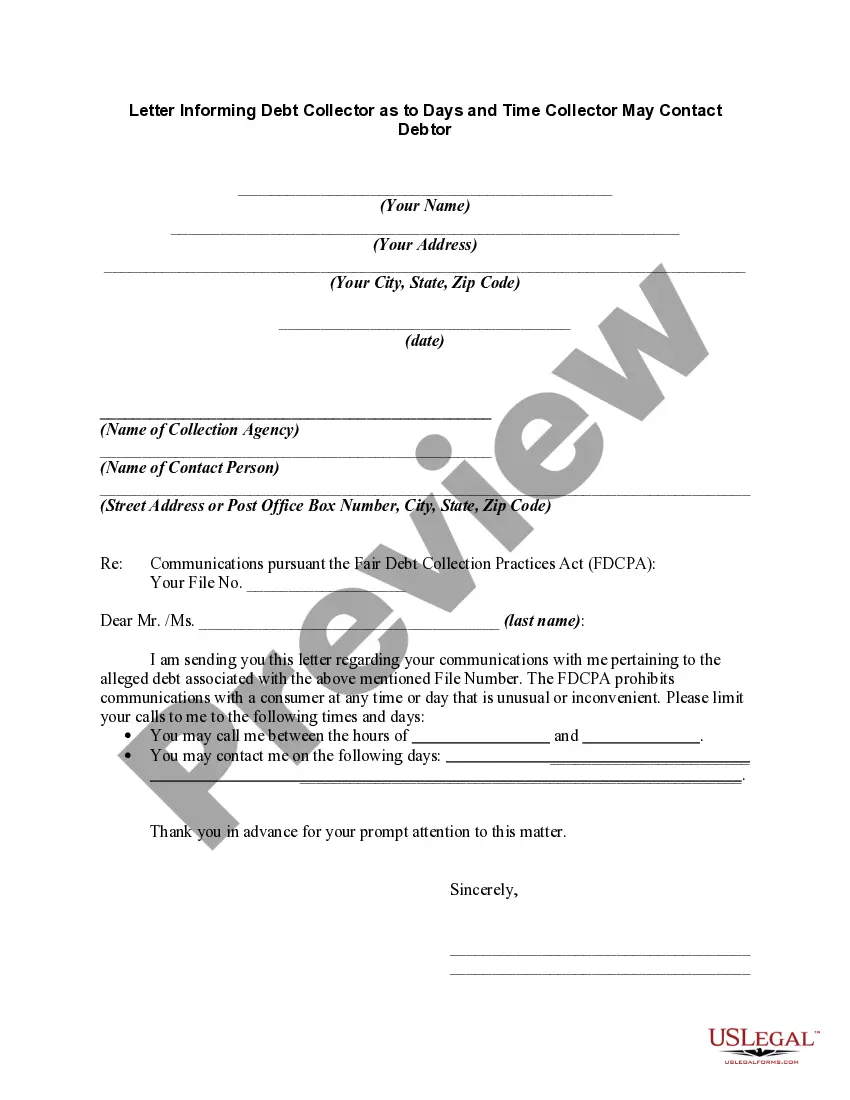

Letter to Debt Collector - Only call me on the following days and times

What this document covers

The Letter to Debt Collector is a legal document that allows you to formally communicate your preferred days and times for receiving calls from debt collectors. This form is important for consumers who want to exercise their rights under the Fair Debt Collection Practices Act (FDCPA) by limiting unsolicited contact. Using this letter helps establish boundaries and protect your privacy during the debt collection process.

Key parts of this document

- Your personal information, including name and address

- Debt collector's company name and contact information

- Specific times and days when you will accept calls

- Identification of the case number related to the alleged debt

- A space for documenting violations of your stated communication preferences

Situations where this form applies

You should use this form when you have received communications from a debt collector and want to specify acceptable times for further contact. This is especially useful if you find their calls disruptive or if you want to maintain a record of your communications. Additionally, this form serves as a precursor to formal complaints if the debt collector fails to comply with your request.

Intended users of this form

- Individuals currently receiving calls from debt collectors

- Consumers who wish to assert their rights under the FDCPA

- People experiencing harassment from debt collectors

- Anyone looking to establish a controlled communication environment regarding their debt

Completing this form step by step

- Enter your name and address at the top of the letter.

- List the debt collector's company name and contact details.

- Clearly specify the days and times you are available for their calls.

- Include the case number associated with the alleged debt.

- Sign and date the letter before mailing it.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. Sending it via certified mail provides sufficient proof of your communication to the debt collector.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Not providing complete contact information for both parties.

- Failing to specify clear days and times for communication.

- Not sending the letter via certified mail for proof of delivery.

- Neglecting to keep copies of the letter and any correspondence.

Why complete this form online

- Convenient access to a professionally drafted document tailored to your needs.

- Edit and customize fields quickly to reflect your specific situation.

- Reliable format ensures compliance with legal standards.

- Immediate downloading means you can act without delay.

Legal use & context

- This form is legally recognized under the FDCPA, which grants consumers the right to manage debt collection communications.

- Proper use of this form may help in taking legal action against a debt collector for violations.

Key takeaways

- Control your communication with debt collectors by specifying your preferred contact times.

- Utilize this form to document interactions and protect your rights under the FDCPA.

- Ensure you send your letter via certified mail for verification purposes.

Looking for another form?

Form popularity

FAQ

Even if the debt is yours, you still have the right not to talk to the debt collector and you can tell the debt collector to stop calling you. However, telling a debt collector to stop contacting you does not stop the debt collector or creditor from using other legal ways to collect the debt from you if you owe it.

Federal law doesn't give a specific limit on the number of calls a debt collector can place to you. A debt collector may not call you repeatedly or continuously intending to annoy, abuse, or harass you or others who share the number. You do have a right to tell the debt collector to stop calling you.

Debt Collectors Can't Call You Repeatedly to Harass You This means that while the FDCPA doesn't place a specific limit on the number of calls debt collectors can make, it prohibits them from calling you multiple times just to harass you. (15 U.S. Code § 1692d).

Federal law doesn't give a specific limit on the number of calls a debt collector can place to you. A debt collector may not call you repeatedly or continuously intending to annoy, abuse, or harass you or others who share the number. You do have a right to tell the debt collector to stop calling you.

Answer the phone and explain you're not the person they're looking for. Tell them that the number they're calling is not the right one. Send a cease and desist letter to request that they stop contacting you.

As per the FDCPA rules and regulations, debt collectors can call you during the weekdays (that is from Monday to Saturday) between 8 am and 9 pm. But on Sunday, debt collectors can call you between 1 pm and 5 pm. They can't call you beyond that time.

The act prohibits publicizing your debts, and showing up at your job to collect your debt counts. They may, however, call you at work, though they can't reveal to your co-workers that they are debt collectors. To stop these calls, ask the debt collector not to contact you at work. They must stop, according to the law.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

Generally, debt collectors cannot call you at an unusual time or place, or at a time or place they know is inconvenient to you and they are prohibited from contacting you before 8 a.m. or after 9 p.m.