Personal Guaranty - General

What is this form?

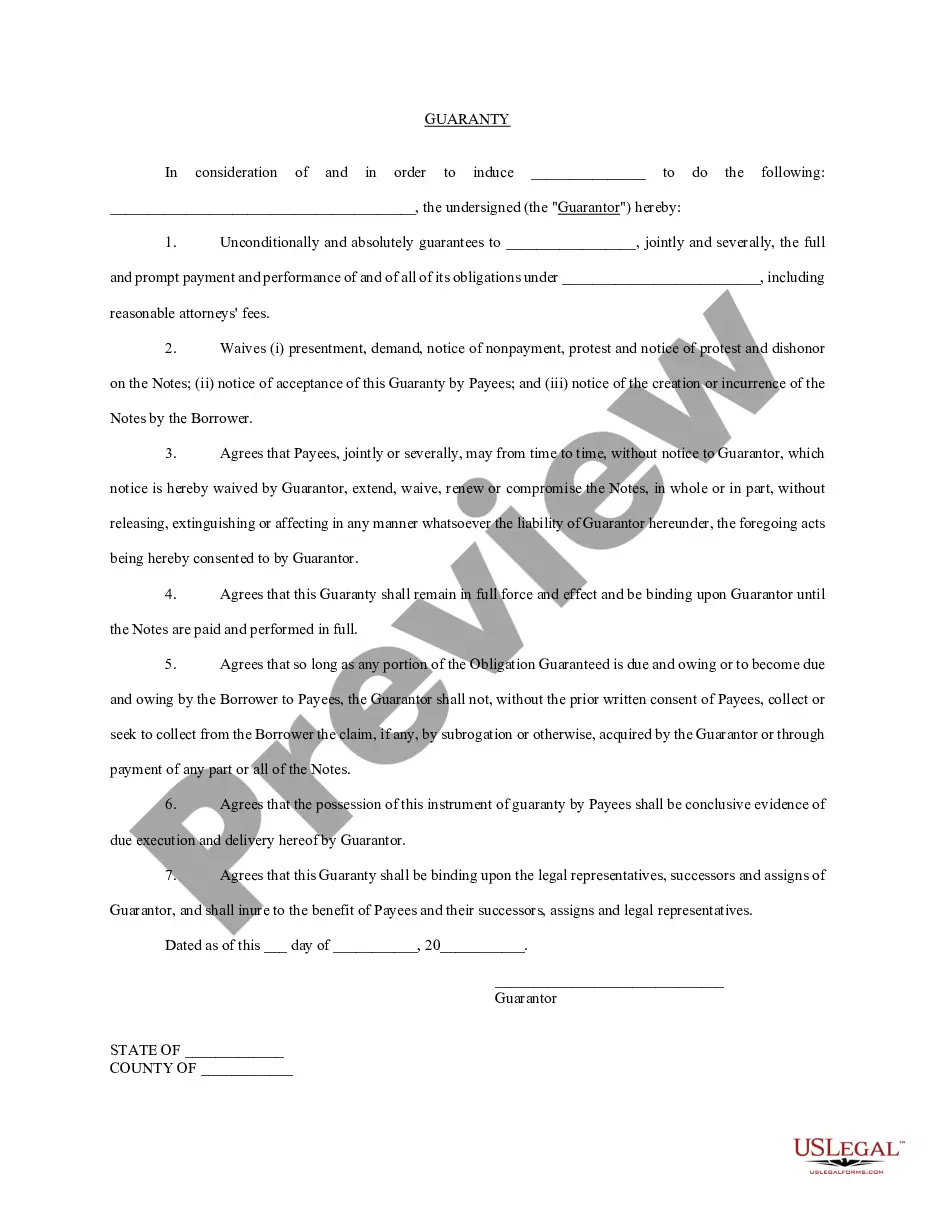

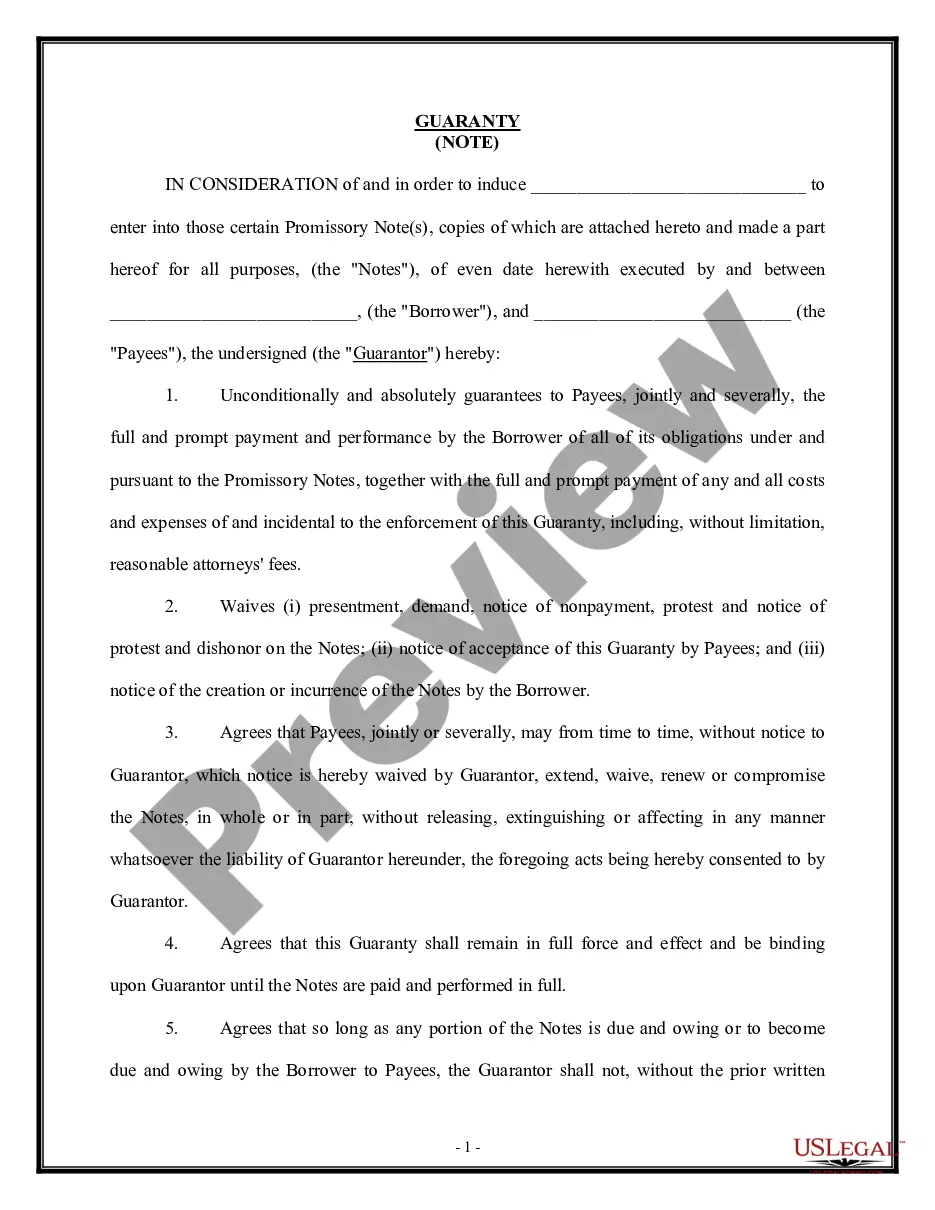

The Personal Guaranty - General is a legal document in which a guarantor agrees to ensure the full and prompt payment of all obligations incurred by a payor. This form provides a strong assurance to payees that they will receive what is owed, regardless of the payor's circumstances. It is distinct from similar forms as it emphasizes unconditional responsibility and the waiver of various notices and demands that would typically be expected in other agreements.

