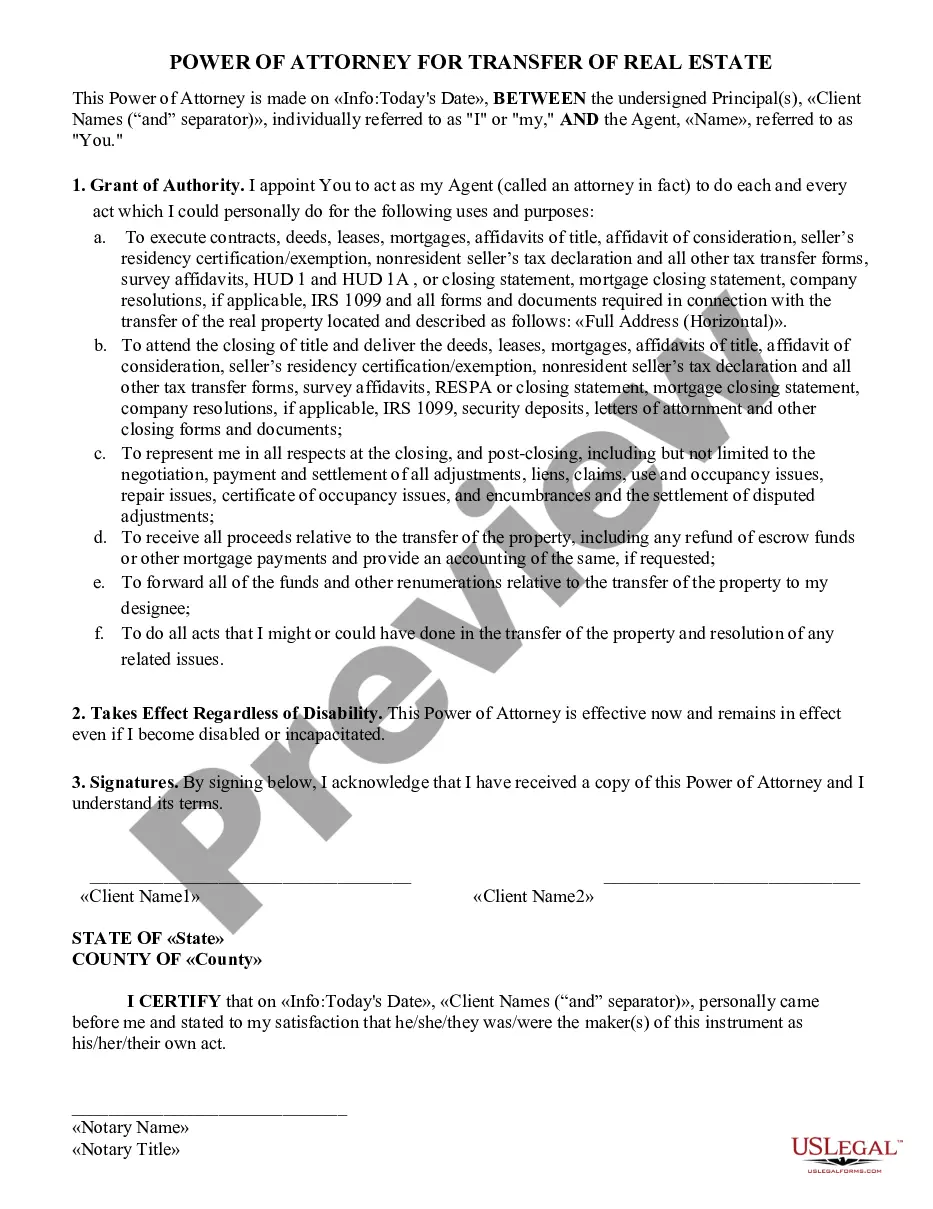

South Dakota Special or Limited Power of Attorney for Real Estate Purchase Transaction by Purchaser

