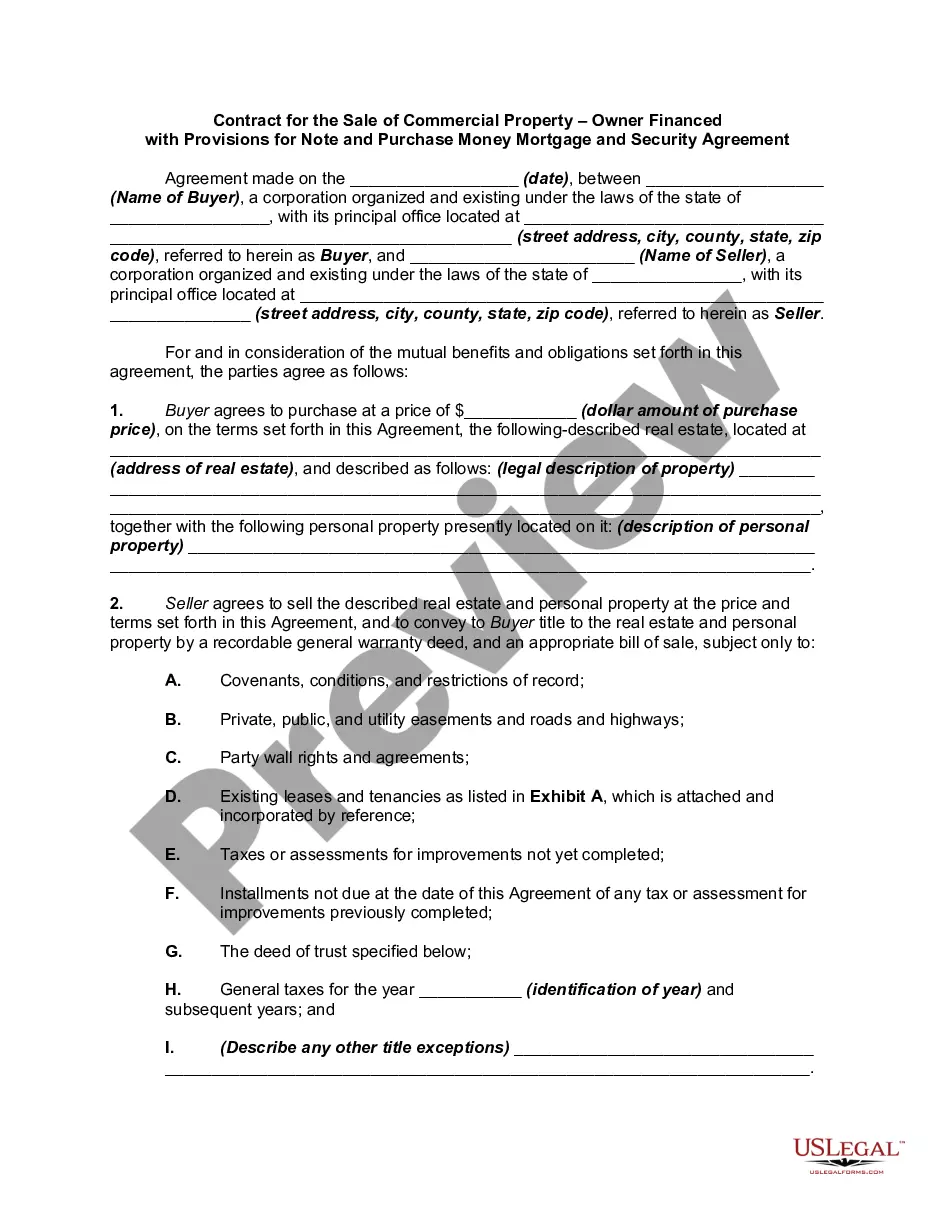

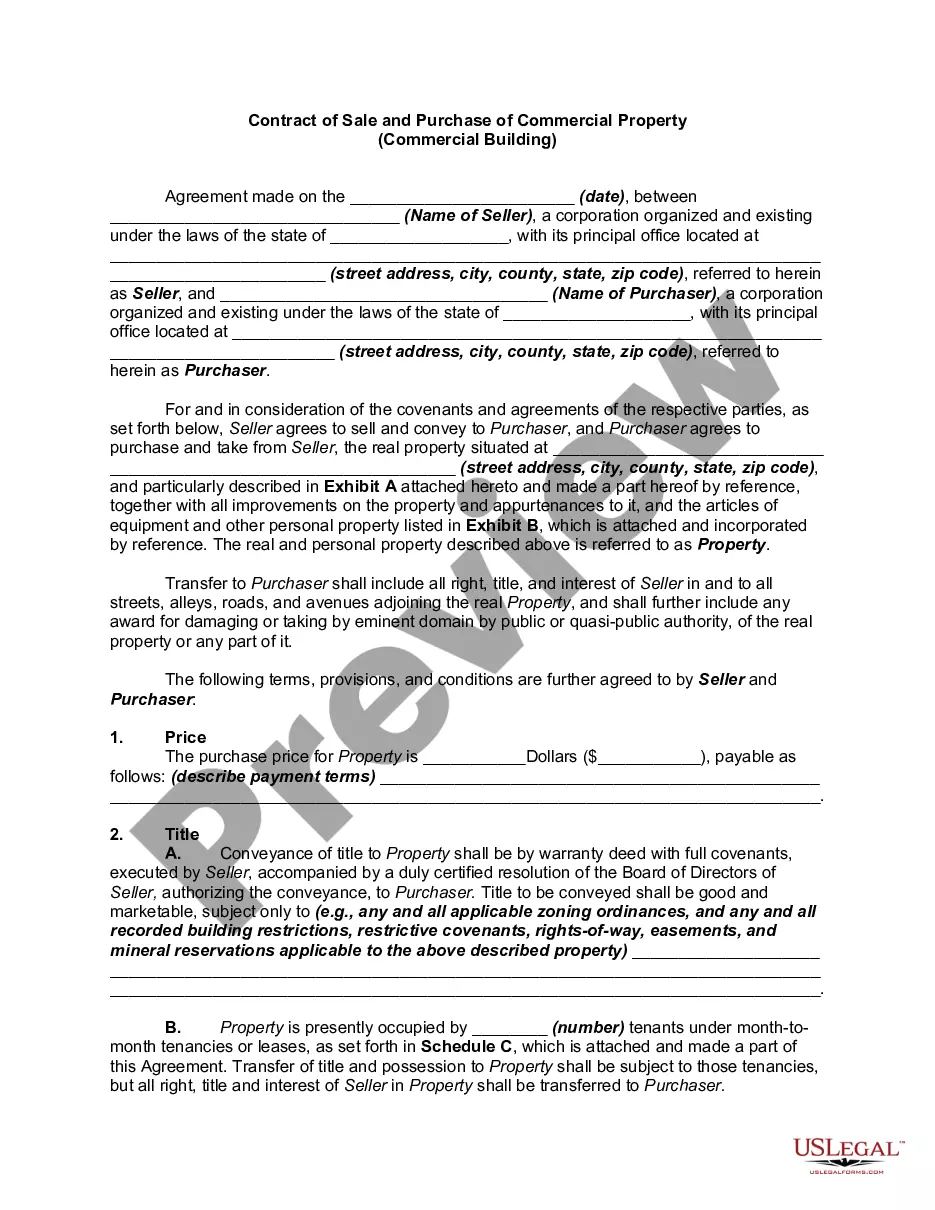

