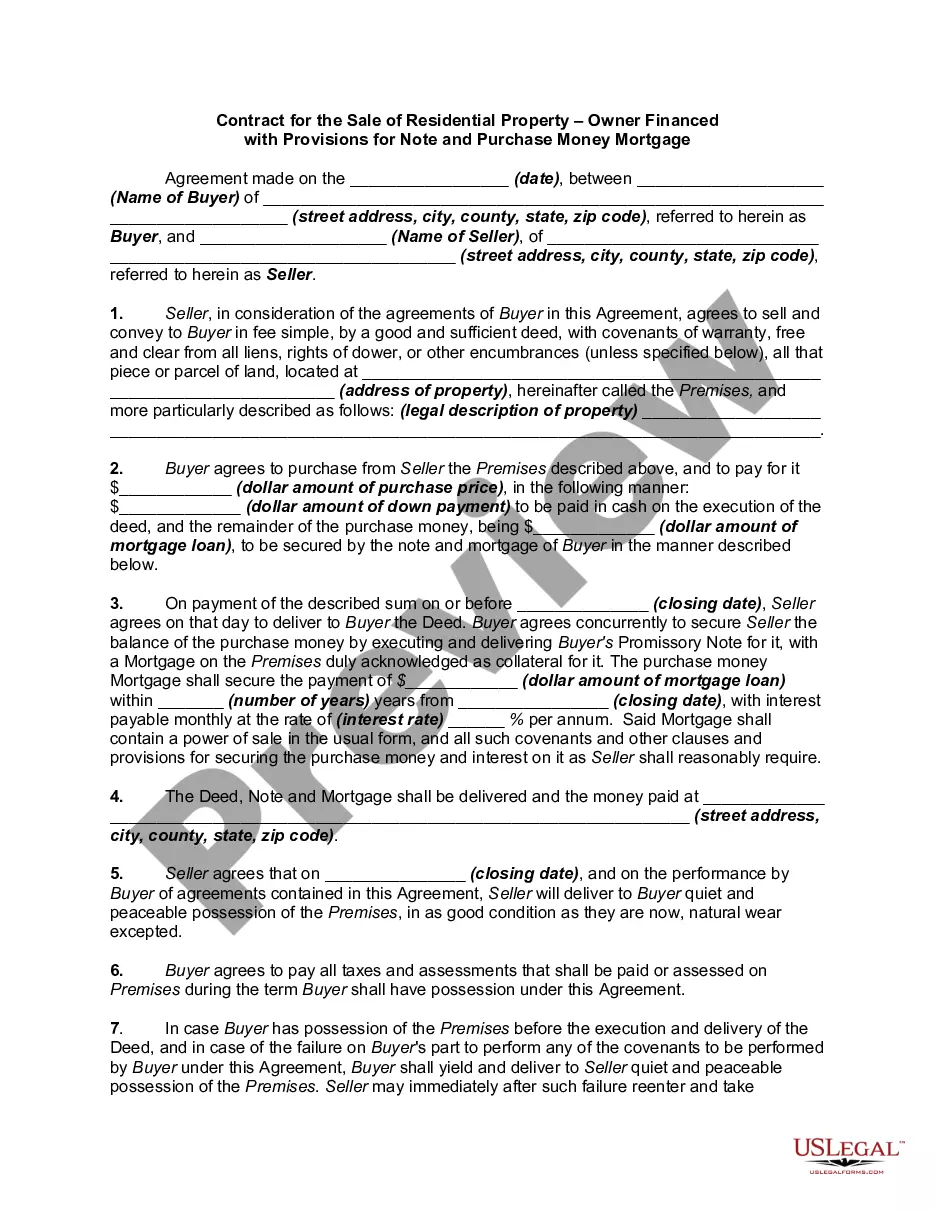

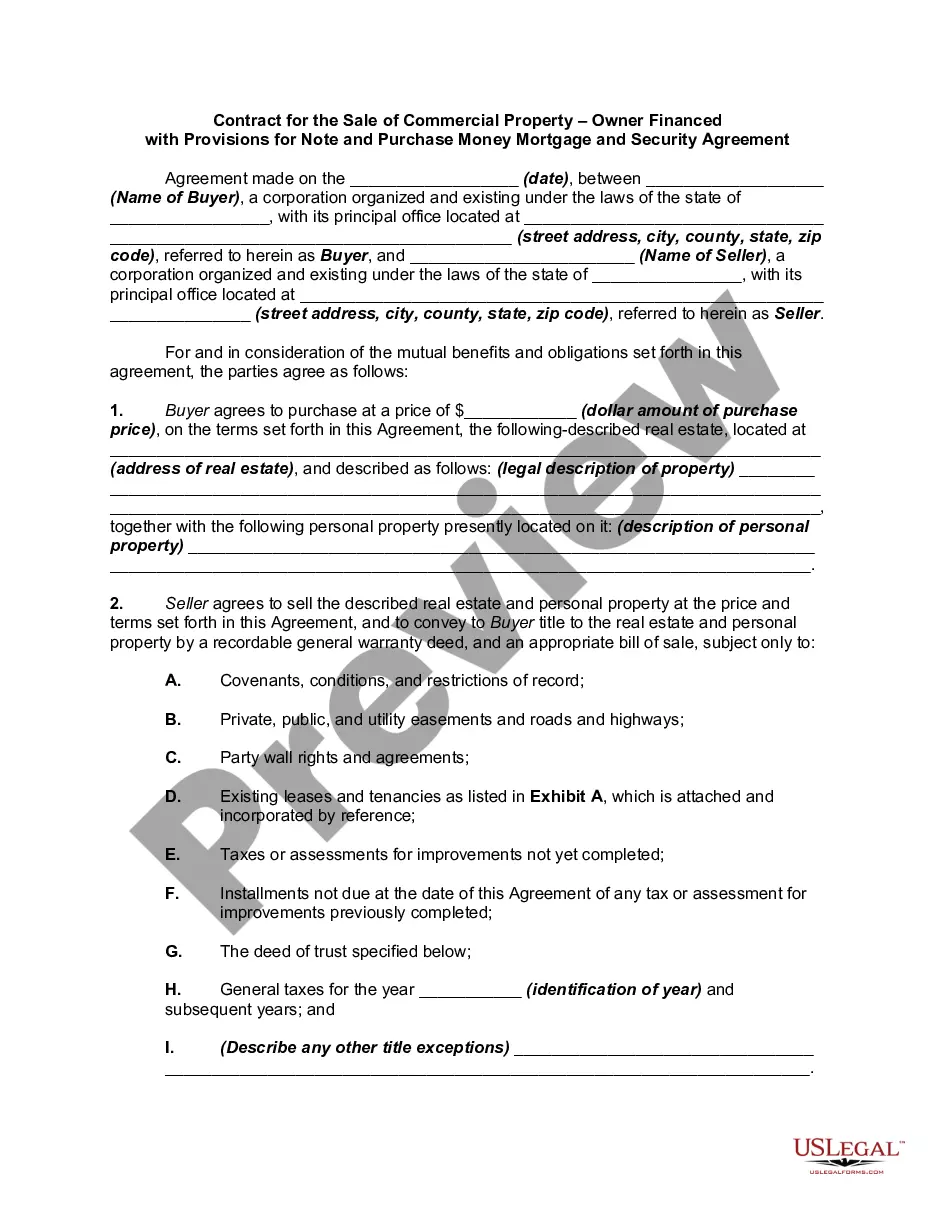

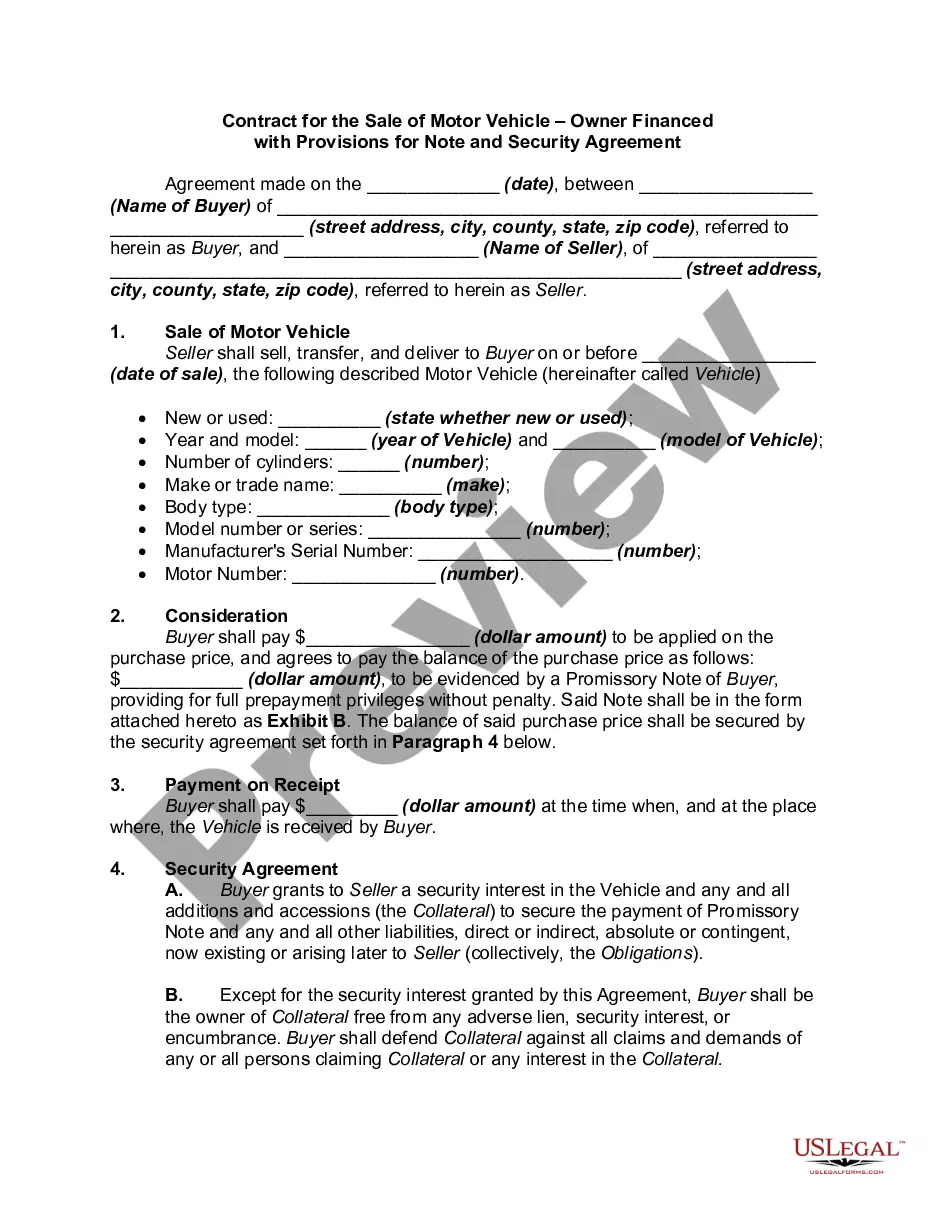

Contract for the Sale of Personal Property - Owner Financed with Provisions for Note and Security Agreement

What is this form?

The Contract for the Sale of Personal Property - Owner Financed with Provisions for Note and Security Agreement is a legal document outlining the sales agreement between a buyer and a seller for personal property, where financing is involved. This form establishes a security interest in the sold property, allowing the seller to reclaim the goods in case of buyer default. It is an essential tool for both parties to ensure clear terms of sale, payment, and rights regarding the collateral involved in the transaction.

