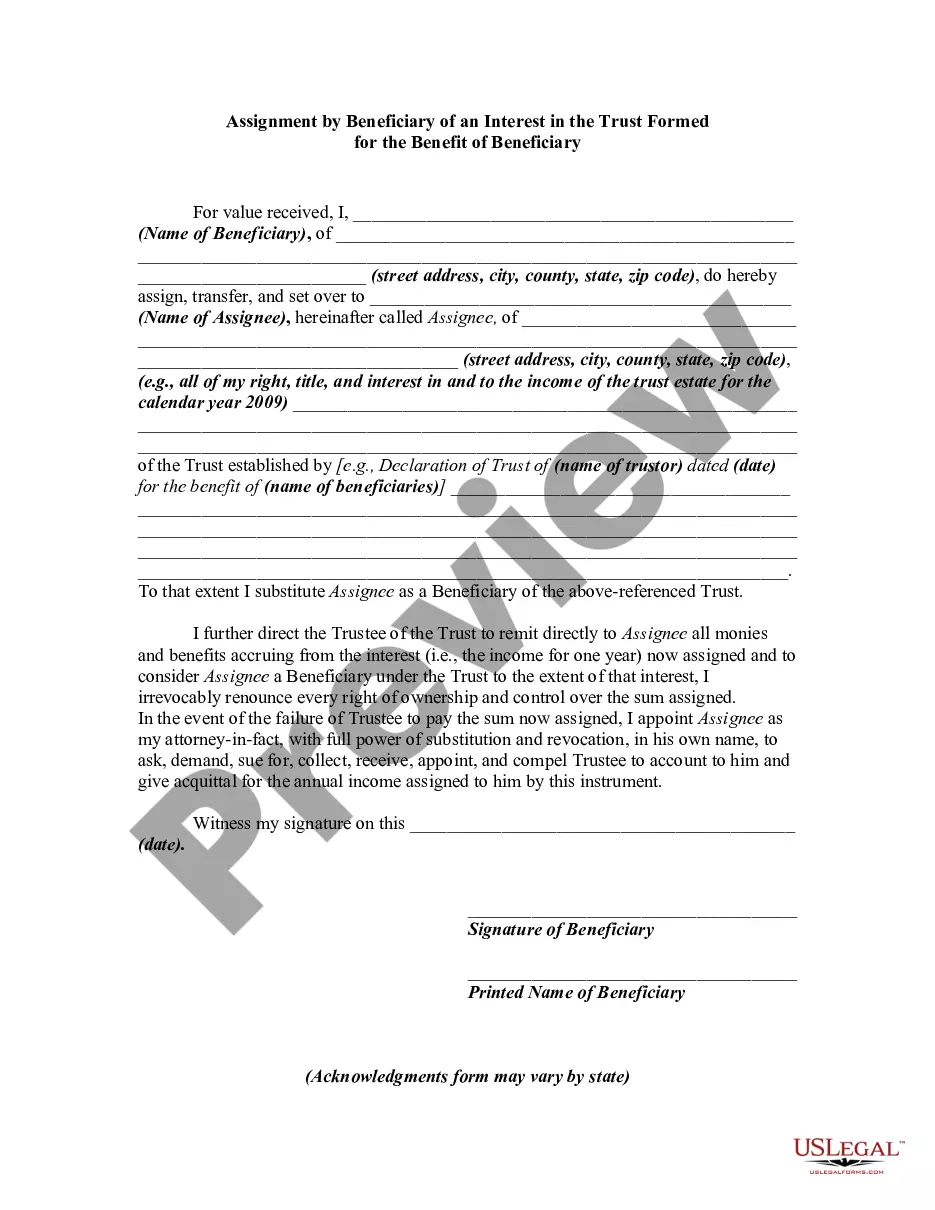

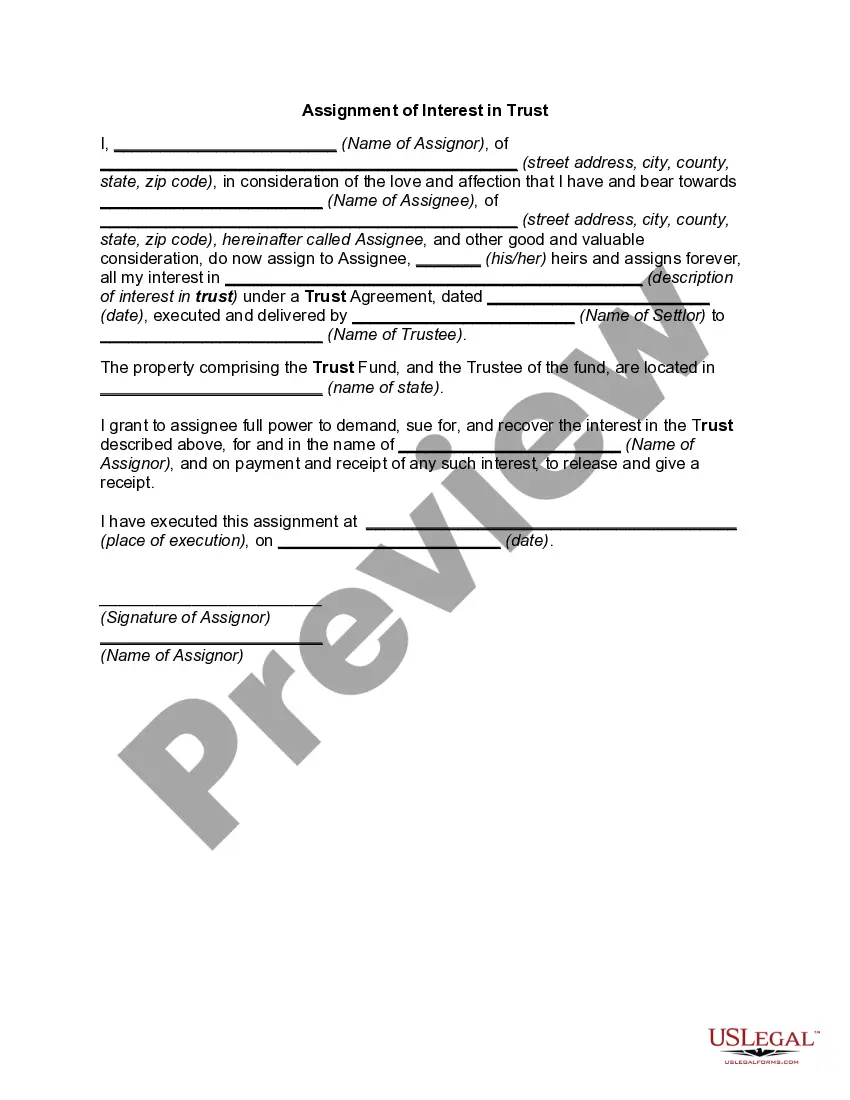

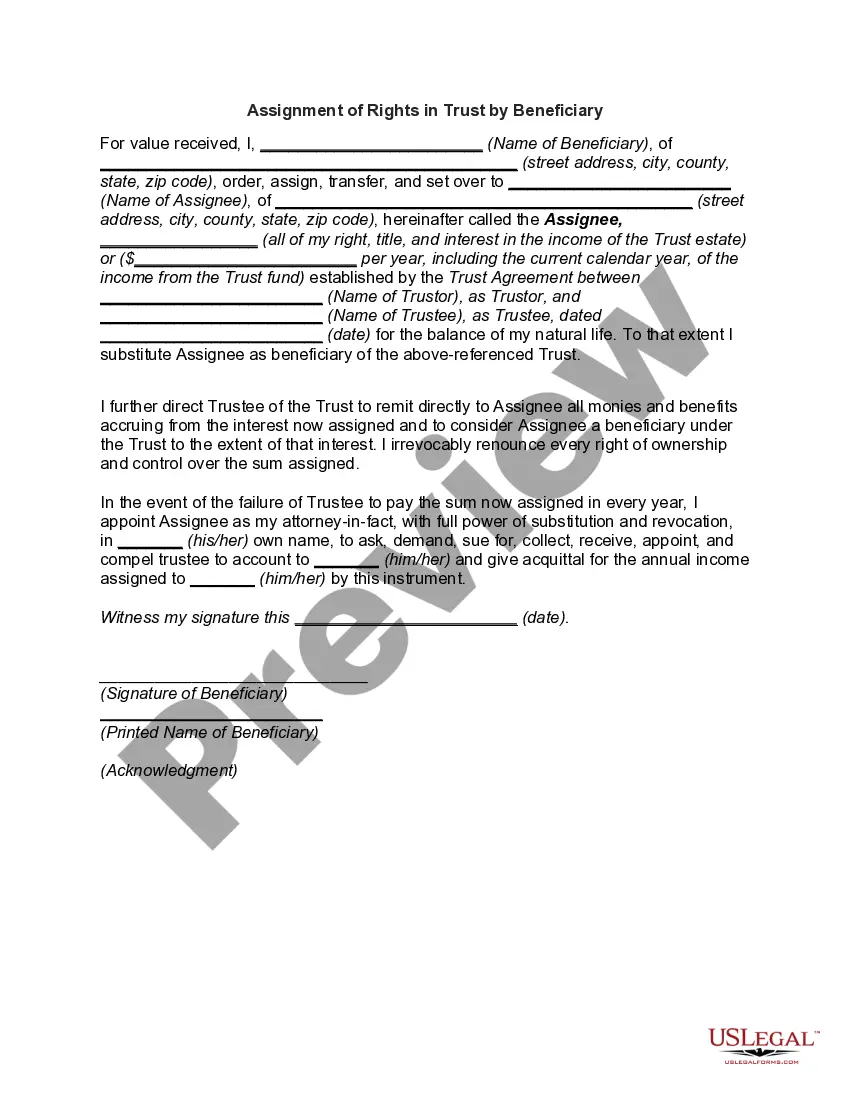

Assignment by Beneficiary of a Percentage of the Income of a Trust

Understanding this form

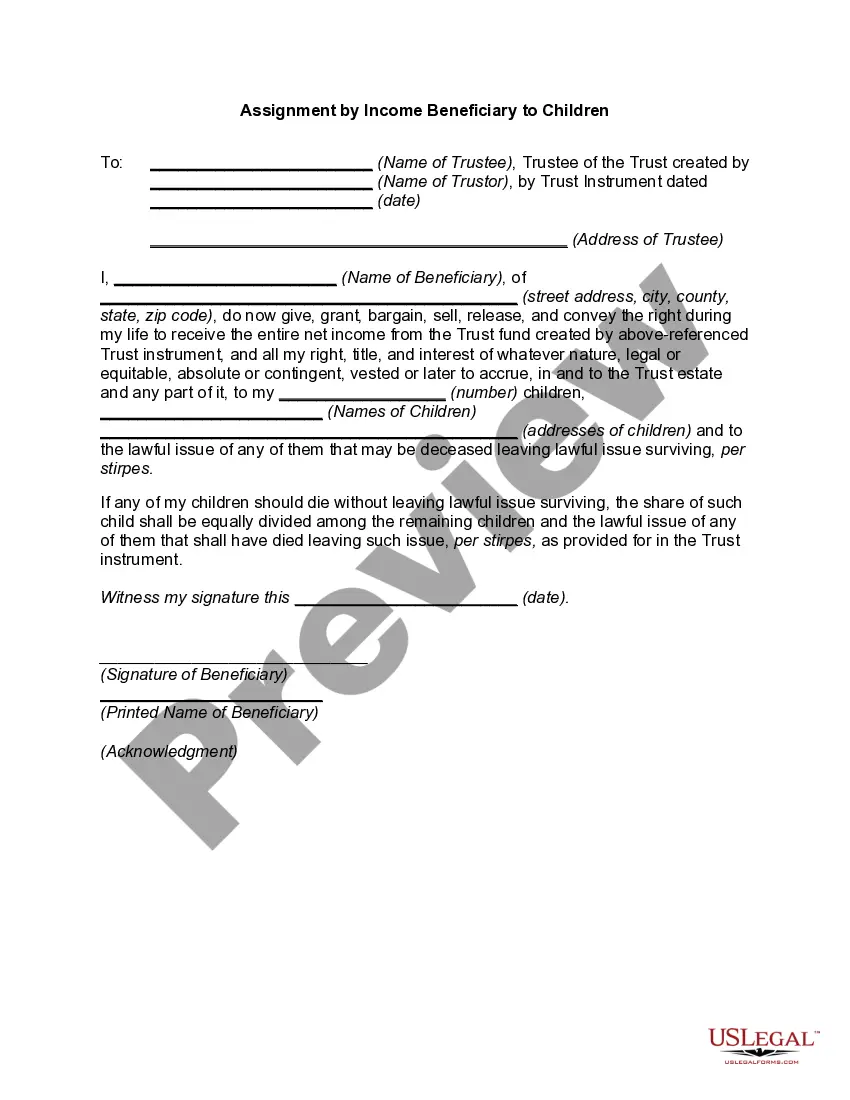

The Assignment by Beneficiary of a Percentage of the Income of a Trust is a legal document that allows a trust beneficiary to transfer a portion of their interest in a trust to another party. This form specifically addresses the assignment of rights to income generated by a trust, distinguishing it from similar agreements that may involve outright property transfers. Understanding this form is crucial for beneficiaries wanting to manage or reallocate their income from a trust effectively.

