This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Purchase Money Mortgage Template

Instant download

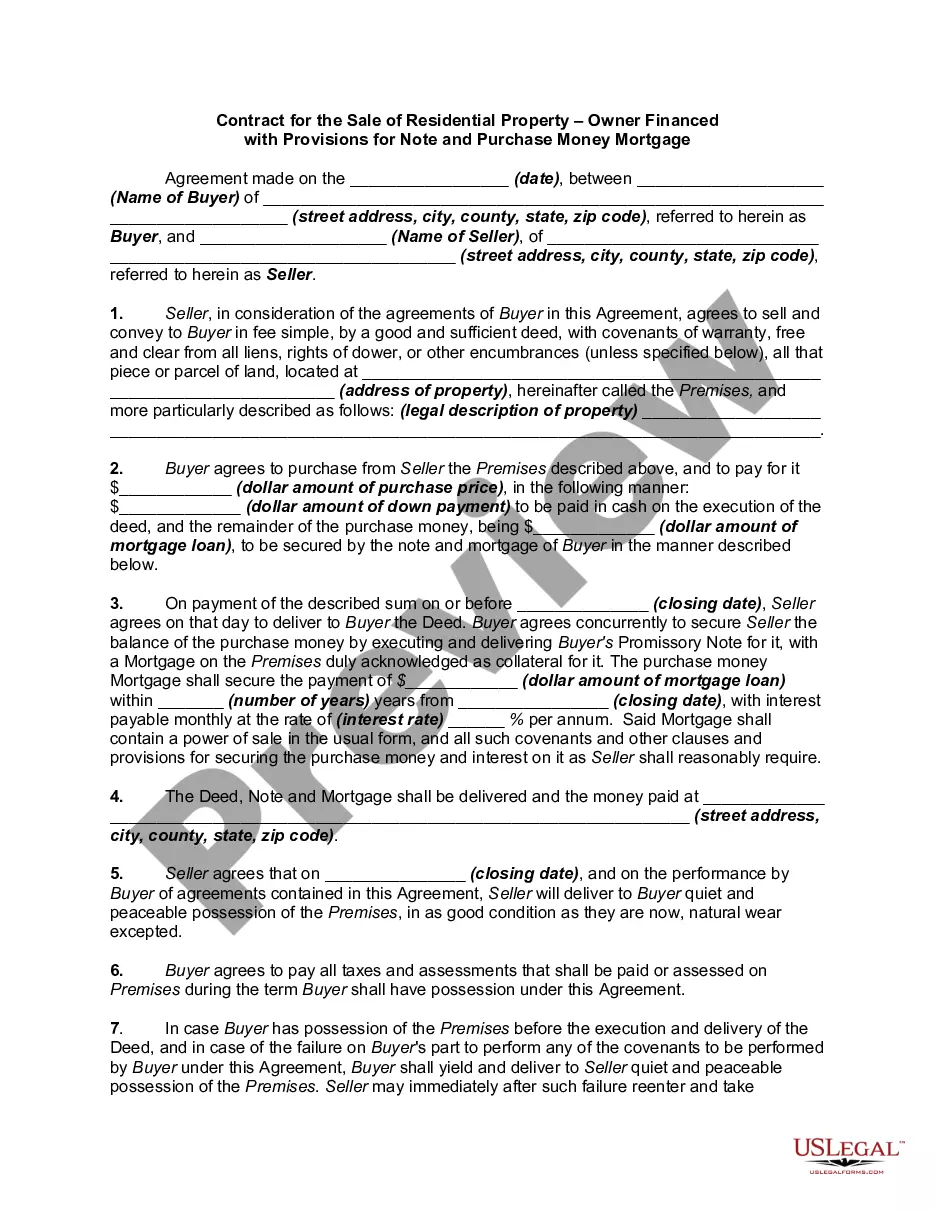

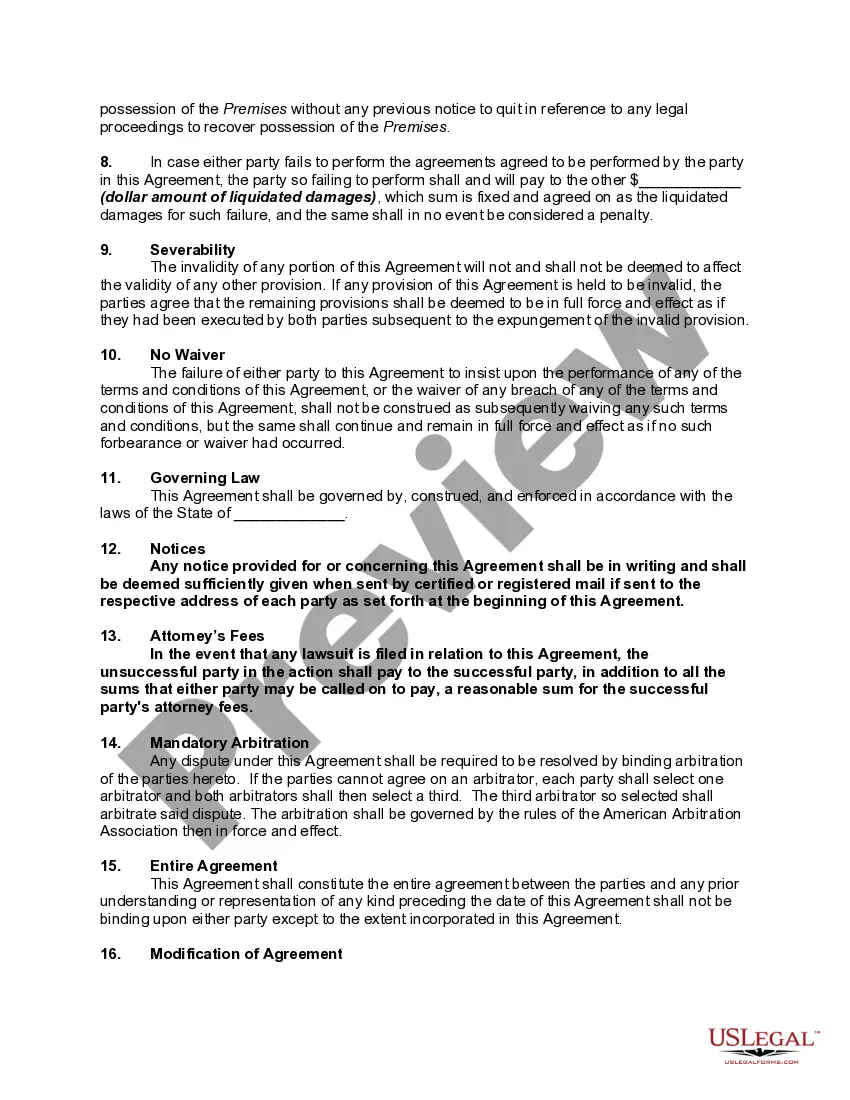

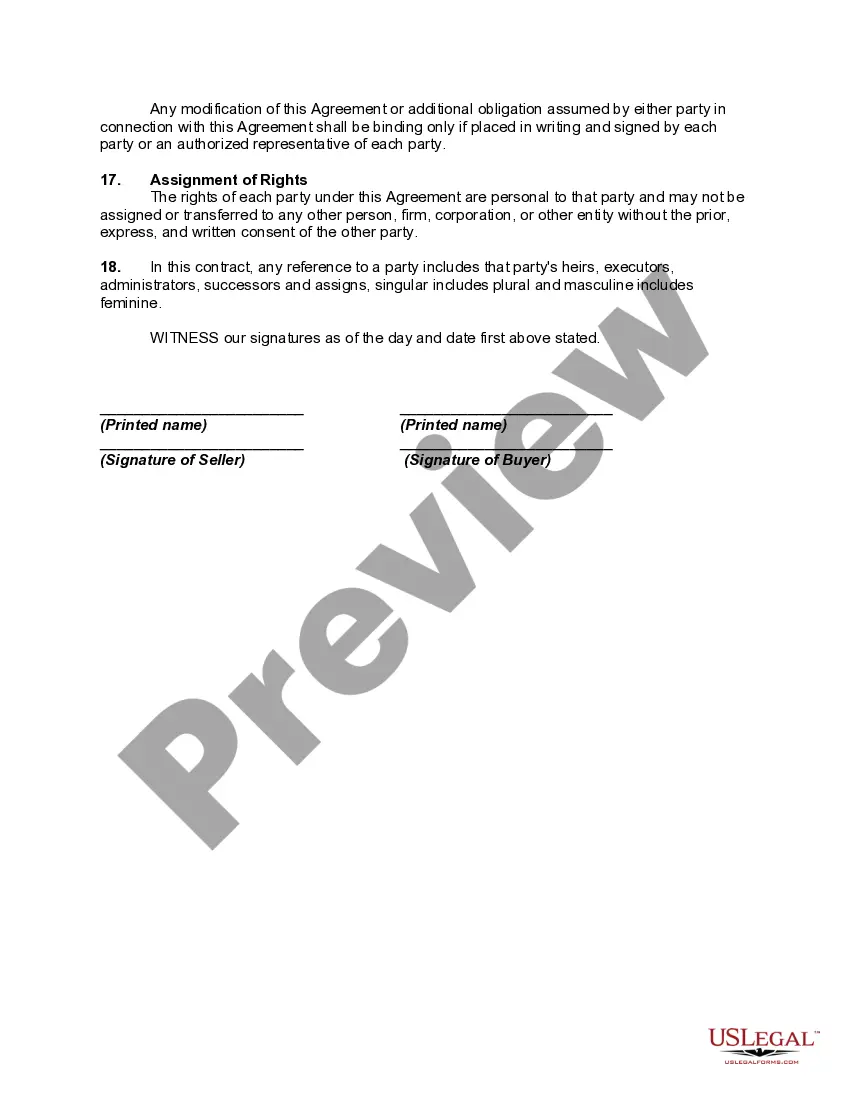

Description For Sale By Owner Contract

Free preview Purchase Money Mortgage

How to fill out Note Money Mortgage Form Pdf?

Aren't you sick and tired of choosing from countless templates every time you need to create a Contract for the Sale of Residential Property - Owner Financed with Provisions for Note and Purchase Money Mortgage? US Legal Forms eliminates the wasted time numerous American citizens spend searching the internet for appropriate tax and legal forms. Our expert team of lawyers is constantly changing the state-specific Forms library, to ensure that it always provides the appropriate documents for your situation.

If you’re a US Legal Forms subscriber, simply log in to your account and then click the Download button. After that, the form may be found in the My Forms tab.

Users who don't have an active subscription need to complete easy actions before having the capability to get access to their Contract for the Sale of Residential Property - Owner Financed with Provisions for Note and Purchase Money Mortgage:

- Utilize the Preview function and read the form description (if available) to be sure that it’s the right document for what you’re trying to find.

- Pay attention to the applicability of the sample, meaning make sure it's the right template for your state and situation.

- Use the Search field at the top of the web page if you want to look for another file.

- Click Buy Now and select a convenient pricing plan.

- Create an account and pay for the services using a credit card or a PayPal.

- Download your sample in a required format to complete, print, and sign the document.

When you have followed the step-by-step instructions above, you'll always be able to sign in and download whatever file you will need for whatever state you want it in. With US Legal Forms, completing Contract for the Sale of Residential Property - Owner Financed with Provisions for Note and Purchase Money Mortgage templates or any other legal paperwork is easy. Get going now, and don't forget to double-check your samples with accredited lawyers!