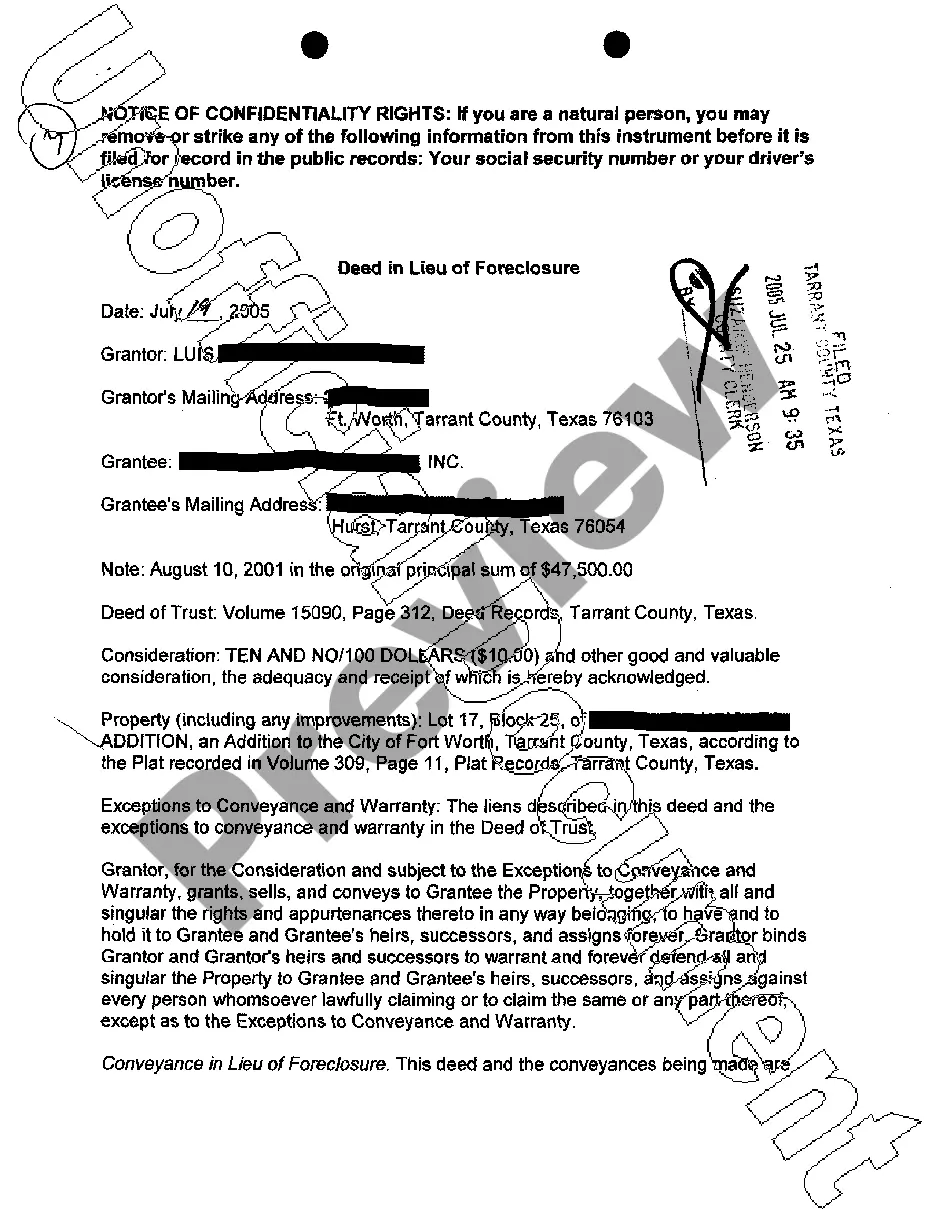

Texas Deed in Lieu of Foreclosure

What this document covers

A Deed in Lieu of Foreclosure is a legal document in which a property owner voluntarily transfers ownership of their property to the lender to avoid foreclosure proceedings. This form serves as an alternative to foreclosure and can help protect the homeowner's credit. It is important to note that while it achieves a similar outcome, it differs from standard foreclosure processes by potentially allowing for a smoother resolution between the borrower and lender.

