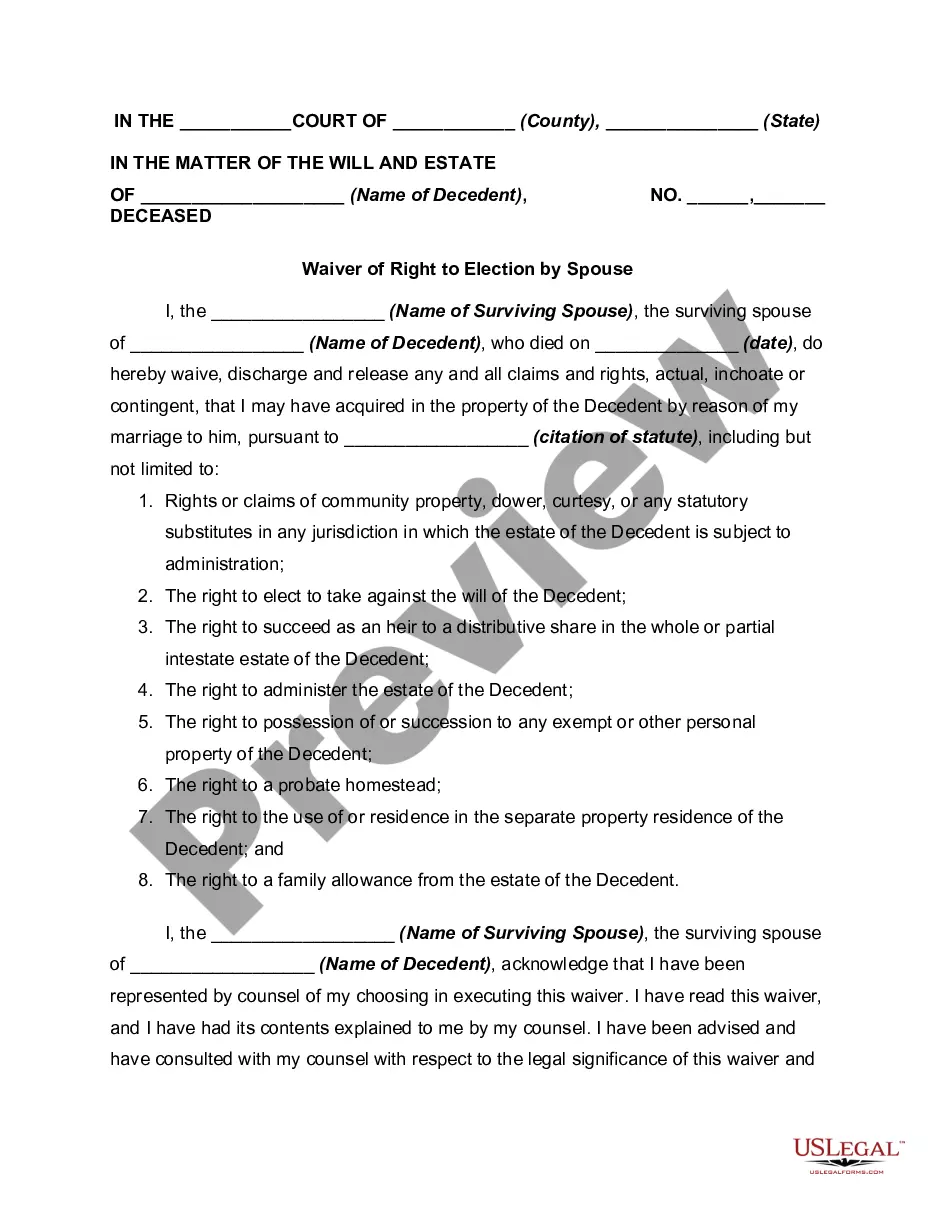

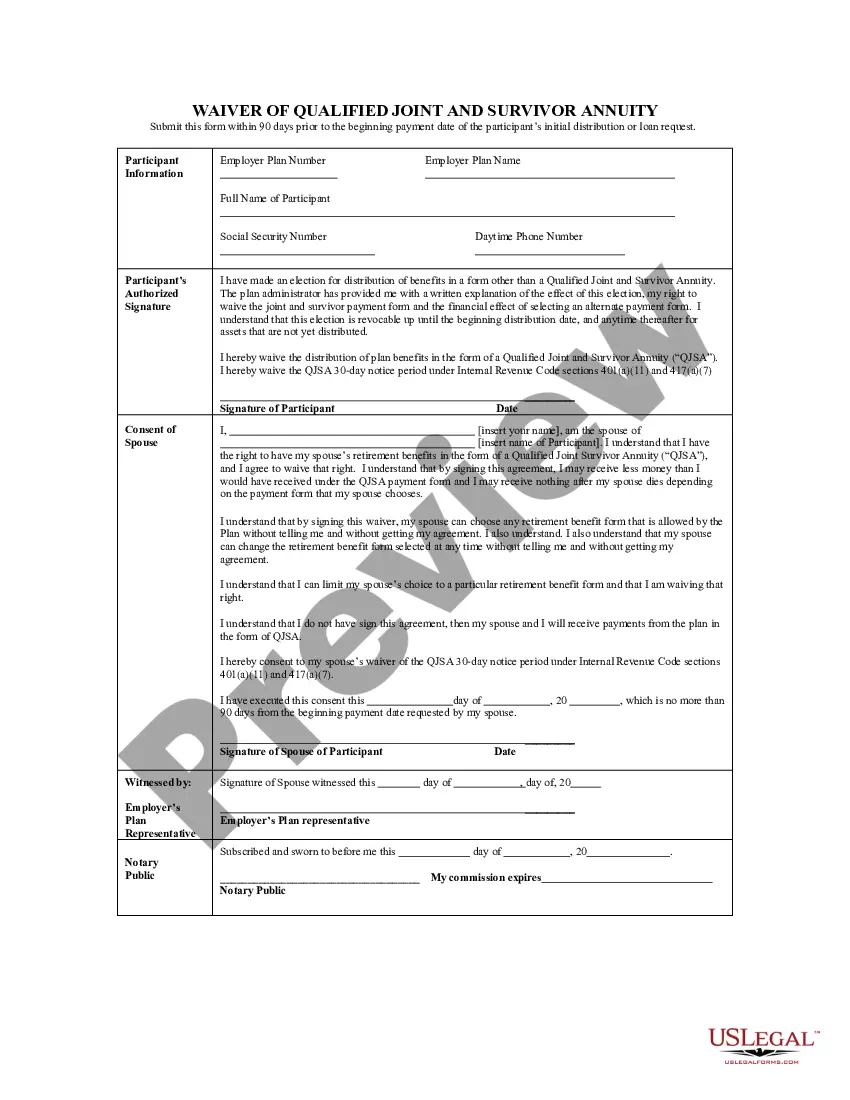

Waiver of the Right to be Spouse's Beneficiary

About this form

The Waiver of the Right to be Spouse's Beneficiary is a legal document that allows a spouse to voluntarily surrender their rights as a beneficiary to their partner's vested account. This form is essential for couples who wish to designate a different beneficiary for retirement accounts or other financial assets rather than automatically allocating those rights to the spouse. This form differs from standard beneficiary designations as it specifically addresses the relinquishment of rights by a spouse, a crucial consideration in estate planning and financial management.

Key components of this form

- The name of the spouse waiving their rights.

- The account or plan name for which the waiver is being executed.

- A clear statement indicating the voluntary nature of the waiver.

- Options for changing the waiver agreement, if applicable.

- Signature sections for both the waiving spouse and a witness.

Situations where this form applies

This form should be used in situations where a married individual wants to designate someone other than their spouse as the beneficiary of their financial accounts, such as retirement plans or trust funds. It is often utilized during estate planning to ensure that specific assets are directed according to the account holder's personal wishes, or when a couple is considering separation or divorce but wants to clarify financial rights before taking legal action.

Intended users of this form

- Spouses who wish to waive their rights to a vested account as a beneficiary.

- Individuals engaged in estate planning who want to specify alternate beneficiaries.

- Couples considering legal separation or divorce.

- Anyone wanting to ensure clarity in financial rights and beneficiary designations.

How to prepare this document

- Enter the names and details of both spouses involved.

- Specify the account or plan name for which the waiver is being applied.

- Review the waiver statement to ensure understanding of rights being relinquished.

- Decide on options for future changes to the waiver agreement if necessary.

- Sign and date the form in the presence of a witness.

Notarization requirements for this form

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Not completing all required fields, leading to an invalid waiver.

- Failing to obtain a witness signature, which may render the form unenforceable.