About this form

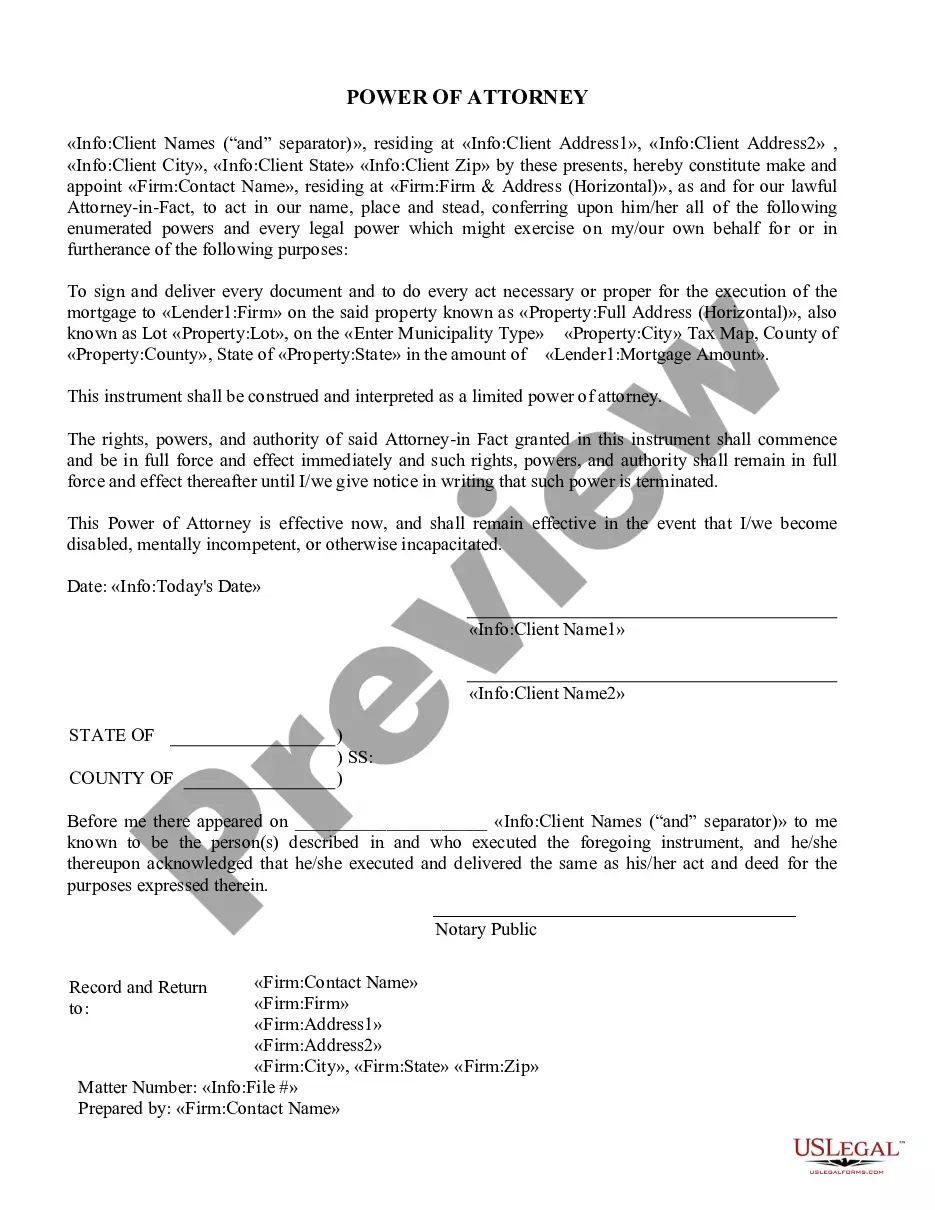

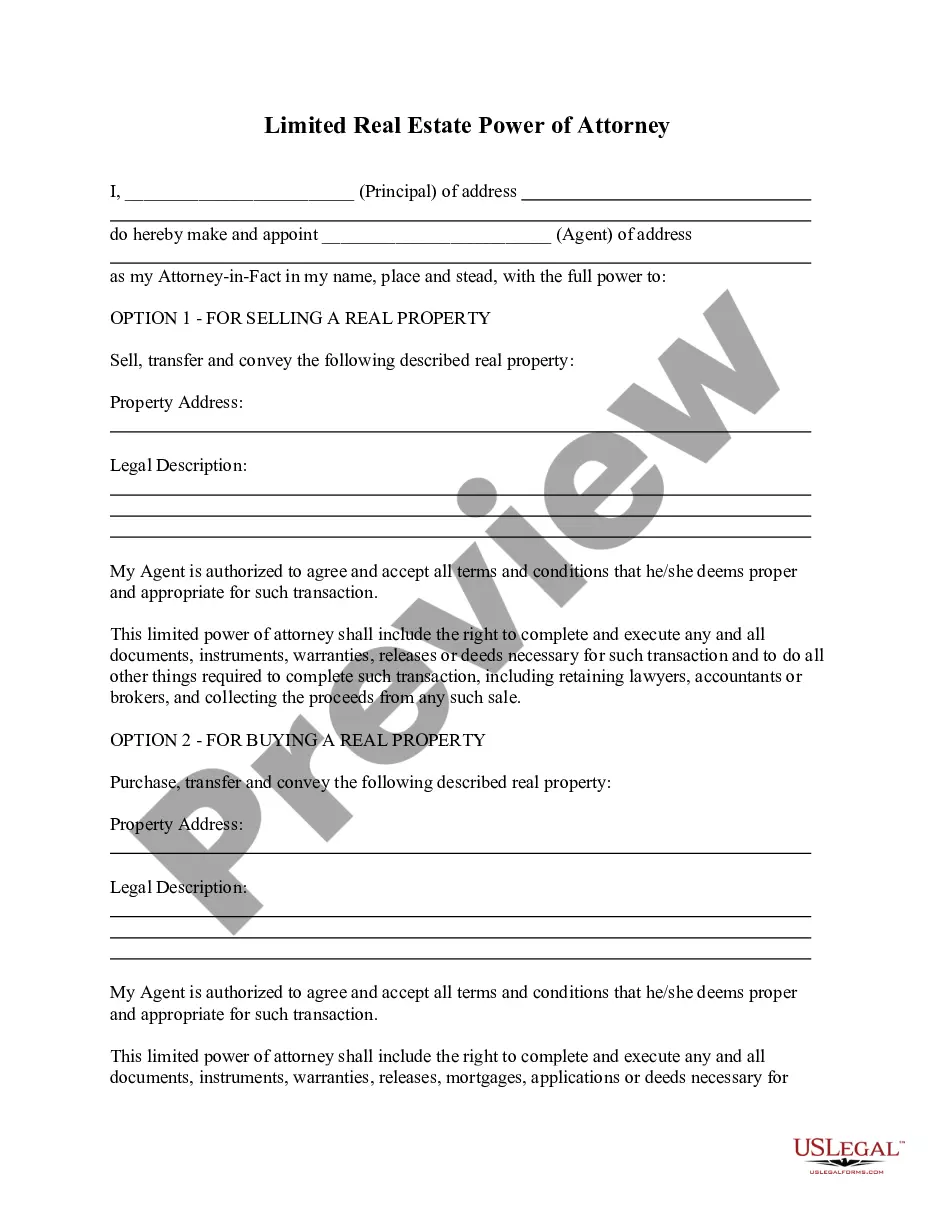

The Special or Limited Power of Attorney for Real Estate Purchase Transaction is a legal document that allows a purchaser to appoint an attorney-in-fact to act on their behalf in completing a real estate transaction. This form is specifically tailored for facilitating property purchases, enabling the attorney-in-fact to execute necessary documents such as loan agreements and closing statements. Unlike a general power of attorney, this form restricts authority to real estate transactions only, making it ideal for ensuring focused legal action in property dealings.

Form components explained

- Identification of the purchaser and attorney-in-fact, including their addresses.

- Declaration of authority granted to the attorney-in-fact for completing the purchase.

- Details regarding the real property being purchased, including its legal description.

- Signature lines for the purchaser and notary public.

- Notary acknowledgment section to verify the authenticity of the document.

When this form is needed

This form should be used when a purchaser is unable to complete a real estate transaction themselves and wishes to appoint another individual to handle the transaction on their behalf. Common situations include when the purchaser is unavailable due to travel, health issues, or when they prefer to delegate the closing process to an experienced agent or attorney.

Intended users of this form

This form is suitable for:

- Individuals purchasing real estate who want to delegate authority.

- Real estate investors managing multiple properties requiring streamlined processes.

- Anyone needing to complete a transaction without being physically present.

How to prepare this document

- Identify the parties involved, including the purchaser and the appointed attorney-in-fact.

- Specify the real estate property being purchased, including its full address and legal description.

- Enter the date of execution and sign the document in the designated area.

- Complete the notary acknowledgment section, ensuring the notary verifies your identity and signature.

- Make copies of the completed and notarized document for your records and for the attorney-in-fact.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include the complete legal description of the property.

- Not signing the form in the presence of a notary public.

- Leaving blank fields which can lead to legal complications.

- Choosing an attorney-in-fact who is unable to effectively carry out the purchaser's intentions.

Why complete this form online

- Convenient access to professionally drafted legal forms at any time.