Key components of this form

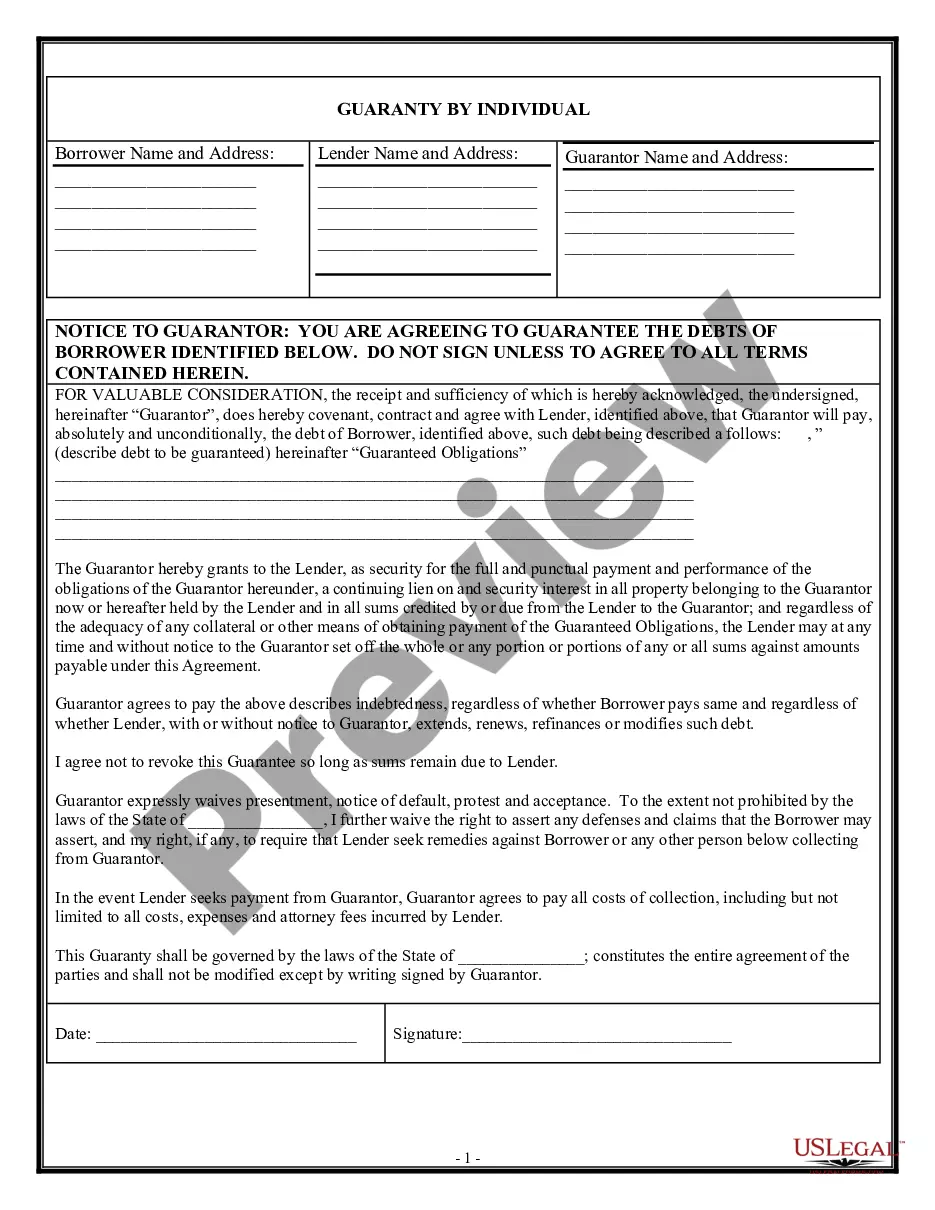

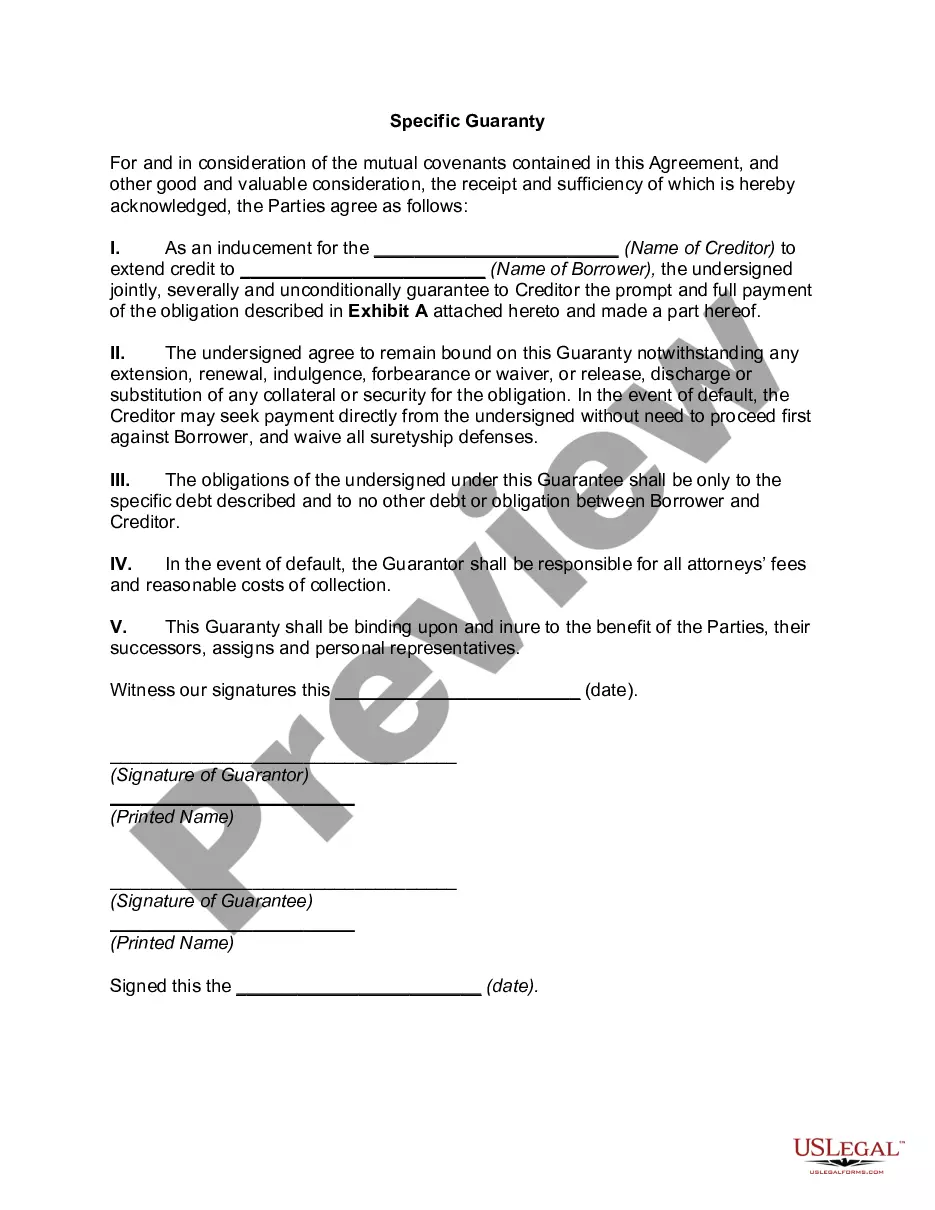

- Identification of the payees and the guarantor involved in the agreement.

- Unconditional guarantee of payment and performance of obligations.

- Waiver of presentment, demand, and notice of nonpayment rights.

- Agreement on the binding nature of the guaranty until all obligations are fulfilled.

- Conditions regarding subrogation rights after payment by the guarantor.