Key parts of this document

- Identification of the beneficiary assigning their interest.

- Details of the income and benefits being assigned.

- Information about the assignee receiving the interest.

- Specification of the trust involved, including the trustee's details.

- Signature of the beneficiary and acknowledgment by a notary public.

Situations where this form applies

This form is needed when a beneficiary of a trust wishes to transfer a portion of their income rights to another individual or entity. Common scenarios include financial planning strategies, such as providing support to family members, or when the original beneficiary seeks to convert a future income stream into immediate cash by assigning their rights.

Who should use this form

- Beneficiaries of trusts who wish to assign a portion of their income rights.

- Individuals seeking to restructure their income from a trust for financial reasons.

- Legal representatives managing the interests of beneficiaries in trusts.

Completing this form step by step

- Identify the beneficiary by entering their full name and address.

- Specify the assignee by entering their name and address.

- Detail the trust, including the name of the trustor and the trustee.

- Indicate the percentage or amount of income being assigned.

- Sign and date the form in the presence of a notary public.

Does this document require notarization?

Yes, this form must be notarized to be legally valid. This ensures that the signature of the beneficiary is verified, preventing potential disputes about the authenticity of the assignment. With US Legal Forms, you can easily utilize integrated online notarization, offering 24/7 availability and secure video calls for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to clearly identify the parties involved.

- Not specifying the exact percentage of income being assigned.

- Omitting the trustee's information from the form.

- Neglecting to sign the form or have it notarized.

Why use this form online

- Convenience of downloading and filling the form at your own pace.

- Editability allows for easy adjustments to suit your specific needs.

- Access to legally vetted templates ensures compliance with relevant laws.

Legal use & context

- This form formally assigns a portion of trust income, making it enforceable under law.

- Notarization adds a layer of security, ensuring legal integrity.

- Assignments may be subject to trustee approval as per the trust agreement.

Key takeaways

- The assignment allows beneficiaries to transfer their income rights from a trust.

- Completing the form correctly ensures legal validity and clarity of intent.

- Consult state laws to ensure compliance and understand implications.

Looking for another form?

Form popularity

FAQ

An allocation rate is a percentage of an investor's cash or capital outlay that goes toward a final investment. The allocation rate most often refers to the amount of capital invested in a product net of any fees that may be incurred through the investment transaction.

If you have more than one life insurance beneficiary, you can allocate how much each person or entity will receive. These are known as beneficiary allocation rules. For instance, if you have two children, you could state that each will receive 50% of the total amount.

Usually, a trust prohibits beneficiaries from assigning their interest in the trust before distribution. The anti-assignment provision protects undistributed trust assets from claims by a beneficiary's creditors.

Your primary beneficiary is first in line to receive your death benefit. If the primary beneficiary dies before you, a secondary or contingent beneficiary is the next in line. Some people also designate a final beneficiary in the event the primary and secondary beneficiaries die before they do.

Each beneficiary is designated a specific percentage of the money, adding up to 100%. A contingent beneficiary receives assets in the same manner stated for the primary beneficiary.

Write only one beneficiary on each line. Make sure that you write the full names of all beneficiaries. For example, if you name you children as beneficiaries, DO NOT merely write children on one of the lines; instead write the full names of each of your children on separate lines.

In general, most people name one or two primary beneficiaries, and one or two contingent beneficiaries to ensure that their bases are covered.

Yes, you can have multiple primary beneficiaries.Contingent beneficiaries are the people you name as backups should your primary beneficiaries die before or at the same time as you. These backup beneficiaries only receive the money if the primary beneficiaries are unable to.

Your primary beneficiary must survive you or be an existing trust at your death. A contingent beneficiary will inherit your assets only if you have no surviving primary beneficiaries at the time of your death.