Main sections of this form

- Date of the agreement and details of the buyer and seller.

- Description of the goods being sold.

- Payment terms, including the purchase price and specifics of the promissory note.

- Provisions for the security agreement and what constitutes collateral.

- Warranties regarding the condition and title of the goods.

- Provisions for risk of loss and the right of inspection by the buyer.

When this form is needed

This form should be utilized when you are purchasing personal property and require owner financing, ensuring a formal agreement is in place that protects the seller's interests with a security interest in the property. It is ideal for transactions involving items such as vehicles, machinery, or other significant assets where the buyer cannot pay the full price upfront.

Who this form is for

- Individuals or businesses looking to sell personal property while providing financing options to buyers.

- Buyers needing to finance the purchase of personal property through an installment plan.

- Parties wanting to clearly outline payment and security terms related to the sale.

How to complete this form

- Identify the date and fill in the names and addresses of both the buyer and seller.

- Provide a clear description of the personal property being sold.

- Specify the purchase price and outline the payment terms, including the amounts and form of the promissory note.

- Detail any necessary signatures and initial notices of rights and inspection.

- Review and ensure all provisions regarding security interests and warranties are completed correctly.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. It is essential to check local requirements to ensure compliance with any state-specific rules regarding notarization of contracts.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately describe the goods being sold.

- Omitting crucial payment terms or the amount of the promissory note.

- Not including the security interest provisions clearly in the agreement.

- Neglecting to have both parties sign the document.

Why complete this form online

- Immediate access to professionally drafted legal documents.

- Convenience of filling out and downloading the form anytime.

- Editability allows for customization to fit specific transaction needs.

- Reliability, knowing the form meets current legal standards.

Legal use & context

- This form provides a comprehensive framework for the sale of personal property while ensuring the seller's investment is protected.

- In the event of default, the security interest allows the seller to recover the goods without lengthy legal proceedings.

- The terms laid out in this agreement can help in avoiding potential legal disputes related to the sale.

Summary of main points

- The form facilitates the sale of personal property with owner financing.

- It includes essential components such as payment terms and security interests.

- Proper completion and understanding of this form can prevent misunderstandings between buyer and seller.

Looking for another form?

Form popularity

FAQ

Owner financing is a transaction in which a property's seller finances the purchase directly with the person or entity buying it, either in whole or in part. This type of arrangement can be advantageous for both sellers and buyers because it eliminates the costs of a bank intermediary.

There is no legal requirement that a lender charge interest. However, the failure to charge interest on an owner-financed sale or real property may bring into question for tax purposes whether the transfer was a legitimate sale or a gift.

The best way to find seller financing is to ask for it in every offer you make. Eventually you'll find a seller that would prefer the fixed payments to a taxable lump sum at closing.

When you sell with owner financing and report it as an installment sale, it allows you to realize the gain over several years. Instead of paying taxes on the capital gains all in that first year, you pay a much smaller amount as you receive the income. This allows you to spread out the tax hit over many years.

Interest rates for seller-financed loans are typically higher than what traditional lenders would offer. The seller takes on some risk by holding financing, and he or she may charge a higher interest rate to offset this risk. It's not uncommon to see interest rates from 4% to 10%. They could be higher, too.

In a contract for deed, often done with seller finance deals, the answer is a little complicated. The buyer holds "equitable" title, while the seller holds legal title.

In seller financing, the seller takes on the role of the lender. Instead of giving cash to the buyer, the seller extends enough credit to the buyer for the purchase price of the home, minus any down payment. The buyer and seller sign a promissory note (which contains the terms of the loan).

While it's not common, seller financing can be a good option for buyers and sellers under the right circumstances. Still, there are risks for both parties that should be weighed before signing any contracts.

The average down payment for residential properties on seller-financed loans in 2018 was 19%. While there are ways to buy or sell a property with zero or very little money down, this is rare. In most circumstances, sellers require 10% to 20% down, although there's no minimum requirement.