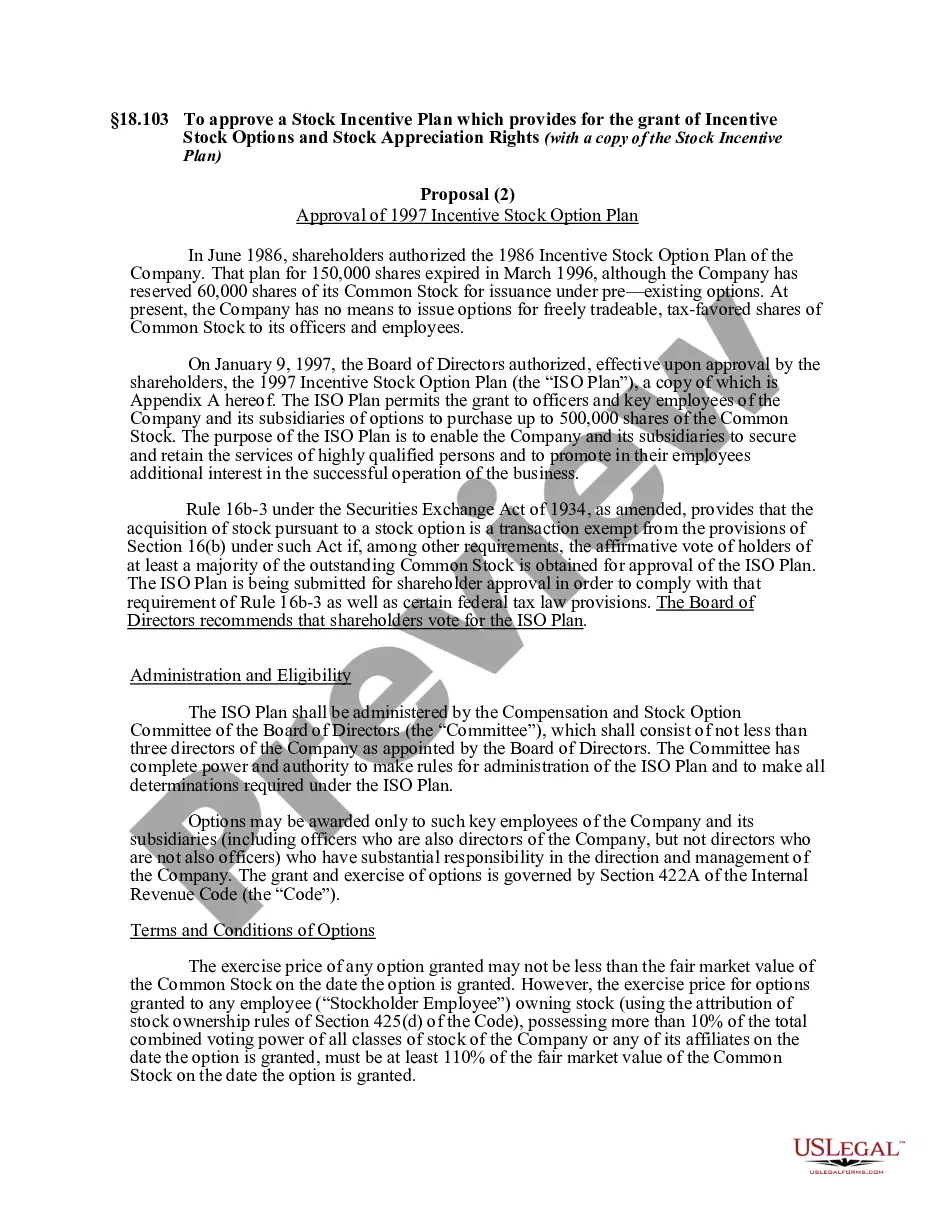

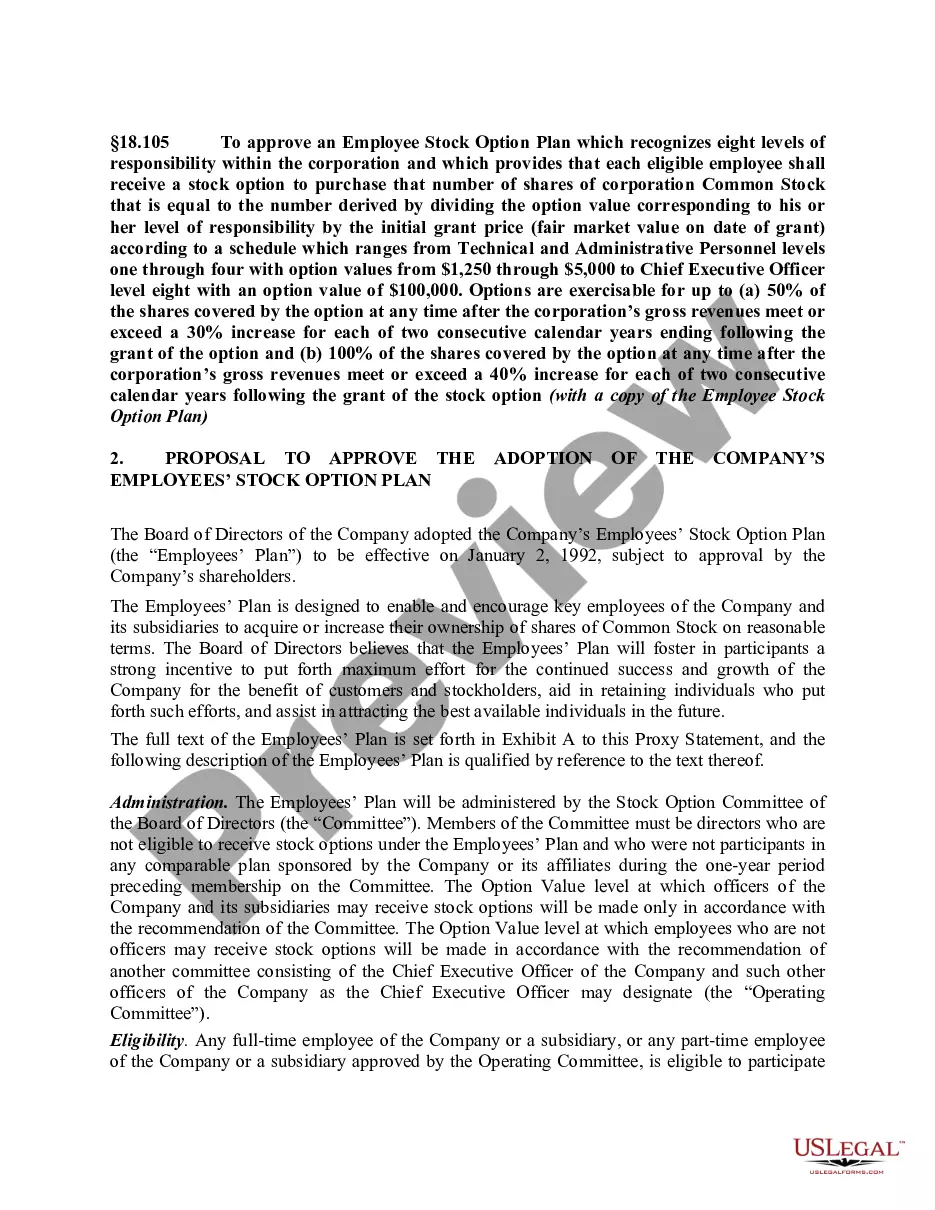

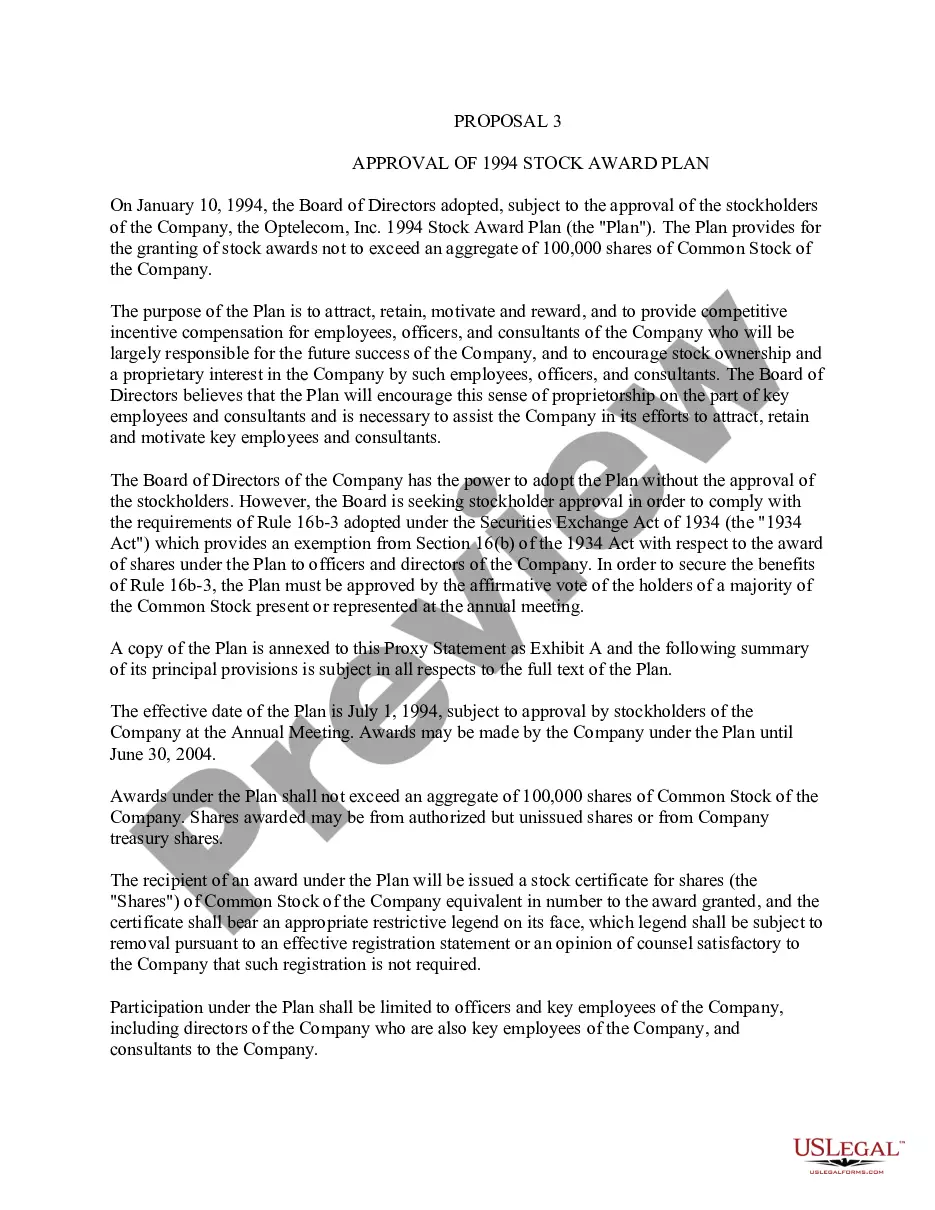

Proposal Approval of Nonqualified Stock Option Plan

About this form

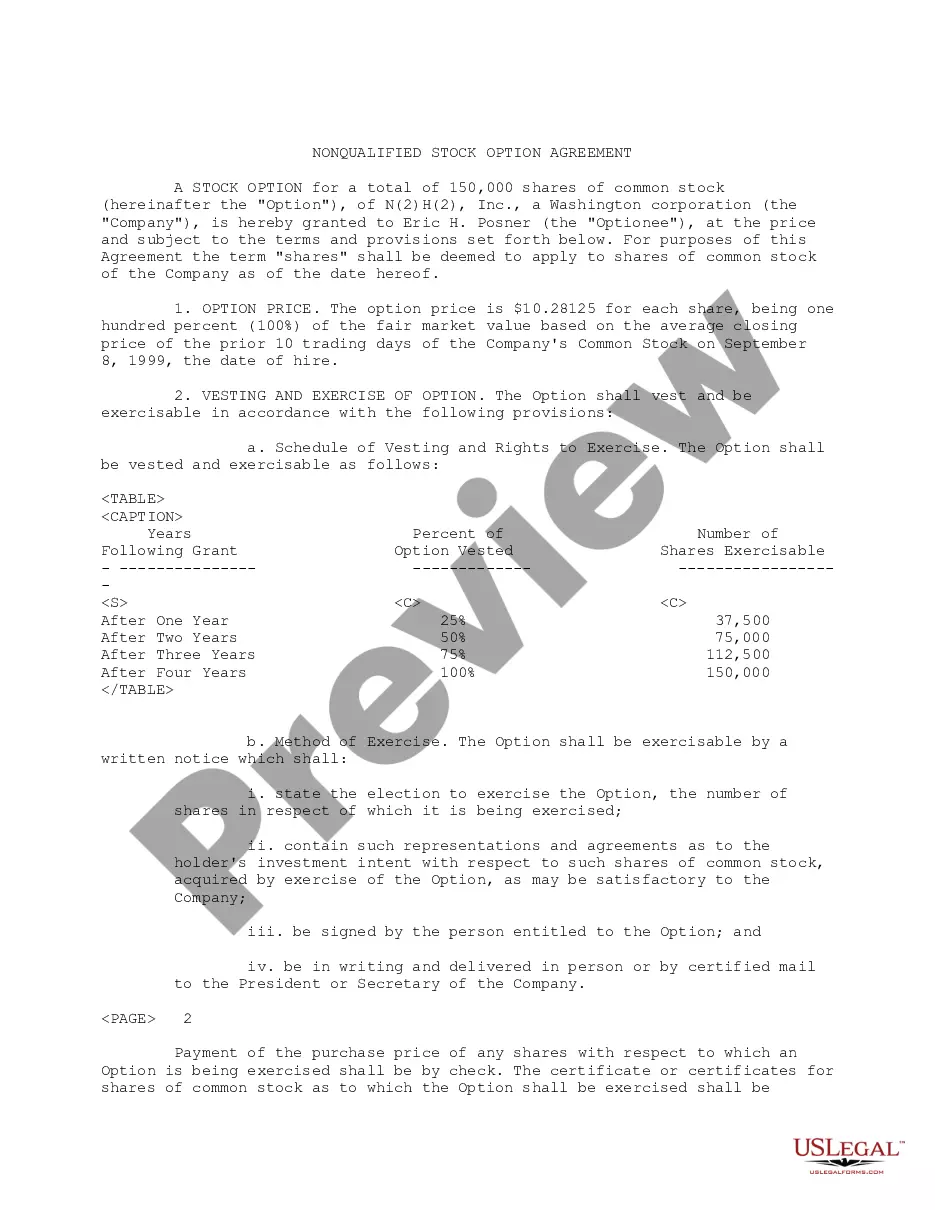

The Proposal Approval of Nonqualified Stock Option Plan is a legal document used by companies to secure shareholder approval for a new stock option plan aimed at compensating key employees and officers. This form outlines the specifics of the 1997 Non-Qualified Stock Option Plan, detailing the number of shares authorized, eligibility criteria, and the administration of the plan. It differs from other forms by focusing specifically on nonqualified stock options, which provide companies with a flexible way to incentivize employees without adhering to certain regulatory limits applicable to qualified stock options.

Main sections of this form

- Introduction of the 1997 Non-Qualified Stock Option Plan and its purpose.

- Administration details including the Compensation and Stock Option Committee's role.

- Eligibility requirements for key employees and management.

- Details regarding the terms and conditions of options and Stock Appreciation Rights (SARs).

- Provisions for antidilution and adjustments in case of market changes.

- Federal income tax implications for options and SARs exercised under the plan.