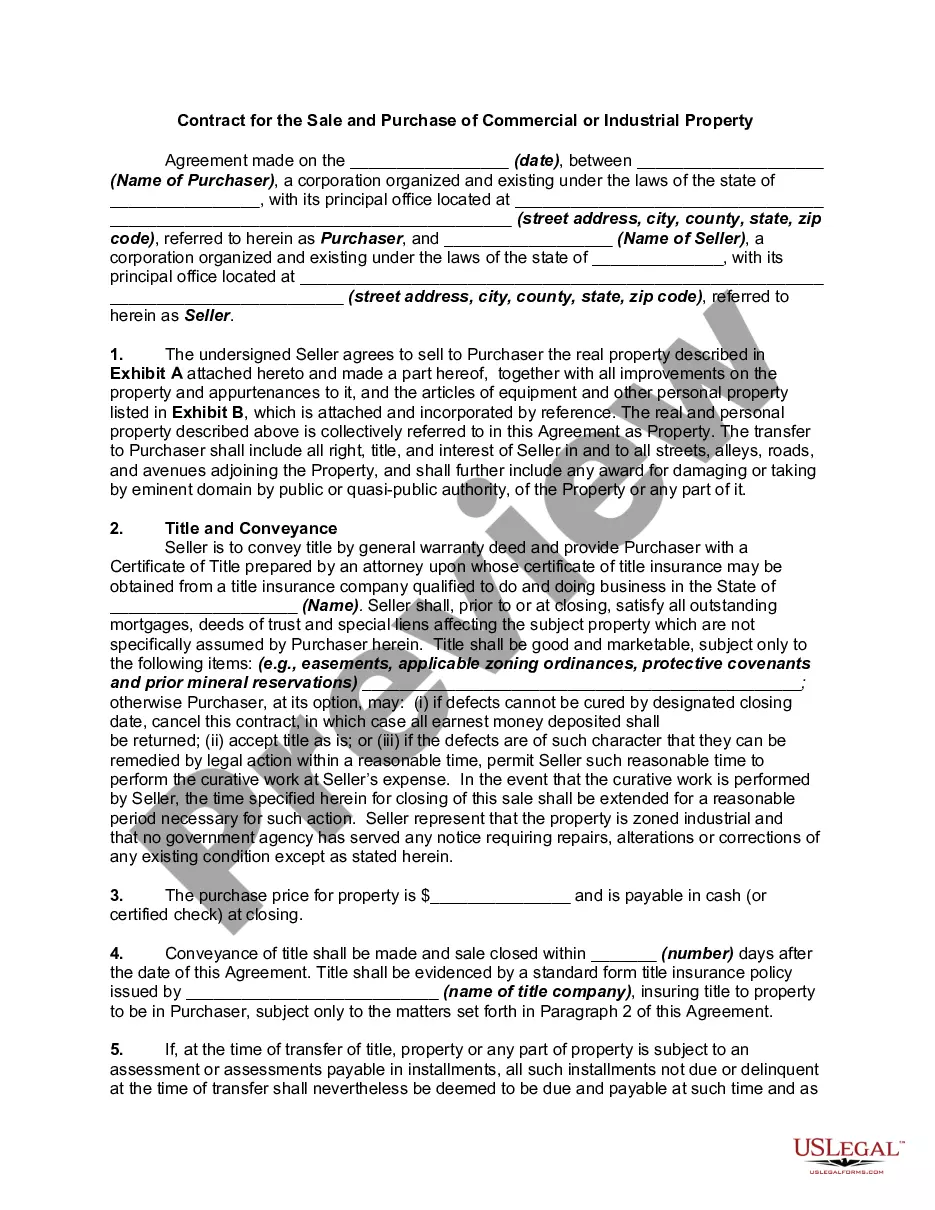

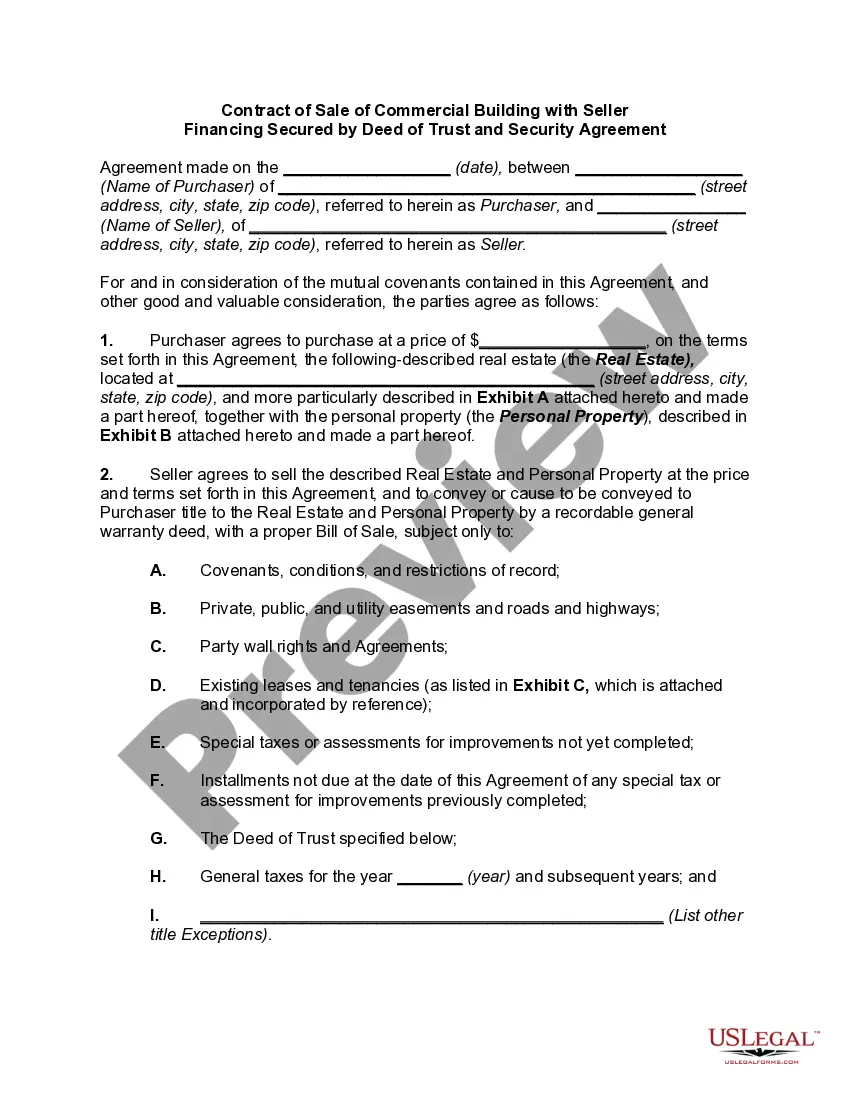

Contract to Sell Commercial Property with Commercial Building - Seller Financing Secured by Mortgage and Security Agreement

