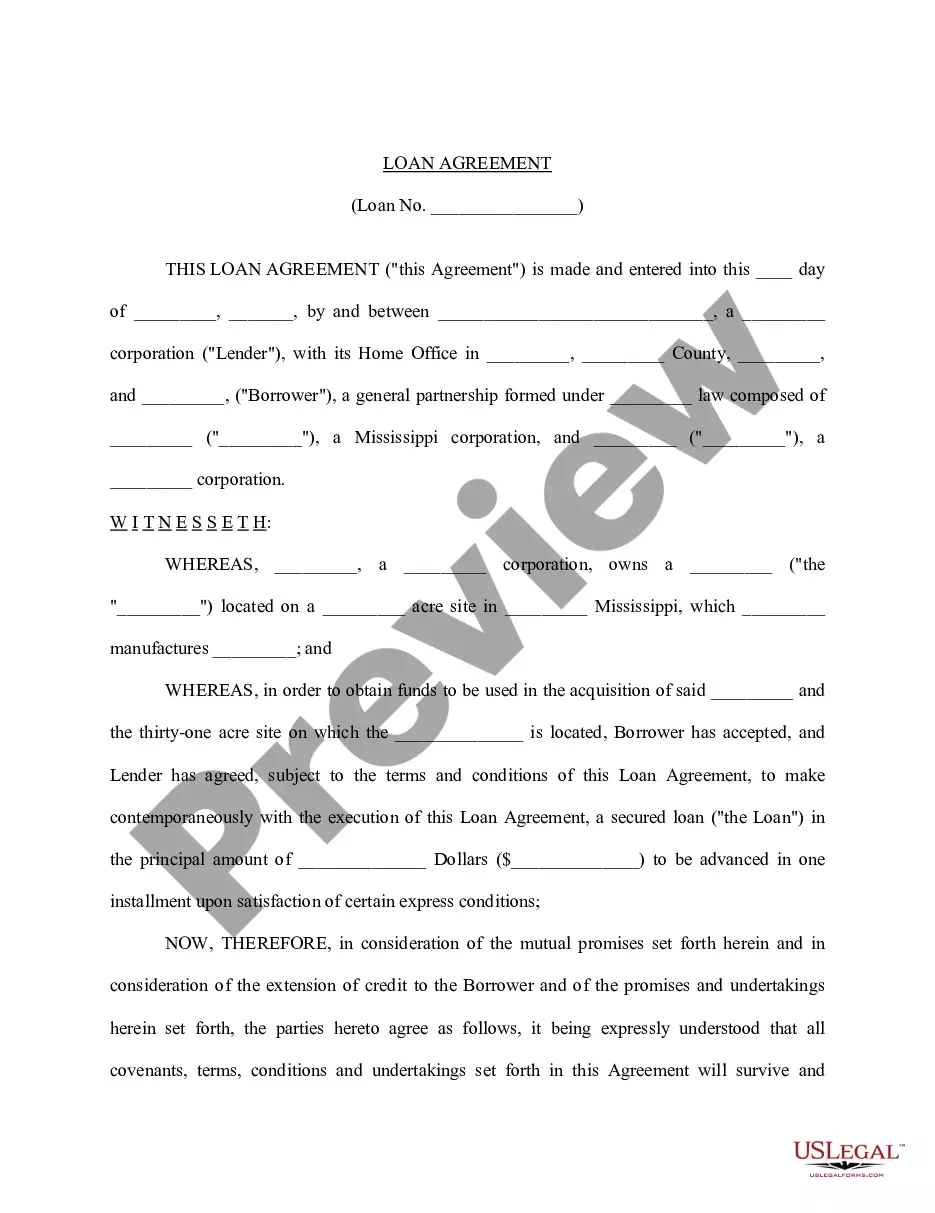

Building Loan Agreement between Lender and Borrower

Understanding this form

This Building Loan Agreement between Lender and Borrower is a legally binding document that outlines the terms and conditions under which a lender provides a loan to a borrower for the purpose of constructing a building on real property. This agreement establishes the responsibilities of both parties, describes the loan amount, interest rates, payment schedule, and requirements for building construction. Unlike common loan agreements, this form specifically addresses construction financing and includes provisions related to the property and construction project involved.

Key parts of this document

- Identification of the borrower and lender, including their legal business structure and addresses.

- Details about the loan amount, interest rate, and payment terms.

- Specifications regarding the construction project, including plans that require lender approval.

- Conditions for securing the loan with a mortgage on the property.

- Provisions for inspection and release of mortgage portions as needed.

- Stipulations regarding legal compliance, including the necessity for notifications and approvals.

Common use cases

This form should be used when a borrower seeks financing to construct a building and needs to formalize the agreement with a lender. Situations that often require this agreement include residential home construction, commercial property development, and any situation where the borrower intends to secure a loan specifically for building purposes. Additionally, it is necessary to establish clear terms to protect both the lender's investment and the borrower's obligations.

Who needs this form

- Individuals or businesses looking to secure a construction loan from a lender.

- Lenders providing financing for construction projects.

- Contractors involved in construction who may need to facilitate agreements between lenders and borrowers.

- Real estate developers needing to establish clear financial terms for a building project.

How to prepare this document

- Identify the parties involved by entering the names and addresses of both the borrower and lender.

- Specify the loan amount and the applicable interest rate.

- Detail the property description that will secure the loan and include any necessary plans.

- Fill in the terms regarding payment schedules, including start dates and payment amounts.

- Ensure that all relevant parties sign the document to finalize the agreement legally.

Is notarization required?

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to accurately describe the property being financed.

- Leaving out necessary details about payment schedules or interest rates.

- Not obtaining the required approvals for construction plans before finalizing the agreement.

- Inadequate signatures or missing initials in key sections of the document.

- Neglecting to verify state-specific legal requirements for construction loans.

Why complete this form online

- Convenience of accessing and completing the document from anywhere with internet access.

- Editability allows users to customize the form according to their specific needs and details.

- Accuracy is enhanced by using templates created by licensed attorneys.

- Immediate download provides instant access to essential legal documents.

- Time-saving compared to traditional methods of document creation and customization.

Looking for another form?

Form popularity

FAQ

The most basic loan agreement is commonly called an "IOU." These are typically used between friends or relatives for small amounts of money, and simply state the dollar amount that is owed. They do not usually say when payment is due, nor include any interest provisions.

Loan agreements are binding contracts between two or more parties to formalize a loan process.Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid.

For a personal loan agreement to be enforceable, it must be documented in writing and signed by both parties. You may choose to keep a copy in your county recorder's office if you wish, though it's not legally necessary. It's sufficient for both parties to keep their own copy, ideally in a safe place.

A loan agreement does not require a notary signature. The purpose of a notary seal is to provide evidence that the signature is genuinely the signature of the person signing.

Borrower-lender agreement means a credit agreement (i) to finance a transaction between the borrower and a person (the supplier) other than the lender, and. (ii)

Identity of the Parties. The names of the lender and borrower need to be stated. Date of the Agreement. Interest Rate. Repayment Terms. Default provisions. Signatures. Choice of Law. Severability.

Come up with a schedule for repayment. Use a family contract template that includes a repayment schedule. Set and interest rate. Put your agreement in writing. Keep payment records.

Starting the Document. Write the date at the top of the page. Write the Terms of the Loan. State the purpose of the personal payment agreement and the terms for returning the money. Date the Document. Statement of Agreement. Sign the Document. Record the Document.

State the purpose for the loan. #Set forth the amount and terms of the loan. Your agreement should clearly state the amount of money you're lending your friend, the interest rate, and the total amount your friend will pay you back.