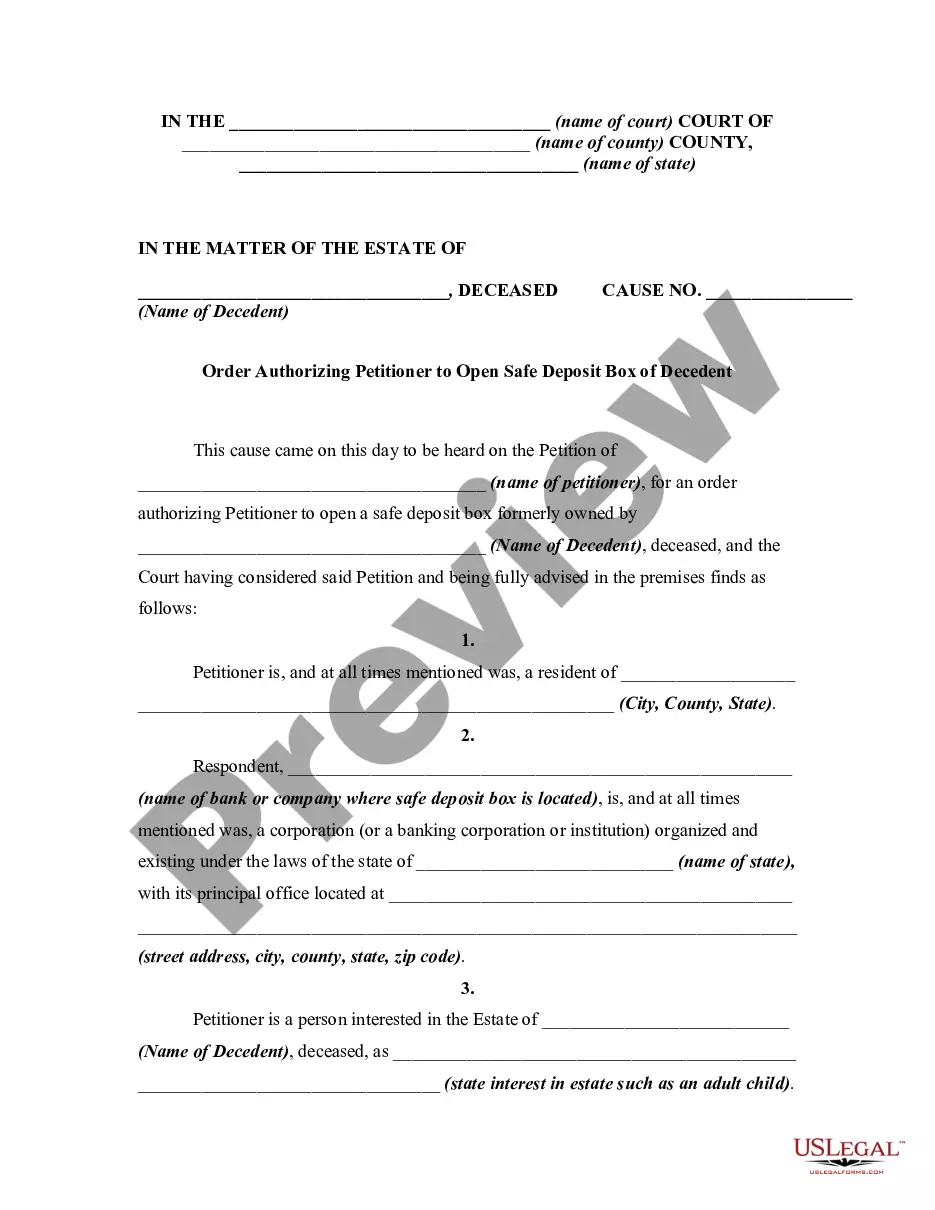

Petition For Order to Open Safe Deposit Box of Decedent

About this form

The Petition for Order to Open Safe Deposit Box of Decedent is a legal document used to request court authorization to access a deceased person's safe deposit box. This form is necessary when the bank or financial institution denies access, typically due to the absence of a will or other important documents within the box, and can help facilitate the discovery and proper handling of the deceased's final wishes regarding their estate.

Form components explained

- Petitioner's information, including name and address.

- Identification of the deceased and details of their safe deposit box.

- Statement of interest in the estate by the petitioner.

- Allegation of attempts to access the safe deposit box.

- Request for court order, including specific actions to be taken regarding the contents of the box.

Common use cases

This form should be used when you believe a deceased person has a safe deposit box containing important documents, such as a will, but you are unable to access it. This situation commonly arises when family members or the executor of the estate encounter resistance from the bank or institution managing the box. Utilizing this form can help streamline the process of gaining access to necessary estate planning documents.

Who should use this form

- Family members of the decedent, such as children or spouses.

- Executors or personal representatives designated to manage the estate.

- Individuals with a legal interest in the decedent's estate.

Completing this form step by step

- Identify yourself by entering your name, address, and relationship to the decedent.

- Provide the name of the deceased individual and details about their safe deposit box.

- Outline your interest in the estate clearly.

- Describe your attempts to access the safe deposit box and the bank's response.

- Submit the completed form to the appropriate court alongside any required fees and documentation.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, some jurisdictions may have unique requirements regarding notarization for court submissions. It's important to check your state's specific guidelines.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to accurately identify the deceased or the safe deposit box location.

- Omitting necessary details about your interest in the estate.

- Not including all required signatures and notarization, if applicable.

Why complete this form online

- Convenient access to the form 24/7.

- Easy editing capabilities to ensure all information is accurate.

- Reliable, attorney-drafted forms tailored to meet legal standards.

Legal use & context

- This petition is often required in probate proceedings to ensure that the decedent's wishes regarding their estate are honored.

- It is enforceable in court, helping to facilitate access to potentially critical documents for the estate's administration.

- Legal definitions and requirements vary by state, emphasizing the need for local legal knowledge when using this form.

Quick recap

- The petition allows access to a deceased personâs safe deposit box, necessary for estate management.

- Proper completion and notarization of the form are crucial for legal validity.

- Understanding state-specific laws is essential to ensure compliance and expedite the process.

Looking for another form?

Form popularity

FAQ

It asks the court for authority to open a decedent's safe deposit box when the bank won't grant access, usually because important documents are not inside. The form identifies the petitioner and decedent, describes the box, shows the petitioner's interest in the estate, and requests specific steps the court should take regarding the box's contents.

To open a decedent's safe deposit box after death, this form is used to petition the court for an order granting access when the bank has denied it. It includes the petitioner's information, identifies the decedent and box, states the petitioner's estate interest, describes attempts to access the box, and requests the court take action on the contents.

Yes, a bank may restrict access to a decedent’s safe deposit box. This form is designed to obtain a court order authorizing opening the box when access has been blocked, especially to retrieve documents or other estate-related items needed to manage the decedent's affairs.

Include the petitioner's information (name and address), identification of the deceased and the box, a statement of the petitioner's interest in the estate, factual allegations of attempts to access the box, and a precise request for the court order detailing the actions to be taken with the box's contents.

The form is intended for family members (such as children or spouses), executors or personal representatives, and anyone with a legal interest in the decedent's estate who needs to access a safe deposit box that's been blocked by a bank.

Compared with other probate forms, this Petition for Order to Open Safe Deposit Box of Decedent specifically seeks a court order to access a decedent's box when the bank has denied access, and it requires identifying the deceased, the box, the petitioner's estate interest, and the requested court-directed actions.