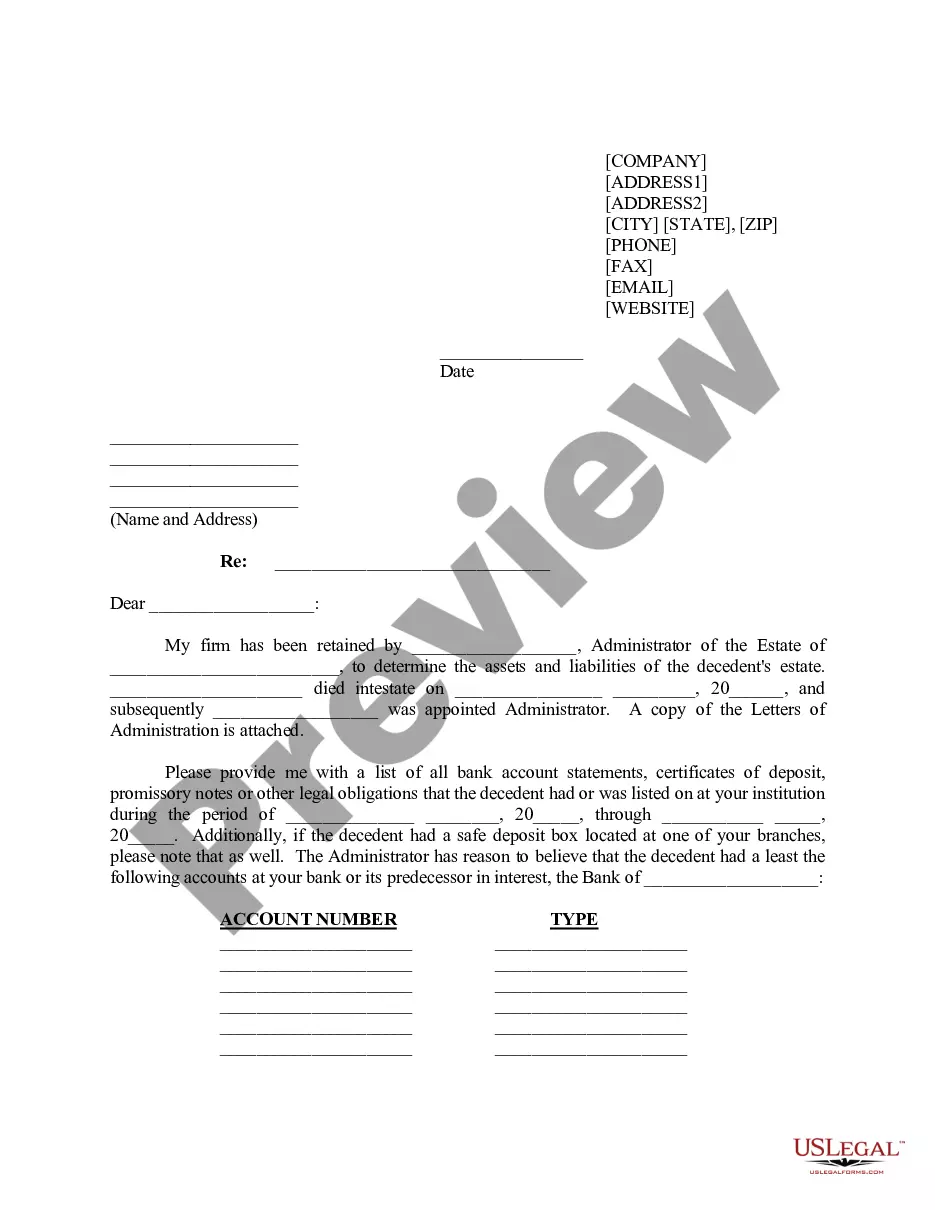

Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent

About this form

This Letter of Instruction to Investment Firm Regarding Account of Decedent is a legal document used by an executor or trustee to request the transfer of assets from an investment account of a deceased individual to a trust. This form ensures that the distribution of assets is carried out according to the decedent's last will and testament, thereby distinguishing it from other transfer requests that do not involve a trust arrangement.