- Easy to download and customize according to specific transaction needs.

- Reliable templates designed by licensed attorneys to ensure legal compliance.

Main things to remember

- The form is used to appoint an attorney-in-fact for real estate transactions.

- Notarization is required to validate the form.

- Common mistakes include incomplete information and lack of notarization.

- This document streamlines the property purchase process when the purchaser cannot be present.

Looking for another form?

Form popularity

FAQ

An estate consists of cash, cars, real estate and anything else owned by the deceased that has value.A deceased person's heirs receive any amount left over after all debts are settled, as dictated by the terms of a valid will.

The primary purpose of an estate plan is to help you examine your financial needs and assets in order to make sure that your heirs are provided for in the best possible way, including lifetime planning as well as disposition of property at death.

Estate administration is the process that occurs after a person dies. During this process, the decedent's probate assets are collected, creditors are paid, and then the remaining assets are distributed to the decedent's beneficiaries in accordance with the decedent's will.

An estate is the economic valuation of all the investments, assets, and interests of an individual. The estate includes a person's belongings, physical and intangible assets, land and real estate, investments, collectibles, and furnishings.Estate taxes may be levied on the value of one's estate at death.

Unfortunately, every estate is different, and that means timelines can vary. A simple estate with just a few, easy-to-find assets may be all wrapped up in six to eight months. A more complicated affair may take three years or more to fully settle.

An estate, in common law, is the net worth of a person at any point in time alive or dead. It is the sum of a person's assets legal rights, interests and entitlements to property of any kind less all liabilities at that time.The term is also used to refer to the sum of a person's assets only.

An estate consists of cash, cars, real estate and anything else owned by the deceased that has value.A deceased person's heirs receive any amount left over after all debts are settled, as dictated by the terms of a valid will.

Noun. a piece of landed property, especially one of large extent with an elaborate house on it: to have an estate in the country. Law. property or possessions. the legal position or status of an owner, considered with respect to property owned in land or other things.

Estate: The assets you own at your death that could be used to pay your debts, including all personal property, real property, and other liquid assets.