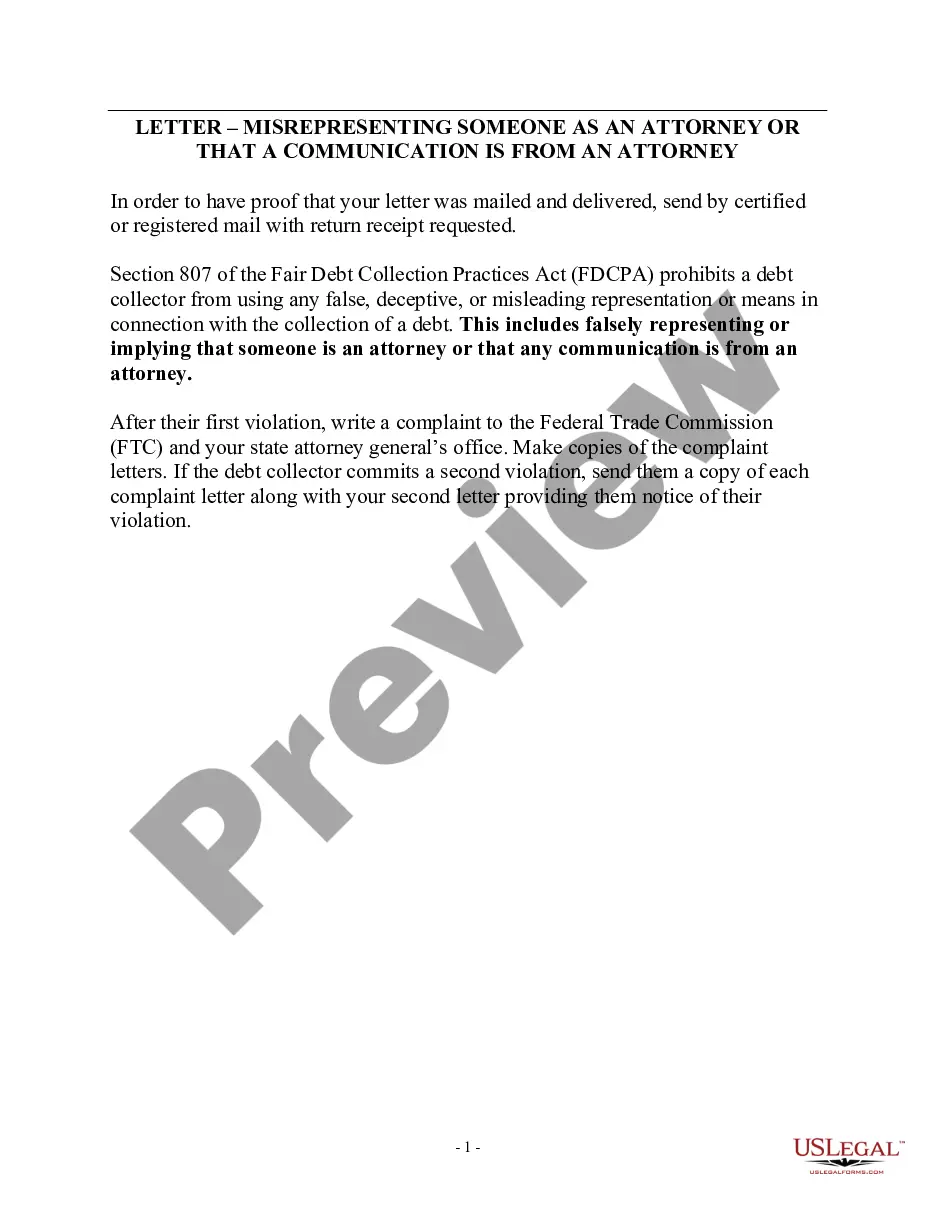

Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

About this form

The Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself is a legal document designed for debtors to formally notify creditors of any misleading practices related to debt collection. This form specifically addresses violations under Section 807 of the Fair Debt Collection Practices Act (FDCPA), which prohibits debt collectors from using false, deceptive, or misleading representations while collecting a debt. By using this form, you can assert your rights and hold creditors accountable for their actions.

Key parts of this document

- Your name and address.

- Recipient's name and address (creditor or debt collector).

- Case number associated with the debt.

- Description of the violation as it occurred.

- Request for cessation of misleading behavior.

- Enclosures section to list complaint letters sent to government authorities.

When to use this form

This form should be used when you believe a debt collector has violated the FDCPA by misrepresenting themselves or the debt they are attempting to collect. Real-world scenarios include receiving misleading letters, being contacted by debt collectors who falsely claim to represent a government agency, or encountering collection tactics that involve deception or intimidation. Utilizing this notice can help you document the violation and take steps toward resolution.

Who should use this form

This form is intended for:

- Debtors who have been subjected to misleading debt collection practices.

- Consumers who want to assert their rights under the Fair Debt Collection Practices Act.

- Individuals seeking to resolve disputes with creditors or debt collectors.

Instructions for completing this form

- Identify yourself by entering your name and address at the top of the letter.

- Clearly state the recipient's name and address, including a contact person if available.

- Note the relevant case number associated with the debt.

- Provide a detailed description of the violation, outlining how the creditor misrepresented themselves.

- Sign and date the letter, then send it using certified or registered mail for proof of delivery.

- Keep copies of the letter and any correspondence for your records.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to send the letter via certified or registered mail, which can limit proof of delivery.

- Not including a specific case number, which can confuse the recipient.

- Using vague language that does not specifically describe the violation.

- Neglecting to keep copies of all correspondence related to the violation.

Why complete this form online

- Convenient access from anywhere at any time, allowing for easy completion.

- Editable document format enables customization to fit your specific situation.

- Reliability of attorney-drafted templates ensures compliance with legal standards.

- Quick delivery of the document can expedite your response to creditors.

Legal use & context

- This form serves as a formal notification to creditors about their violations of the FDCPA.

- It provides evidence of attempts to resolve the issue amicably before pursuing further legal action.

- Understanding your rights under the FDCPA can empower consumers against harassment tactics.

Looking for another form?

Form popularity

FAQ

Sue the Debt Collector in State Court. Sue the Creditor in Small Claims Court. Report the Action to a Government Agency. Report the Action to the State Attorney General. Use the Violation as Leverage in Debt Settlement Negotiations.

Under the Fair Debt Collection Practices Act, debt collectors are required to identify themselves in any communication with a debtor. This rule prevents collection agents from tricking consumers into returning calls or other communications without knowing the nature of the communication.

In most cases, a debt collector may not tell anyone other than you, your spouse or your attorney that you owe money.

The Fair Debt Collection Practices Act (FDCPA) protects debtors from harassment by debt collectors. If a collector has violated the FDCPA, you can sue the collector in court. The FDCPA provides a range of damages for successful FDCPA lawsuits, including monetary damages, attorneys' fees, and more.

For example, they can't: misrepresent the amount you owe. lie about being attorneys or government representatives. falsely claim you'll be arrested, or claim legal action will be taken against you if it's not true.

In an individual action, a plaintiff may recover actual damages, but courts have consistently held that additional damages are limited to a maximum of $1,000 per proceeding and not $1,000 per violation. See, e.g., Wright v.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.The court might also order the debt collector to stop engaging in certain collection activities.

Harassment of the debtor by the creditor More than 40 percent of all reported FDCPA violations involved incessant phone calls in an attempt to harass the debtor.