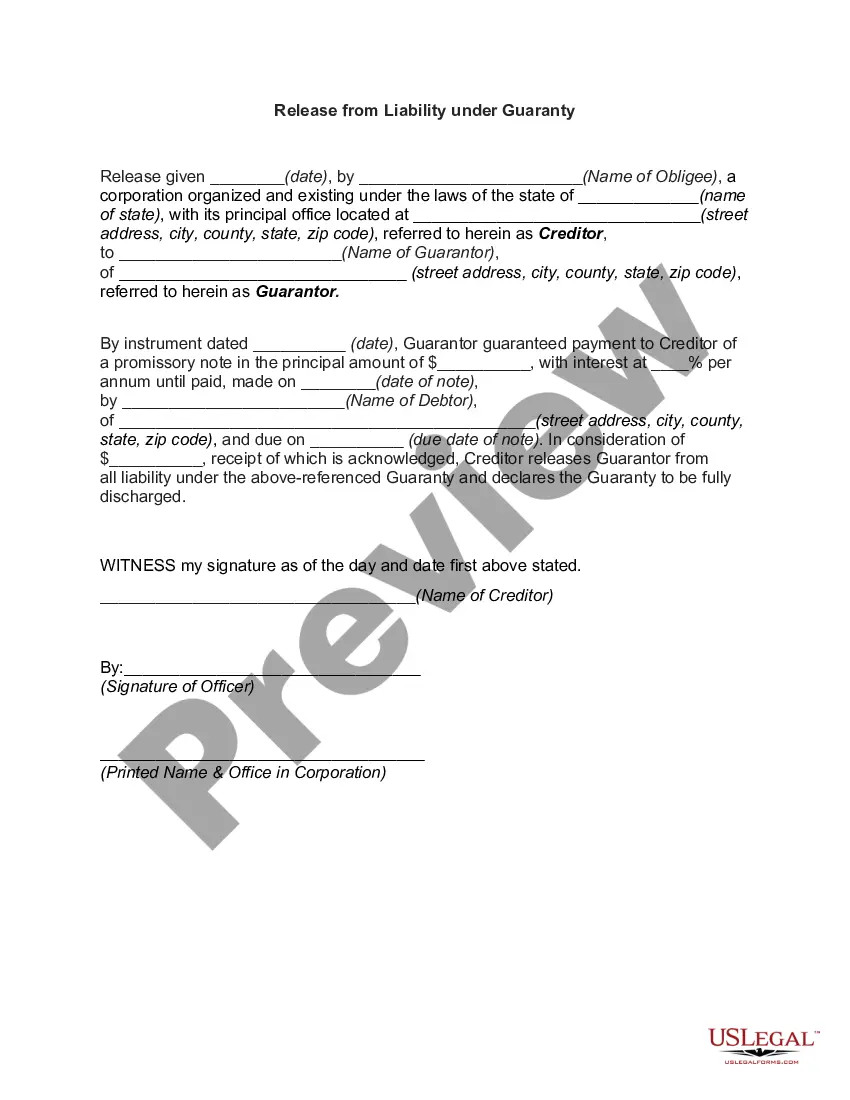

Guarantor Waiver Which Avoids Release of Guarantor by Reason of the Tenant Discharge Release or Bankruptcy