Overview of this form

This Contract to Sell Commercial Property with Commercial Building - Seller Financing Secured by Mortgage and Security Agreement is a legal document used to facilitate the sale of commercial real estate. This form outlines the terms of the sale, including seller financing, conditions of conveyance, and restrictions that may apply to the property. It differs from standard sales contracts by including provisions for seller financing and securing the agreement with a mortgage and security agreement.

Key components of this form

- Date and parties involved: Includes sections for the date of agreement and details of both the seller and purchaser.

- Property description: Specifies the real estate being purchased and includes a legal description.

- Purchase price and payment terms: Clearly outlines the financial agreement, including earnest money and buyer's obligations.

- Closing conditions: Details the date and arrangements for closing the sale.

- Warranties and representations: Seller's assurances regarding title and property condition, ensuring no undisclosed violations.

- Governing law and notices: Includes provisions determining the governing jurisdiction and how notices should be communicated.

When to use this form

This form is ideal for use when a seller is financing the purchase of their commercial property. It is particularly useful in situations where the purchaser may not have immediate access to traditional financing options, allowing the seller to retain some control over the financing process. Additionally, it's beneficial when both parties agree on the terms of the sale while acknowledging existing liens or encumbrances on the property.

Intended users of this form

- Sellers of commercial property who wish to offer financing options.

- Purchasers seeking to buy commercial real estate with seller financing.

- Real estate agents or brokers involved in commercial transactions.

- Attorneys or legal advisors assisting clients in commercial real estate deals.

Completing this form step by step

- Identify the parties: Enter the names and addresses of both the seller and purchaser.

- Specify the property: Clearly describe the property being sold, including its legal description and any personal property involved in the sale.

- Enter the financial terms: Fill in the purchase price, earnest money amount, and payment terms for the buyer.

- Detail the closing information: Specify the date, time, and location for the closing of the sale.

- Sign and date the agreement: Ensure all parties sign the contract and date it as required.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Leaving fields blank: Ensure all sections are completed to avoid disputes.

- Not specifying legal descriptions clearly: Incomplete descriptions can lead to confusion about the property being sold.

- Failing to include closing conditions: Omitting vital details can delay the transaction.

- Incorrectly calculating payment terms: Double-check figures to ensure accuracy.

Benefits of completing this form online

- Convenience: Access form templates anytime and from anywhere.

- Editability: Easily customize the form to meet your specific needs.

- Reliability: Utilize professionally drafted forms that comply with common legal standards.

Looking for another form?

Form popularity

FAQ

In seller financing, the seller takes on the role of the lender. Instead of giving cash to the buyer, the seller extends enough credit to the buyer for the purchase price of the home, minus any down payment. The buyer and seller sign a promissory note (which contains the terms of the loan).

The seller financing addendum outlines the terms at which the seller of the property agrees to loan the money to the buyer in order to purchase their property.Once complete, this addendum should be signed and attached to the purchase agreement made between the parties.

The best way to find seller financing is to ask for it in every offer you make. Eventually you'll find a seller that would prefer the fixed payments to a taxable lump sum at closing.

Complete the addendum, including your name, the purchaser's name and a description of the property. Include the type of financing that you are providing, such as first mortgage, second mortgage or deed of trust. List the terms of the loan.

Once you choose to sell your business with seller or owner financing, your buyer will pay for a portion of the business upfront in cash. You'll finance the rest of the sale in the form of a loan. Your lawyer will draw up and file the terms of your loan in a promissory note, which is essentially a legally binding IOU.

In a contract for deed, often done with seller finance deals, the answer is a little complicated. The buyer holds "equitable" title, while the seller holds legal title.

A security agreement refers to a document that provides a lender a security interest in a specified asset or property that is pledged as collateral.In the event that the borrower defaults, the pledged collateral can be seized by the lender and sold.

A homeowner with a mortgage can offer seller-carried financing but it's sometimes difficult to actually do.Home sellers, looking to increase their buyer pools, might choose to offer seller-carried financing, even if they still have mortgages on their homes.