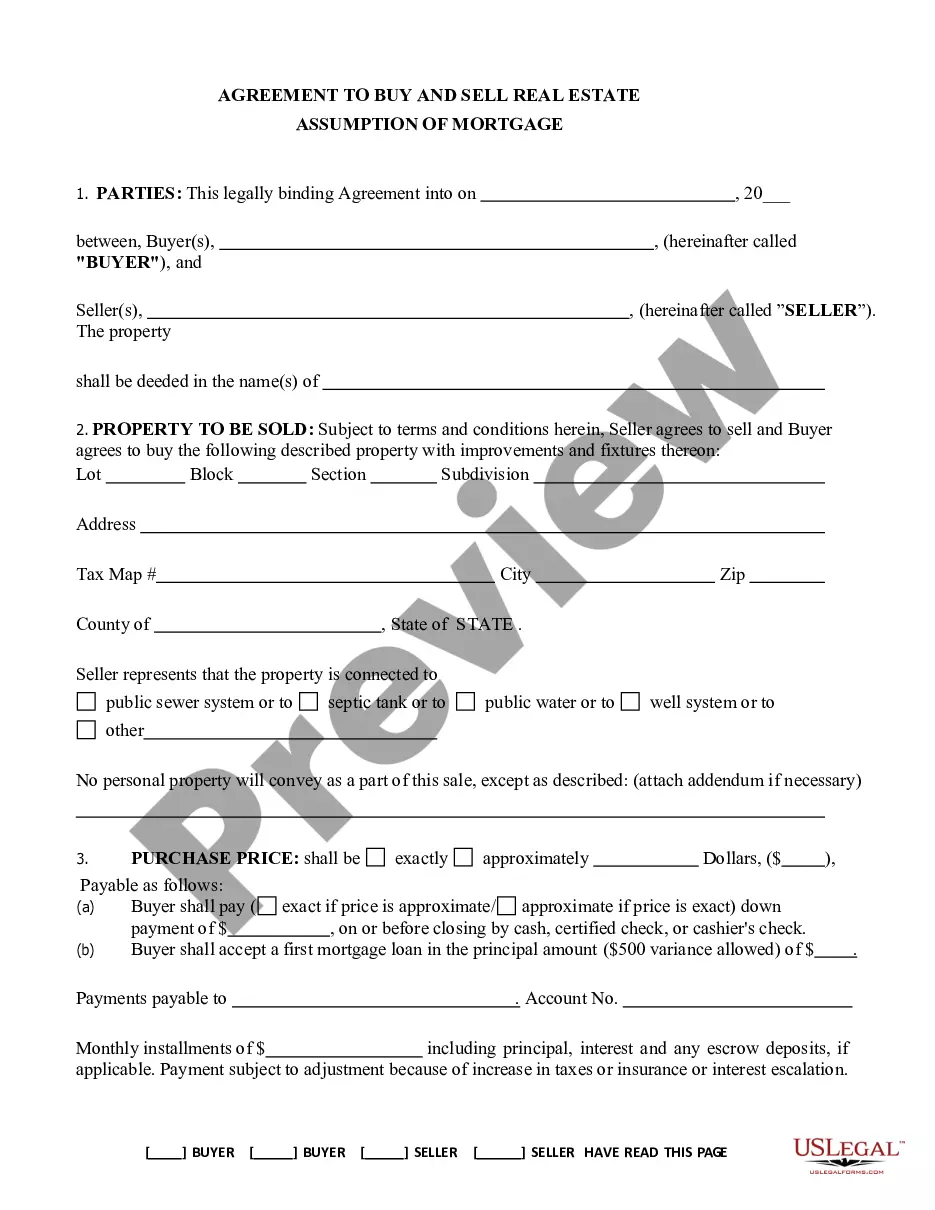

Kentucky Assumption Agreement of Mortgage and Release of Original Mortgagors

Overview of this form

The Assumption Agreement of Mortgage and Release of Original Mortgagors is a legal document used when new purchasers assume responsibility for an existing mortgage. This form facilitates the transfer of debt from the original mortgagors to the new buyers, ensuring that the lender releases the original owners from any future liability on the mortgage. It is an important tool for both lenders and purchasers, distinguishing itself from other mortgage-related documents by focusing specifically on the assumption of an existing mortgage debt.

Key parts of this document

- Identification of the original mortgagors and new purchasers.

- Details on the mortgage debt being assumed, including amounts and interest rates.

- Agreement to make monthly payments and perform obligations under the existing mortgage.

- Release clause for original mortgagors from future liability.

- Space for signatures and notary acknowledgment.

When this form is needed

This form is used when a property is sold, and the new buyers intend to take over the existing mortgage obligations. It is applicable in situations where the lender permits the assumption of the mortgage, allowing the new buyers to step into the financial responsibility of the loan without requiring the original owners to remain liable.

Who needs this form

- New purchasers of a property who wish to assume an existing mortgage.

- Original mortgagors looking to transfer mortgage obligations and become relieved of future liabilities.

- Lenders who need a formal agreement to document the assumption of the mortgage debt.

Steps to complete this form

- Identify the parties involved: the original mortgagors and new purchasers.

- Enter the details of the mortgage, including the total debt amount and interest rate.

- Specify the start date for the new monthly payments.

- Complete all necessary fields for signatures from all parties involved.

- Have the document notarized, if required, to ensure its validity.

Does this document require notarization?

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to correctly enter the mortgage details, such as the total debt amount.

- Not having the signature of all required parties.

- Neglecting to have the document notarized, if required.

- Leaving sections incomplete which may lead to confusion or legal issues in the future.

Advantages of online completion

- Convenience of completing the form from home without the need for in-person visits.

- Editability allows you to ensure accuracy and make changes easily before finalizing.

- Access to professionally drafted templates that provide legal reliability.

Looking for another form?

Form popularity

FAQ

Having an assumable loan might give a seller a marketing edge, particularly if mortgage rates have risen since the seller got the loan. For a buyer, assuming a mortgage can save thousands of dollars in interest payments and closing costs but it could require making a big down payment.

What is a mortgage assumption agreement? It's actually pretty self-explanatory. A person who assumes a mortgage takes over a payment from the previous homeowner. Basically, the agreement shifts the financial responsibility of the loan to a different borrower.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

In most circumstances, a mortgage can't be transferred from one borrower to another. That's because most lenders and loan types don't allow another borrower to take over payment of an existing mortgage.

You will get the options like transferring an assumable mortgage by requesting your lender to make the change, refinancing the loan in the new owner's name, transferring when the situation demands a loan's due on sale clause, etc. If a loan is assumable that means you can transfer the mortgage to anyone else.

Conventional loans cannot be assumed because the loan must be backed (FHA loan) or insured (VA loan) by a government entity. If your parents' mortgage falls under either of these categories, you're in the clear. However, you'll need to see if the bank believes you're eligible to receive the loan.

Advantages. If the assumable interest rate is lower than current market rates, the buyer saves money straight away. There are also fewer closing costs associated with assuming a mortgage. This can save money for the seller as well as the buyer.

You can transfer a mortgage to another person if the terms of your mortgage say that it is assumable. If you have an assumable mortgage, the new borrower can pay a flat fee to take over the existing mortgage and become responsible for payment. But they'll still typically need to qualify for the loan with your lender.

If you simply want to transfer your own mortgage to another person, it is possible, but there are a few strings attached. This is known as gifting a property.Typically, you're removing yourself from the mortgage by repaying the loan in full. The new homeowner will then take out a new mortgage on the property.