When to use this form

This form should be used when a company needs to propose a new nonqualified stock option plan to its shareholders for their approval. It is particularly relevant during corporate restructuring, when aiming to attract or retain key talent, or when an existing stock option plan expires and needs replacement. Companies planning to issue options to employees as part of their compensation package will also require this form to ensure compliance with legal and regulatory obligations.

Who this form is for

- Corporate boards of directors looking to implement a nonqualified stock option plan.

- Shareholders who need to review and approve changes to stock option plans.

- Human resource professionals tasked with employee compensation and benefits.

- Legal teams ensuring compliance with Securities Exchange Act requirements.

How to complete this form

- Identify the parties involved, including the company and its shareholders.

- Detail the plan setup, including the number of shares available for issuance under the new stock option plan.

- Specify the eligibility criteria for employees and management who will receive options.

- Outline the procedure for administering the stock option plan and the oversight by the Compensation and Stock Option Committee.

- Ensure all necessary legal language and compliance measures are included according to relevant securities laws.

Is notarization required?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately define the number of shares available under the plan.

- Neglecting to comply with specific state laws or corporate governance requirements.

- Overlooking the required majority vote from shareholders for approval.

- Not including complete details about the administration of the stock option plan.

Why use this form online

- Convenient access to legally compliant templates that are easy to download and fill out.

- Editable format allows users to customize components as necessary for their specific needs.

- Reliable and secure storage options for completed forms, ensuring important documents are always retrievable.

- Time-saving ability to complete and submit forms electronically.

Legal use & context

- This form is governed by federal laws regarding stock options and must adhere to the guidelines under the Securities Exchange Act.

- Shareholder approval is essential to ensure the validity of the nonqualified stock option plan.

- Understanding the tax consequences is important for both the company and employees participating in the plan.

Main things to remember

- The Proposal Approval of Nonqualified Stock Option Plan is essential for companies to seek shareholder approval for stock options.

- Understanding eligibility, administration, and tax implications is critical when using this form.

- The plan aims to attract and retain employees by providing stock ownership opportunities.

Looking for another form?

Form popularity

FAQ

Employers must report the income from a 2020 exercise of Non-qualified Stock Options in Box 12 of the 2020 Form W-2 using the code V. The compensation element is already included in Boxes 1, 3 (if applicable) and 5, but is also reported separately in Box 12 to clearly indicate the amount of compensation arising from

Stock options are of two main types. Incentive stock options, generally only offered to key employees and top management, receive preferential tax treatment in many cases, as the IRS treats gains on such options as long-term capital gains.

Start with Form 8949, Part I, Short-Term Capital Gains and Losses. Check Box C since you did not receive a Form 1099. On Line 1, Column A, Description of Property, enter the name of the company or its symbol, and after that write "call options" and the number of call options you sold.

Qualified stock options, also known as incentive stock options, can only be granted to employees. Non-qualified stock options can be granted to employees, directors, contractors and others. This gives you greater flexibility to recognize the contributions of non-employees.

Any compensation income received from your employer in the current year is included on Form W-2 in Box 1. If you sold any stock units to cover taxes, this information is included on Form W-2 as well. Review Boxes 12 and 14 as they list any income included on Form W-2 related to your employee stock options.

Once you exercise your non-qualified stock option, the difference between the stock price and the strike price is taxed as ordinary income. This income is usually reported on your paystub.If you hold the shares for less than one year, any gain is taxed at your ordinary income tax rates, which are usually higher.

The Cost Basis of Your Non-Qualified Stock Options The cost basis is equal to the exercise price, multiplied by the number of shares exercised. In our example above, the cost basis is equal to 2,000 shares times $50/share, or $100,000.

However, when you sell an optionor the stock you acquired by exercising the optionyou must report the profit or loss on Schedule D of your Form 1040. If you've held the stock or option for less than one year, your sale will result in a short-term gain or loss, which will either add to or reduce your ordinary income.

Disqualifying Disposition: Income recognized on W-2 is NOT subject to income tax withholding or FICA or Medicare withholding.