Key parts of this document

- Grantor and Grantee information: Identifies the property owner (Grantor) and the lender (Grantee).

- Property description: Details the property being transferred.

- Acknowledgment of lien: Confirms that the Grantee has a lien on the property.

- Transfer of ownership: Specifies the transfer of ownership rights from the Grantor to the Grantee.

- Removal of personal property: Declares that all personal property not subject to the lien has been removed.

Common use cases

This form is typically used when a homeowner is facing financial difficulties and can no longer maintain mortgage payments. If foreclosure seems imminent, the homeowner can offer a Deed in Lieu of Foreclosure to the lender. This can also be beneficial when the property value has declined, making it difficult for the homeowner to sell. Utilizing this form can provide a more amicable way to resolve the mortgage imbalance while mitigating the impact on credit history.

Who this form is for

- Homeowners struggling to make mortgage payments.

- Individuals facing impending foreclosure on their property.

- Borrowers seeking to safeguard their credit rating by avoiding foreclosure.

- Property owners who have negotiated with their lender for a deed transfer.

Completing this form step by step

- Identify the parties: Clearly state the names of the Grantor (property owner) and Grantee (lender).

- Specify the property: Include a detailed description of the property being transferred.

- Include acknowledgment of lien: Ensure that the Grantor confirms the existence of the lender's lien on the property.

- Transfer ownership: Clearly outline the terms under which ownership will be transferred.

- Sign and date the document: Both parties should provide their signatures and the date of signing.

Notarization requirements for this form

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include a complete property description, which may cause legal issues.

- Not obtaining the necessary signatures from both parties.

- Neglecting to review local laws that might affect the validity of the document.

- Submitting the form without ensuring all personal property has been removed from the premises.

Why complete this form online

- Convenience: Easily download and customize the form from anywhere.

- Editability: Tailor the language to fit your specific circumstances.

- Reliability: Legal forms are prepared by licensed attorneys to ensure compliance with state law.

Main things to remember

- A Deed in Lieu of Foreclosure can help avoid foreclosure and protect your credit.

- Complete the form accurately to ensure validity and avoid legal issues.

- This form complies with Texas laws; always reference local regulations.

- Remove all personal property from the property before execution.

Looking for another form?

Form popularity

FAQ

The impact that a deed in lieu has on your score depends primarily on your credit history.According to FICO, if you start with a score of around 780, a deed in lieu (without a deficiency balance) shaves 105 to 125 points off your score; but if you start with a score of 680, you'll lose 50 to 70 points.

Rather than deal with the foreclosure process, I would like to give you the deed to my home, in exchange for forgiveness on the loan. I do not have a second mortgage, and there are no other liens on the property. I have attached all relevant documents for the house and for my current economic situation.

Disadvantages of a Deed in Lieu of Foreclosure. Perhaps the biggest disadvantage of a deed in lieu is that the Lender takes subject to all other encumbrances and interests in the Property. Therefore if there is a second mortgage, for example, a deed in lieu would likely not be a viable strategy.

If your lender agrees to a short sale or to accept a deed in lieu of foreclosure, you might owe federal income tax on any forgiven deficiency. The IRS learns of the deficiency when the lender sends it a Form 1099-C, which reports the forgiven debt as income to you.

The waiting period on a conventional loan after a deed in lieu is 4 years, compared to 7 years on a conventional loan.

Final Thoughts On Deed In Lieu Of Foreclosure When you take a deed in lieu agreement, you transfer your home's deed to your lender voluntarily. In exchange, the lender agrees to forgive the amount left on your loan. A deed in lieu agreement won't stay on your credit report if a foreclosure will.

The deed in lieu of foreclosure offers several advantages to both the borrower and the lender. The principal advantage to the borrower is that it immediately releases him/her from most or all of the personal indebtedness associated with the defaulted loan.