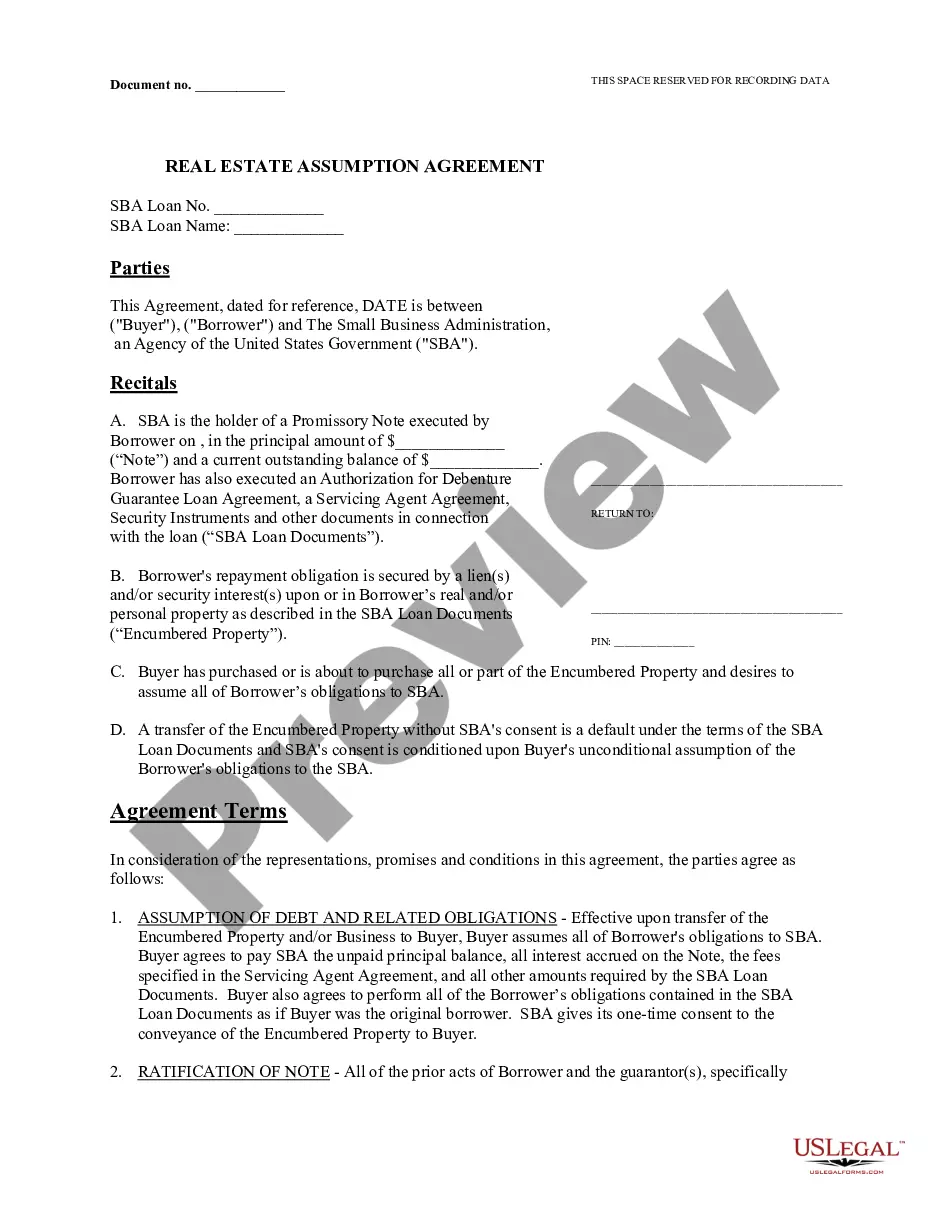

Assumption Agreement of SBA Loan

What is this form?