What’s included in this form

- Identifying information of the investment firm

- Details about the decedent, including their name and probate court

- Designation of the executor and trustee with accompanying legal documents

- Specific instructions for asset transfer from the investment account to the trust

- Enclosures such as Letters Testamentary and a certified copy of the Will

- Contact information for the executor or trustee

Situations where this form applies

This form should be used when a decedent has left a will that specifies assets in an investment account to be transferred to a testamentary trust. Typically, this situation arises following the death of an individual when the executor is responsible for executing the will and ensuring the estate's wishes are carried out. It is particularly important in cases where the investment assets need to be legally directed to a trust for future management.

Who can use this document

- Executors named in a decedent's last will and testament

- Trustees designated to manage a testamentary trust

- Individuals dealing with the estate of a deceased person who had investment accounts

How to complete this form

- Identify and enter the name and address of the investment firm.

- Provide the name of the decedent and the probate details, including the court name and jurisdiction.

- Attach a copy of the Letters Testamentary and the certified Will.

- Specify the exact assets to be transferred and any instructions regarding asset liquidation.

- Sign and date the form, including your contact information for follow-up.

Does this form need to be notarized?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all required enclosures, such as the certified Will and Letters Testamentary.

- Not clearly specifying which assets should be transferred or liquidated.

- Leaving out contact information, which can delay communication.

Why complete this form online

- Convenient and quick access to legal templates at any time.

- Edit or fill out the form easily to suit specific needs without complexity.

- Reliability, with forms drafted by licensed attorneys ensuring legal compliance.

Summary of main points

- The form serves to instruct an investment firm to transfer decedent's account assets to a trust.

- Proper completion is crucial to ensure assets are transferred in accordance with the decedent's will.

- It is important to verify local legal requirements regarding asset transfers.

Looking for another form?

Form popularity

FAQ

Most brokerage companies allow the beneficiary to claim the assets of the account once the beneficiary provides the broker with a death certificate. At that point, the beneficiary can keep the brokerage account at the same broker, retitling it in the beneficiary's own name.

Once the necessary documents are received, a new account is typically set up for the beneficiary or estate, at which time securities registered in the name of the deceased person will be transferred.

The Uniform Transfer on Death Securities Registration Act lets owners name beneficiaries for their stocks, bonds, or brokerage accounts. The process is similar to a payable-on-death bank account.They can then name beneficiaries, and percentage allocations, on the beneficiary form provided by the broker or bank.

When someone dies, their investments will be handed over to any designated beneficiaries. You'll generally have three options for ensuring that your investment assets are transferred after you die: Transfer on death (TOD) registration. Trust accounts.

In order to pay bills and distribute assets, the executor must gain access to the deceased bank accounts.Obtain an original death certificate from the County Coroner's Office or County Vital Records where the person died. Photocopies will not suffice. Expect to pay a fee for each copy.

Transfer on death (TOD) a provision of a brokerage account that allows the account's assets to pass directly to an intended beneficiary; the equivalent of a beneficiary designation. Estate Planning and Inheritance Glossary.

Brokerage accounts, on the other hand, generally pass to your beneficiaries through your will and must go through probate first, which can be time-consuming, public and expensive in some states.Joint accounts are also subject to the claims of both owners' creditors.

Before distributing assets to beneficiaries, the executor must pay valid debts and expenses, subject to any exclusions provided under state probate laws.The executor must maintain receipts and related documents and provide a detailed accounting to estate beneficiaries.

All taxes and liabilities paid from the estate, including medical expenses, attorney fees, burial or cremation expenses, estate sale costs, appraisal expenses, and more. The executor should keep all receipts for any services or transactions needed to liquidate the assets of the deceased.