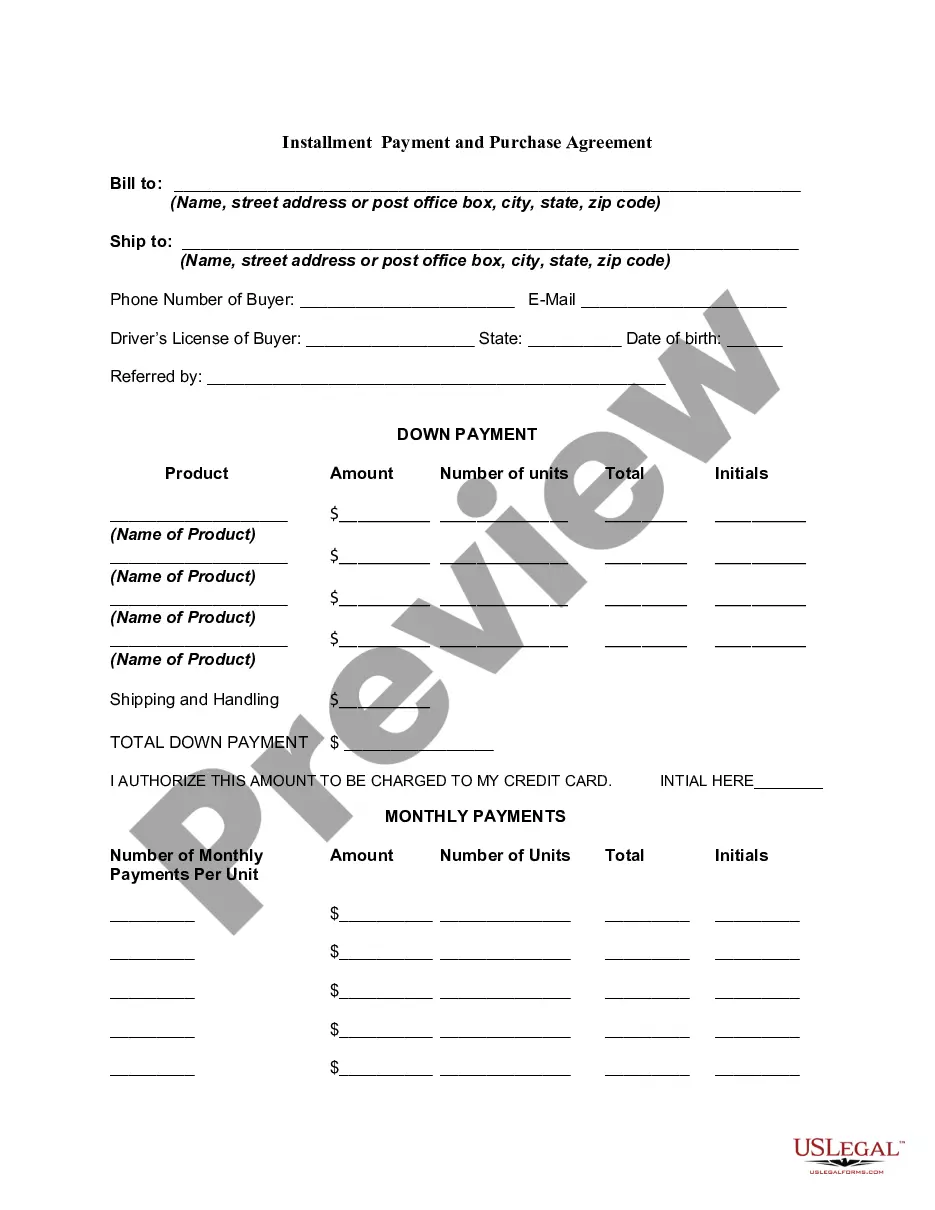

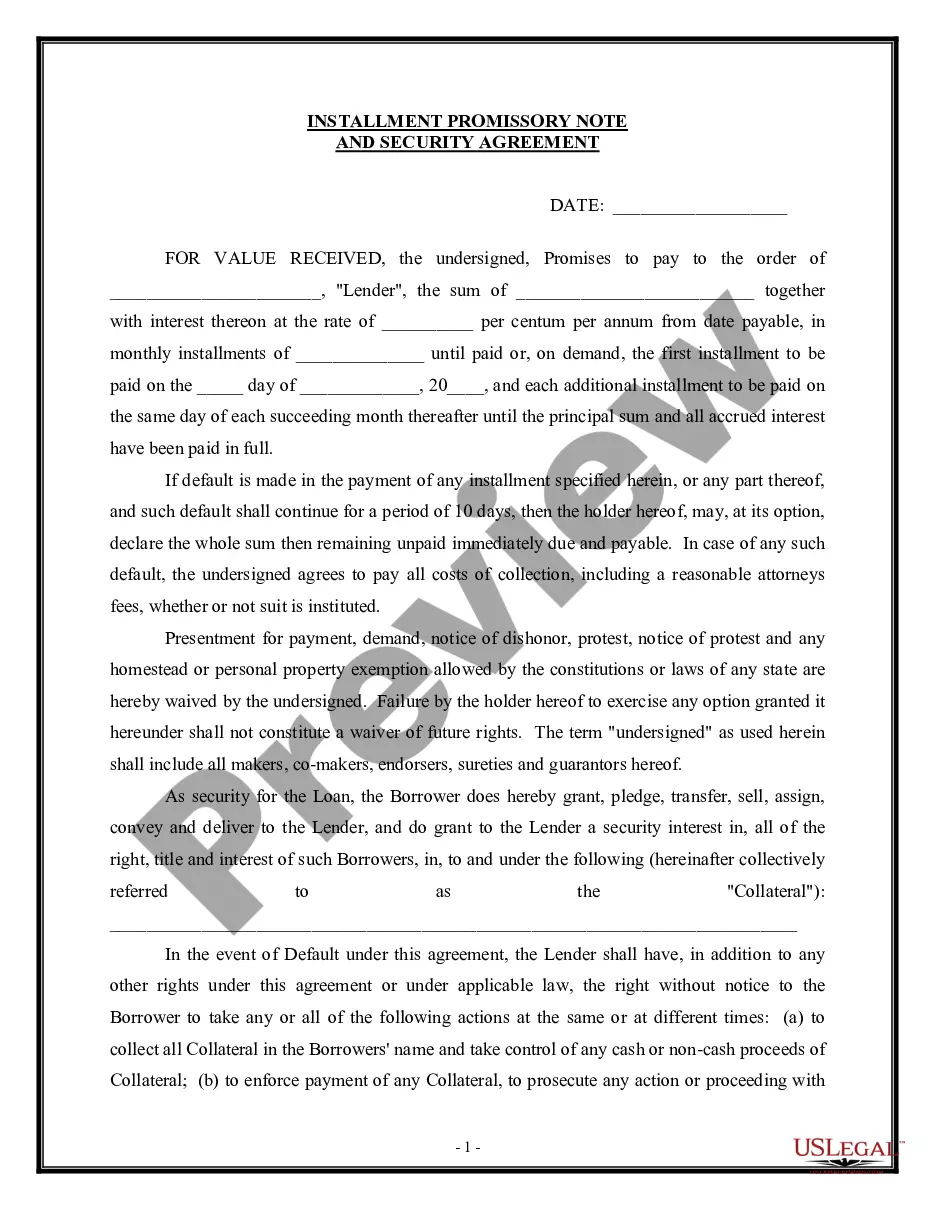

Installment Promissory Note with Acceleration Clause and Collection Fees

Understanding this form

An Installment Promissory Note with Acceleration Clause and Collection Fees is a legal document used to record a borrower's promise to repay a loan amount in installments. This form is essential for situations where a lender wants to set conditions for payment, including late fees and the option to accelerate the full amount owed if the borrower defaults. It provides clear terms for both parties, ensuring that the lender has a legal framework to seek repayment if necessary.