About this form

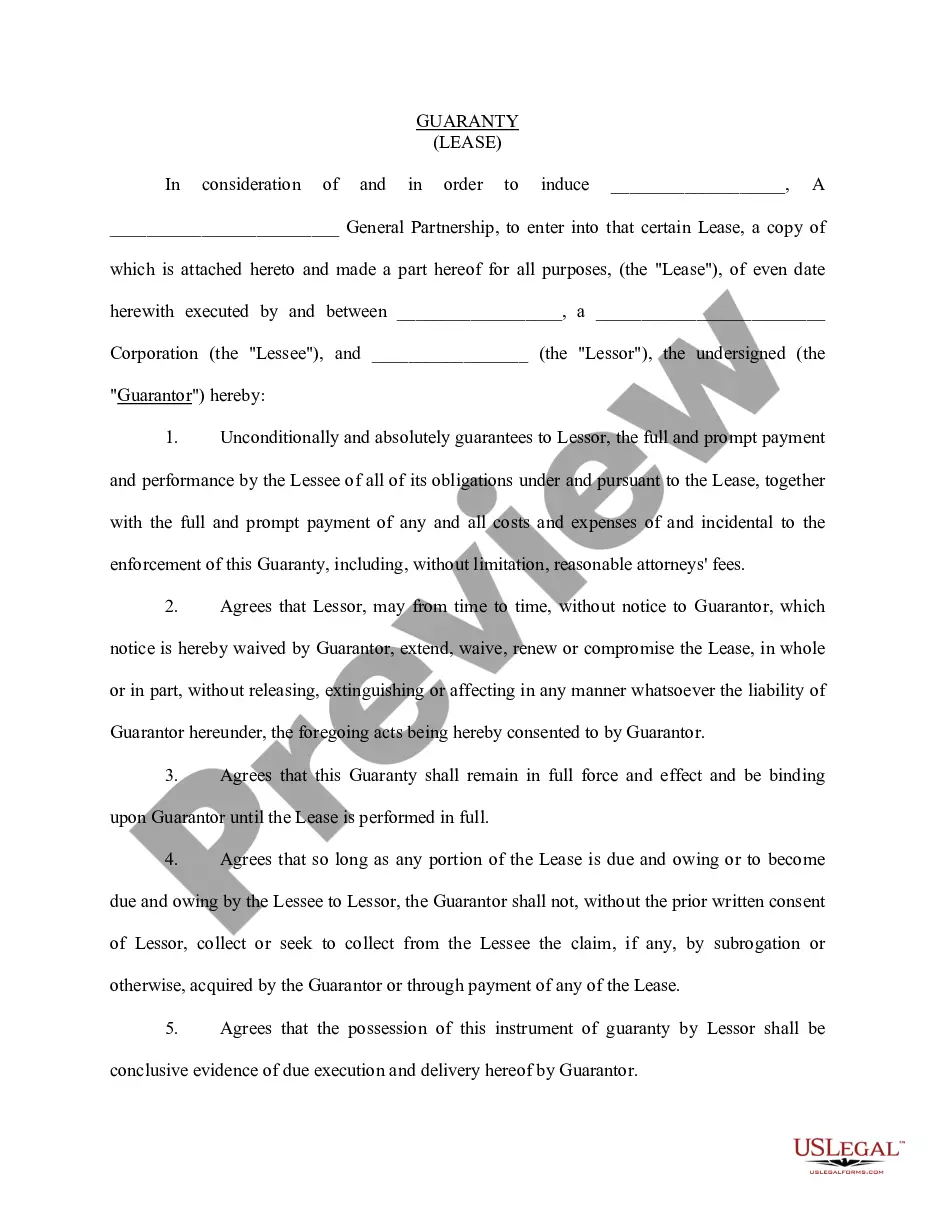

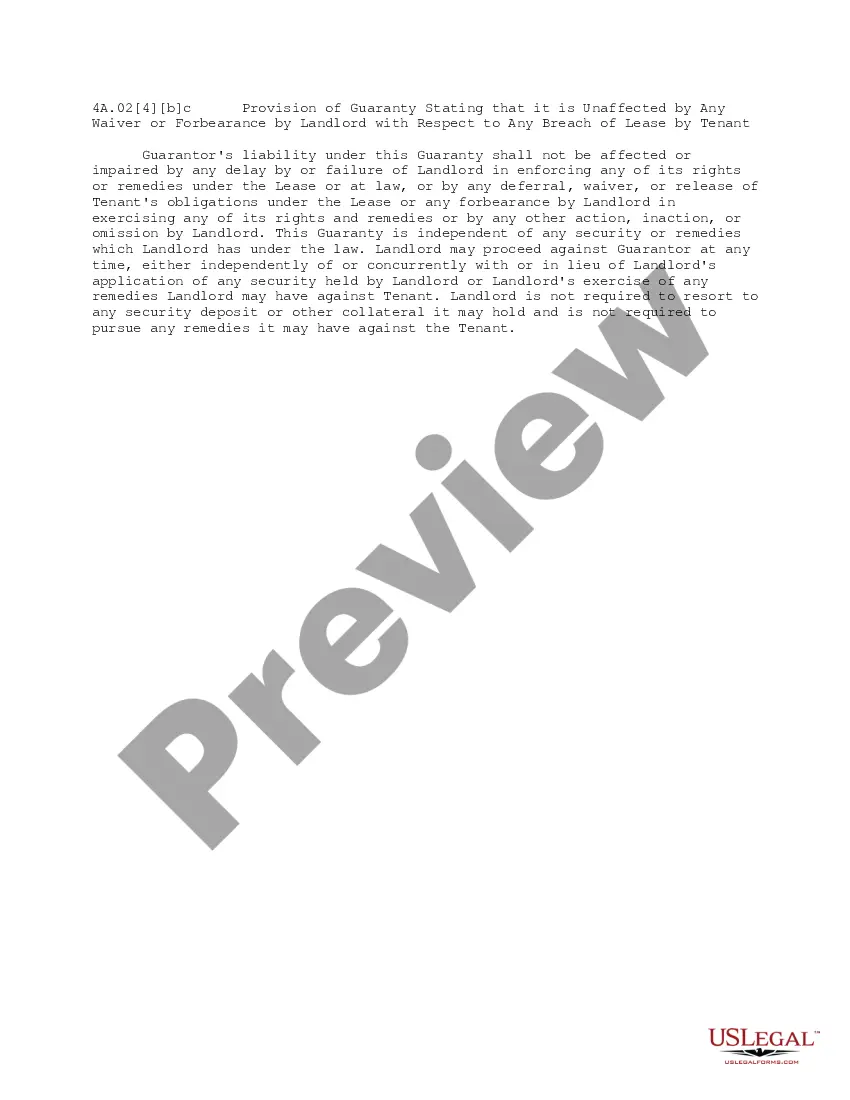

The Guarantor Waiver is a legal document that ensures a guarantor's obligations remain intact even if the tenant is discharged or released due to bankruptcy or other insolvency situations. Unlike standard lease agreements, this form explicitly protects the guarantor's liability, avoiding release based on the tenant's financial issues. This allows landlords to maintain a level of security when the tenant faces financial difficulties.