- Signing the form without fully understanding the rights being waived.

- Not keeping a copy of the signed form for personal records.

Why use this form online

- Convenient access to a legally vetted document, reducing the need for expensive legal consultations.

- Editable fields that allow for personalized information to be added easily.

- Availability of integrated online notarization to ensure legal compliance.

- Secure storage options for completed forms enhance peace of mind.

Looking for another form?

Form popularity

FAQ

This insures the inheritance rights of their children from prior marriages in their respective estates, without having the estate reduced by the share given to the surviving spouse under the laws of intestacy.

A spousal consent is a document signed by the spouse of a member in a limited liability company that has an operating agreement amongst the members or a shareholder in a corporation that has a shareholders agreement amongst the shareholders.

Does the Surviving Spouse Automatically Become the Beneficiary of a Life Insurance Policy? Usually, there is no requirement in the policy itself that only a spouse be named as the beneficiary. The policy owner has the right to choose any beneficiary they wish.

A Member's spouse uses the Spousal Waiver Form to waive his/her legal right to pension benefits after the Member's death. If the Member wishes to select a form of pension that doesn't provide income to his spouse after the Member dies, then the spouse must complete this form prior to the Member's retirement.

The Spouse Is the Automatic Beneficiary for Married People A federal law, the Employee Retirement Income Security Act (ERISA), governs most pensions and retirement accounts.

A Member's spouse uses the Spousal Waiver Form to waive his/her legal right to pension benefits after the Member's death. If the Member wishes to select a form of pension that doesn't provide income to his spouse after the Member dies, then the spouse must complete this form prior to the Member's retirement.

Generally, no. Typically, a spouse who has not been named a beneficiary of an individual retirement account (IRA) is not entitled to receive, or inherit, the assets when the account owner dies.

Your State's community property law requires that you must obtain your spouse's consent for any designation that does not allow your spouse to receive the annuity's death benefit. If your spouse agrees to waive this right, your spouse will need to complete and sign this waiver and have his or her signature notarized.