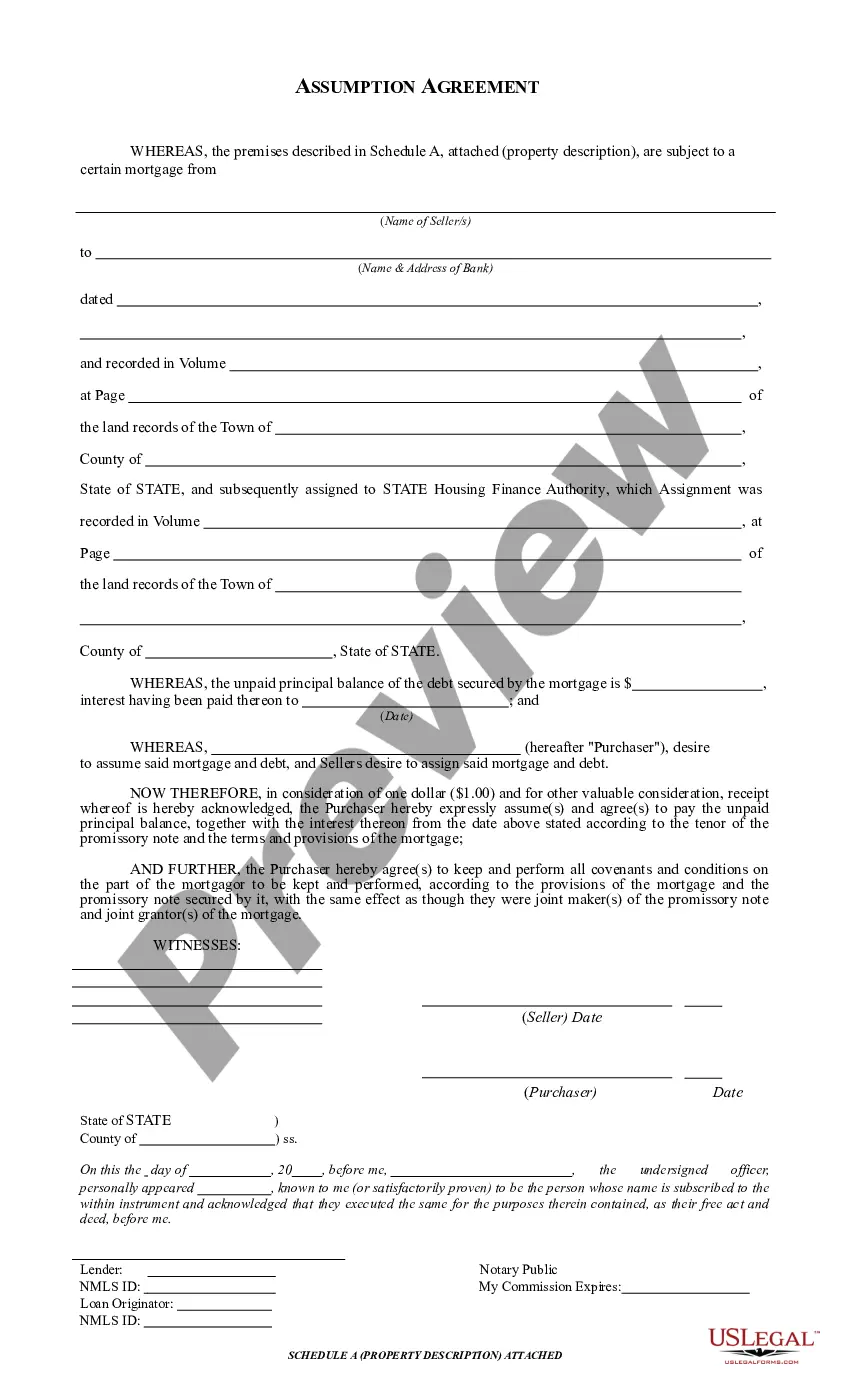

The Assumption Agreement of SBA Loan is a legal document that allows one party, referred to as the Assumptor, to take over the loan obligations from the original borrower under a Small Business Administration (SBA) loan. This form is different from other loan documents as it formally outlines the transfer of liability and payment responsibilities, ensuring that all parties understand their obligations and rights. By using this form, the SBA acknowledges the Assumptor's commitment to continue making loan payments and releases the original borrower from their obligations.

What’s included in this form

- Identification of the Borrower, Assumptor, and SBA.

- Details about the original loan amount and terms.

- Conditions for assumption of loan obligations.

- Consent required from the SBA to transfer the debt.

- Notary section for verification of the agreement.

Common use cases

This form should be used when a borrower wishes to transfer their SBA loan obligations to another party. Typical scenarios include sales of a business where the buyer agrees to take over existing loans, or situations where the original borrower can no longer manage their loan payments. Utilizing this agreement ensures that all parties involved understand the terms and legal obligations of the loan, as well as the approval from the SBA.

Who should use this form

- Business owners looking to transfer their SBA loan to another party.

- Individuals or businesses interested in assuming an existing SBA loan.

- Legal professionals assisting clients with the loan assumption process.

How to complete this form

- Identify and enter the names of the Borrower and Assumptor.

- Specify the original principal loan amount and loan details.

- Include the necessary dates related to the original loan documents.

- Obtain consent signatures from both the Assumptor and Borrower.

- Have the form notarized as required to confirm the agreement.

Notarization guidance

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to provide accurate loan details, such as the principal amount and dates.

- Not obtaining the necessary consent from the SBA before assuming the loan.

- Missing signatures from all parties involved in the agreement.

- Not notarizing the document when required.

Why use this form online

- Easy access to legally drafted and verified forms.

- Convenience of completing and downloading the form immediately.

- Flexible usage, allowing modification to fit specific circumstances.

- Reduced risk of errors due to clear, guided instructions.

Looking for another form?

Form popularity

FAQ

Are SBA 504 loans assumable? Yes, as long as the SBA/SPEDCO have an opportunity to review both corporate and personal financial information on the proposed borrower(s) in advance of the sale. One note of caution: the release of the original borrower's personal guaranty is NOT automatic with a loan assumption.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

The SBA isn't willing to negotiate for the sake of negotiating. An OIC will only be considered if you can demonstrate your ability to repay the debt over a reasonable period.

SBA 504 loans can only be assumed once, and the new loan must include a due on sale or death clause to prohibit any future assumptions. All parties involved must sign a written agreement that specifies the terms of the assumption.

EIDL termsLoan collateral can include tangible and intangible property like inventory and equipment. Borrowers can't sell, lease, license or transfer collateral without prior approval from the SBA.

Fortunately for borrowers, SBA loans, including the SBA 7(a) loan, are fully assumable with SBA approval.In particular, the SBA will look to ensure that the new borrower is eligible under SBA guidelines, and has enough financial strength and business experience to make a potential loan default unlikely.

The streamlined SBA loan forgiveness application is available to business owners who borrowed $50,000 or less in PPP funds. The streamlined process is not available for business owners who, together with their affiliates, received $2 million or more under the program.

Guarantee Portion - Under the 7(a) guaranteed loan program SBA typically guarantees from 50% to 85% of an eligible bank loan up to a maximum guaranty amount of $3,750,000.

In order to qualify for an SBA disaster loan, the Small Business Administration will perform a routine credit check to ensure you qualify against the SBA's credit score requirements.According to Fundera, SBA loan minimum credit requirements fall around 620-640.