Key components of this form

- Clear statement that the guarantor's obligations are unaffected by tenant discharge or bankruptcy.

- Details on insolvency proceedings and the implications for payment obligations.

- Conditions under which the guarantor must reinstate obligations if payments are disgorged.

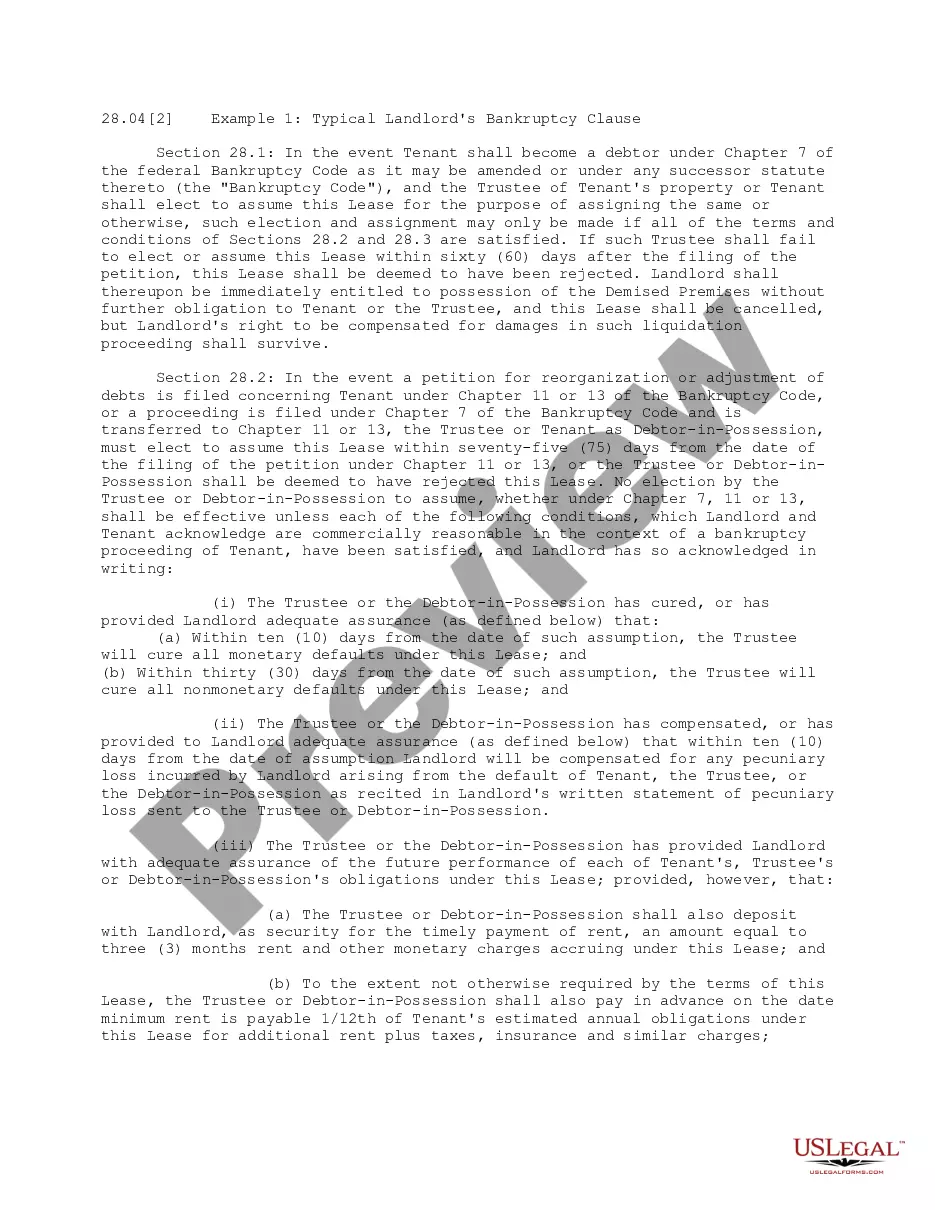

- Provisions related to lease rejection or disaffirmation in bankruptcy contexts.