Main sections of this form

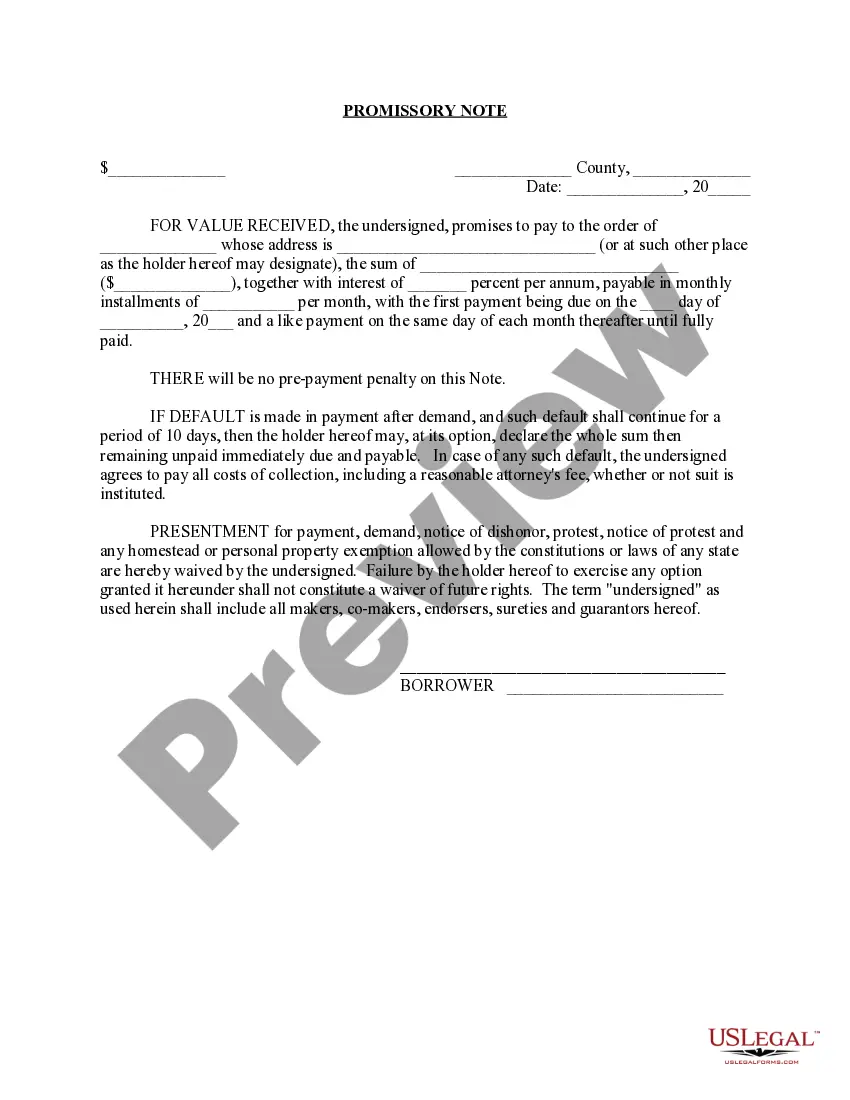

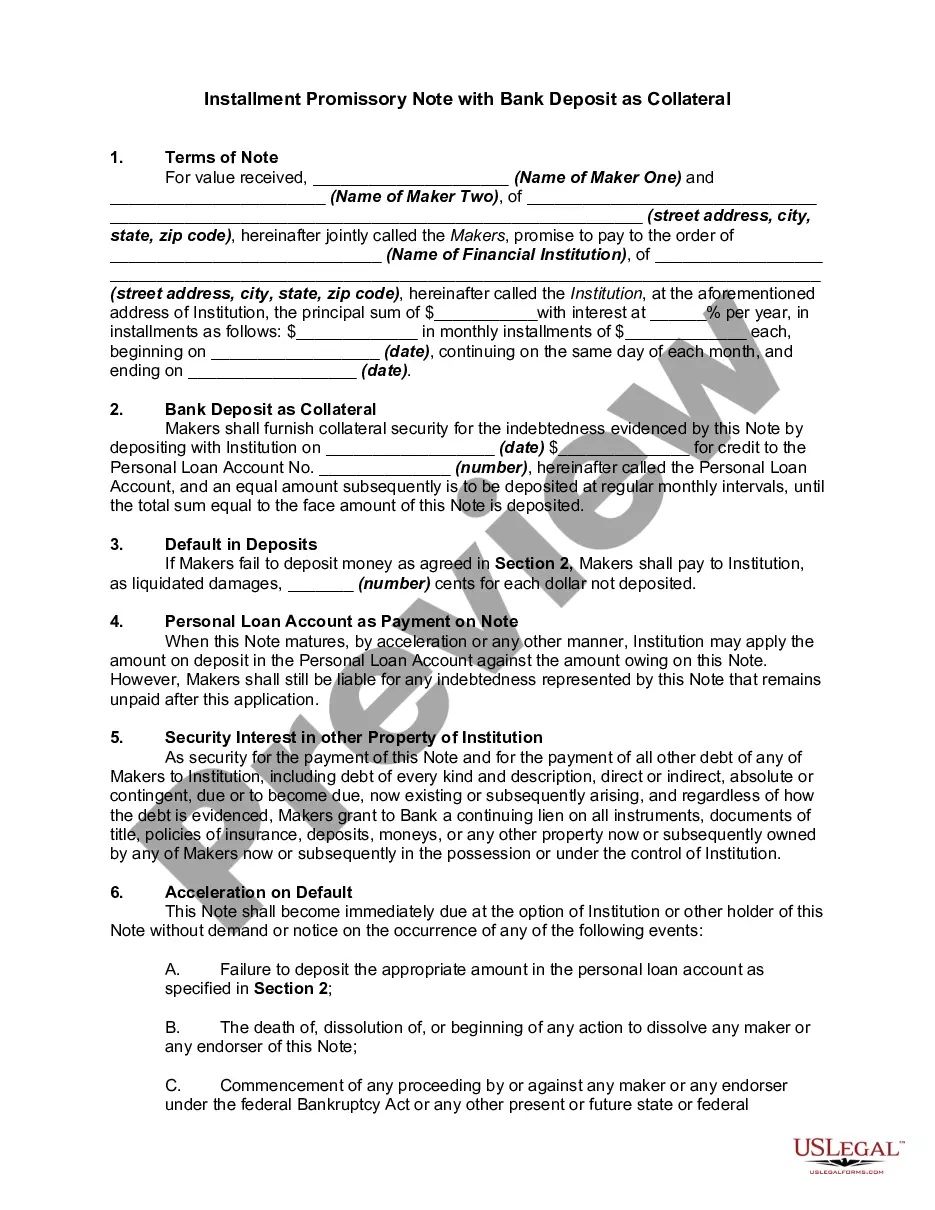

- Amount of Note: The total principal amount being borrowed.

- Date of Execution: The date when the note is signed.

- Names of the Parties: Identification of both the maker (borrower) and payee (lender).

- Installment Payment Schedule: Details on the number and amount of monthly payments.

- Interest Rate: The percentage charged on the unpaid balance of the loan.