- Acknowledgment of the form's execution and reliability upon possession by payees.

When to use this document

This form is typically used in situations where an individual or entity is required to guarantee a loan or service agreement made by someone else. It is especially useful when a payee wants additional security for the payment of funds or fulfillment of obligations under a contract. Businesses often request a personal guaranty to reduce their risk when extending credit to new customers or when dealing with individuals with limited credit history.

Who needs this form

- Individuals who wish to act as guarantors for loans or contractual obligations.

- Business owners seeking additional assurances for credit extended to customers.

- Payees looking for a legally binding document to secure obligations from borrowers.

- Anyone involved in lending situations that require additional security for repayment.

How to prepare this document

- Identify and fill in the names of the payees and the guarantor in the designated fields.

- Clearly state the obligations that are being guaranteed and include relevant details.

- Provide the date of execution to indicate when the agreement takes effect.

- Ensure that all parties sign and date the form to validate the agreement.

- If necessary, have the signature of the guarantor notarized to ensure legal enforceability.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having the guarantor's signature notarized can enhance the document's legal strength and validity. Utilizing US Legal Formsâ integrated online notarization service is a convenient option for users who wish to ensure their agreement is legally binding.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include all required parties in the agreement.

- Not clearly specifying the obligations being guaranteed.

- Neglecting to have the document notarized when required by law.

- Overlooking the need for a date on the form.

- Assuming that a verbal agreement is sufficient without a written guaranty.

Why use this form online

- Convenient access to legal forms at any time without the need for physical visits.

- Easy editing and customization to fit specific agreements and obligations.

- Reliability in terms of legal enforceability when properly completed.

- Secure storage and download options for future reference.

Legal use & context

- This guaranty is legally enforceable as long as it is properly executed and notarized.

- Limitations may apply based on specific state laws and the terms agreed upon in the document.

Looking for another form?

Form popularity

FAQ

A personal guaranty is not enforceable without consideration In fact, no contract is enforceable without consideration. A personal guaranty is a type of contract. A contract is an enforceable promise. The enforceability of a contract comes from one party's giving of consideration to the other party.

Unless a business is a sole proprietorship, personal guarantees can only be discharged by filing an individual bankruptcy. A business bankruptcy will not eliminate a personal guarantee. Likewise, the Chapter 13 co-debtor stay only applies to consumer debts and personal guarantees are usually considered business debts.

A guaranty, much like any other contract, can be revoked later if both the guarantor and the lender agree in writing. Some debts owed by personal guarantors can also be discharged in bankruptcy. Many factors can affect the enforceability of personal guarantees.

Guarantor's death: The legal heirs/representatives are liable to assume the promise executed by the deceased under the guarantee, but they are not liable for future liabilities of the principal debtor after his death unless such liability on legal heirs is expressly mentioned in the guarantee contract.

A personal guarantee is a promise made by a person or an organization (the guarantor) to accept responsibility for some other party's debt (the debtor) if the debtor fails to pay it.A guarantor can be any party, including an individual or another organization, with a credit history.

It's relatively common for a business owner to file individual bankruptcy to get rid of a personal guaranteeand most personal guarantees will qualify for discharge.Also, keep in mind that filing on behalf of the business won't get rid of your personal obligation to pay back the guaranteed loan.

The simple answer is Yes. If the consideration of the guarantee is divisible, the guarantee can be revoked once notice of the death of the Guarantor is received by the Creditor. If the consideration of the guarantee is entire, the Guarantor's estate will be liable for the total amount guaranteed.

Death of a Guarantor Most guaranties survive the death of the guarantor, and any liability will become part of the guarantor's estate.Typically, a lender will not release an estate from liability, unless the lender agrees to allow another party acceptable to the lender to take the deceased guarantor's place.

Business owners can exercise their right to revoke the guarantee. Finally, business owners need to be aware that the personal guarantee may include a right to revoke. Typically, a right to revoke the guarantee does not limit the amount of the guarantor's liability as of the date of the revocation.