When to use this form

This form is essential when a landlord wants to secure the guarantor's commitments despite the tenant facing bankruptcy or financial restructuring. It is particularly useful in commercial leasing situations where landlords are concerned about tenant solvency and seek to protect their rental income. Using this form helps ensure that the guarantor remains responsible for the lease obligations in adverse financial conditions affecting the tenant.

Who should use this form

- Landlords seeking to ensure financial security from guarantors in a lease agreement.

- Guarantors looking to understand their obligations in connection to the tenant's potential bankruptcy.

- Tenants who have guarantors and want clear documentation of their responsibilities in financial distress situations.

- Attorneys and real estate professionals drafting or reviewing lease agreements for commercial properties.

Completing this form step by step

- Identify all parties involved, including the landlord, tenant, and guarantor.

- Clearly state the obligations of the guarantor in relation to the lease.

- Specify any relevant dates associated with the lease and guaranty agreement.

- Review the boilerplate language for clarity and legal sufficiency.

- Have all parties sign and date the document to enforce the agreement.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all parties' names and details accurately.

- Not reviewing the terms for clarity regarding obligations in bankruptcy scenarios.

- Skipping signatures from all relevant parties, including the guarantor.

- Overlooking state-specific legal requirements that may affect validity.

Why complete this form online

- Convenient access to professionally drafted documents that can be downloaded instantly.

- Editability to tailor the form to specific lease conditions or agreements.

- Guidance through the process with legal language that is clear and easy to understand.

Legal use & context

- This form serves to protect landlords' interests in the event of tenant bankruptcy.

- Ensures that guarantors still hold financial responsibility regardless of tenant discharge scenarios.

- Provides clarity on rights and obligations stemming from insolvency proceedings.

Key takeaways

- The Guarantor Waiver protects landlords from financial loss due to tenant bankruptcy.

- It keeps the guarantor's obligations intact even if the tenant's financial situation changes.

- This form is essential for landlords involved in commercial leases with potential tenant insolvency risks.

Looking for another form?

Form popularity

FAQ

These categories are credit card purchases for luxury goods worth more than $650 in aggregate that were made during the 90 days preceding the bankruptcy filing and are owed to a single creditor, fraudulently obtained debts or those obtained under false pretenses, and debts incurred because of willful and malicious

For starters, being a guarantor means that you have an obligation to cover any payments that are not made by the main beneficiary. So if you have agreed to co-sign a loan agreement with a family member or friend and they default on their monthly payments, you will be required to step in a pay on their behalf.

If the guarantor refuses to make the repayment when due, the lenders can then begin to take legal action. A warning letter of pre-court action is typically then sent to the guarantor, with court proceedings beginning 14 days after, provided the repayment is still not made in this period.

So what rights do you have as a guarantor? You control the money: When the payment is made and the loan is funded, the money will go to your bank account as the guarantor.You can delay payment: Imagine that the borrower stops making payments and starts defaulting every month.

Although guarantor loan periods can last a long time, and your relationship with the borrower may change within this period, you cannot stop becoming their guarantor until the loan has been paid off in full. Whilst you can't stop being a guarantor, the loan period can be shortened by making an early repayment.

Unfortunately, if you have signed the loan agreement and the loan has been successfully paid out, you cannot stop being someone's guarantor. So the answer is simply, 'no. '

It's relatively common for a business owner to file individual bankruptcy to get rid of a personal guaranteeand most personal guarantees will qualify for discharge. If it's a nondischargeable debt, however, bankruptcy won't help.You'll have to file individual bankruptcy to get rid of the obligation.

An otherwise valid and enforceable personal guarantee can be revoked later in several different ways. A guaranty, much like any other contract, can be revoked later if both the guarantor and the lender agree in writing. Some debts owed by personal guarantors can also be discharged in bankruptcy.

If the guarantor refuses to make the repayment when due, the lenders can then begin to take legal action. A warning letter of pre-court action is typically then sent to the guarantor, with court proceedings beginning 14 days after, provided the repayment is still not made in this period.