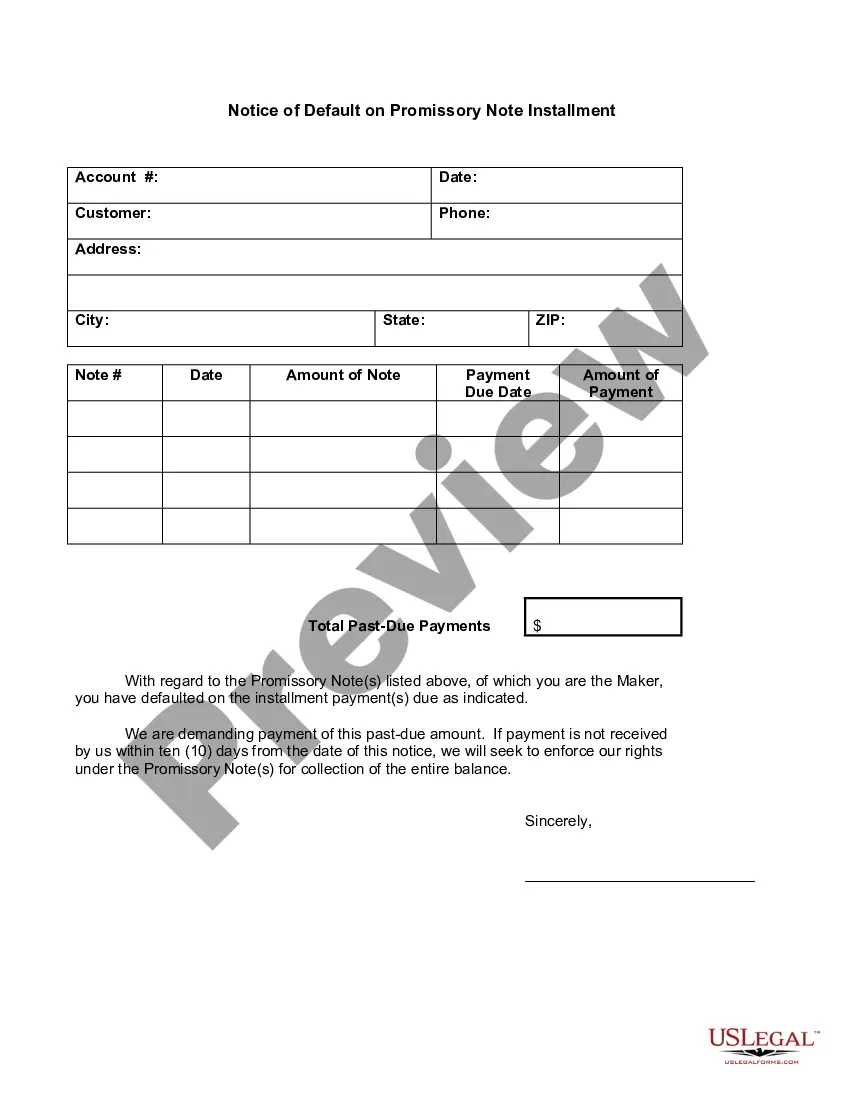

- Acceleration Clause: Conditions under which the lender can demand full repayment if the borrower defaults.

- Collection Fees: Additional charges incurred if there is a delay in payment.

When this form is needed

This form is typically used when a borrower seeks to finance a purchase or loan through installments. It is valuable when the terms of repayment are significant, such as for significant purchases like vehicles, appliances, or personal loans. This note is particularly useful when a lender wishes to formalize the lending agreement, including fees for late payments and the right to demand full repayment under specific conditions.

Who needs this form

- Lenders who want to clearly outline repayment terms for a loan.

- Borrowers seeking to formalize an agreement for borrowing money.

- Individuals or small businesses involved in installment sales.

Steps to complete this form

- Identify the parties involved: enter the names of the borrower and lender.

- Specify the loan amount: clearly state the total amount borrowed.

- Set the interest rate: write the percentage the borrower will be charged.

- Fill in the installment details: indicate the number and amount of monthly payments.

- Provide relevant dates: note the date of execution and the due date for the first installment.

- Have all parties sign and date the document to finalize the agreement.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having the document notarized can enhance its credibility and provide an additional layer of protection in case of disputes.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to specify the correct interest rate.

- Not including the exact amount of the installment payments.

- Omitting signatures from all required parties.

- Leaving out important dates, which may affect enforceability.

- Not understanding the implications of the acceleration clause.

Benefits of completing this form online

- Convenience of downloading and printing the form from home.

- Editability to customize the terms to fit specific needs.

- Access to forms drafted by licensed attorneys, ensuring legal soundness.

- Time-saving as the templates are ready for immediate use.

Legal use & context

- This form creates a legally binding obligation to repay the borrowed amount.

- Actionable provisions in the document clarify the rights and responsibilities of each party.

- Properly executed, this form can be enforced in a court of law, protecting both lender and borrower interests.

Main things to remember

- The Installment Promissory Note outlines clear repayment terms, protecting both parties.

- It is essential to adhere to local laws when executing this form.

- Using this template can simplify the loan process for both borrowers and lenders.

Looking for another form?

Form popularity

FAQ

In order for a promissory note to be valid, both the lender and the borrower must sign the documentation. If you are a co-signer for the loan, you are required to sign the promissory note. Being a co-signer requires you to repay the loan amount in the instance that the borrower defaults on payment.

Step 1 Agree to Terms. Step 2 Run a Credit Report. Step 3 Security and Co-Signer(s) Step 4 Writing the Promissory Note. Step 5 Paying Back the Borrowed Money. Calculating Total Interest Owed. Calculating the Final Payment Amount. Calculating the Monthly Payment Amount.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Writing the Promissory Note Terms You don't have to write a promissory note from scratch. You can use a template or create a promissory note online.

Navigate to the website: www.studentloans.gov. Click "Log In." Enter your FSA ID and Password. Click "Complete Master Promissory Note." Select the appropriate loan type. Enter Your Personal Information.

Types of Property that can be used as collateral. Speak to them in person. Draft a Demand / Notice Letter. Write and send a Follow Up Letter. Enlisting a Professional Collection Agency. Filing a petition or complaint in court. Selling the Promissory Note. Final Tips.

If the borrower does not repay you, your legal recourse could include repossessing any collateral the borrower put up against the note, sending the debt to a collection agency, selling the promissory note (so someone else can try to collect it), or filing a lawsuit against the borrower.

Keep the original promissory note. Once a lender executes a promissory note, he keeps the original of the promissory note. Accept full payment of the loan. Mark paid in full on the promissory note. Place a signature beside the paid in full notation. Mail the original promissory note to the borrower.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.