is crucial for recovering funds from bounced checks.

- It serves to formally inform the issuer and can pave the way for legal action if necessary.

- Ensure compliance with state-specific laws for effective enforcement.

Looking for another form?

Form popularity

FAQ

A stop payment on a check is when you ask your bank to cancel a check before it is processed. After you request a stop payment, the bank will flag the check you specified, and if anyone tries to cash it or deposit it, they'll be rejected.

A stop payment on a check is when you ask your bank to cancel a check before it is processed. After you request a stop payment, the bank will flag the check you specified, and if anyone tries to cash it or deposit it, they'll be rejected.

Give your bank a "stop payment order" Even if you have not revoked your authorization with the company, you can stop an automatic payment from being charged to your account by giving your bank a "stop payment order" . This instructs your bank to stop allowing the company to take payments from your account.

Some merchants may need to have the transaction go through and refund you, anyway. Failing that, you'll need to wait for the transaction to go through and try to lodge a dispute - if you're able to - in order to reclaim the funds. You can not stop the pending debit card transaction.

Payment history is the most important ingredient in credit scoring, and even one missed payment can have a negative impact on your score.Payment history accounts for 35% of your FICO®Score2609 , the credit score used by most lenders.

A stop payment is a request for a bank to stop a check or recurring debit payment that's waiting to be processed. Stop payment requests can only be made by the account holder who sent the original payment, and must be made before the check or payment has been processed.

The first is that stopping payments on your account only makes things worse. It starts a process that can put you deeper in debt, wreck your credit, cause you more stress and negatively affect you for years to come.

Depending on the bank, stop payment orders typically expire after six to 12 months, although many banks allow you to renew a stop payment order if the check is still outstanding. If your bank charges a stopped check fee, they may also charge a fee to renew the stop payment order.

A pending transaction can only be cancelled if the merchant provides us with a pre-authorisation release confirming they have no intention to debit the restricted funds.If you believe a pending transaction is unauthorised, once the funds have debited from your account, we can help you dispute the transaction.