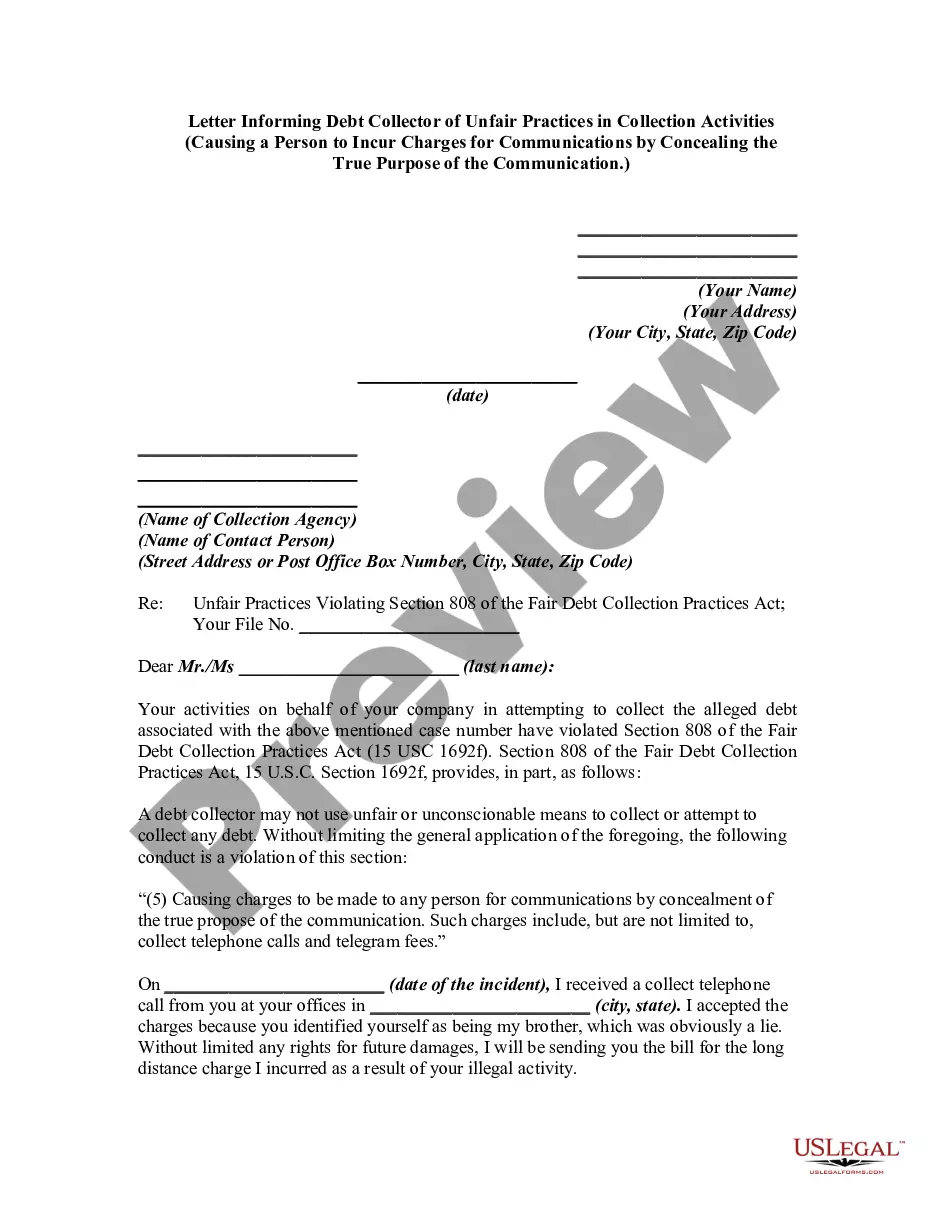

A debt collector may not use unfair or unconscionable means to collect a debt. This includes causing a person to incur charges for communications by concealing the true propose of the communication.

Washington Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Category:

State:

Multi-State

Control #:

US-DCPA-44

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Causing A Consumer To Incur Charges For Communications By Concealing The Purpose Of The Communication?

Selecting the correct sanctioned document format can be challenging. Obviously, there is a multitude of templates accessible online, but how can you find the sanctioned form you require? Utilize the US Legal Forms website. The service offers thousands of templates, such as the Washington Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication, which can serve both business and personal needs. All forms are reviewed by experts and comply with state and federal requirements.

If you are presently registered, Log In to your account and click on the Download button to obtain the Washington Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication. Use your account to search through the legal forms you have previously acquired. Navigate to the My documents section of your account and retrieve another copy of the document you need.

If you are a new user of US Legal Forms, here are simple steps that you should adhere to: First, ensure you have selected the correct form for your city/state. You can review the form using the Review button and read the form description to confirm it suits your needs. If the form does not meet your requirements, use the Search field to find the appropriate form. Once you are confident that the form is suitable, click the Purchase now button to acquire the form. Choose the pricing plan you prefer and enter the required information. Create your account and pay for the order using your PayPal account or credit card. Select the file format and download the legal document template to your device. Complete, modify, print, and sign the obtained Washington Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication.

US Legal Forms is the largest repository of legal templates where you can find numerous document formats. Utilize the service to obtain professionally crafted documents that adhere to legal standards.

- Consider your state and federal regulations when choosing a legal form.

- Explore a variety of templates available on the US Legal Forms platform.

- Easily Log In to access previously downloaded legal documents.

- Follow simple guidelines to select and purchase the correct form.

- Utilize online payment options for convenience.

- Ensure the document is completed, modified, printed, and signed appropriately.

Form popularity

FAQ

When a collection agency communicates with anyone other than the consumer, it can be permissible under certain conditions. The Fair Debt Collection Practices Act (FDCPA) allows such interactions as long as the communication does not reveal sensitive information or intentions. However, it is crucial for debt collectors to adhere to guidelines, such as those specified in the Washington Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication.

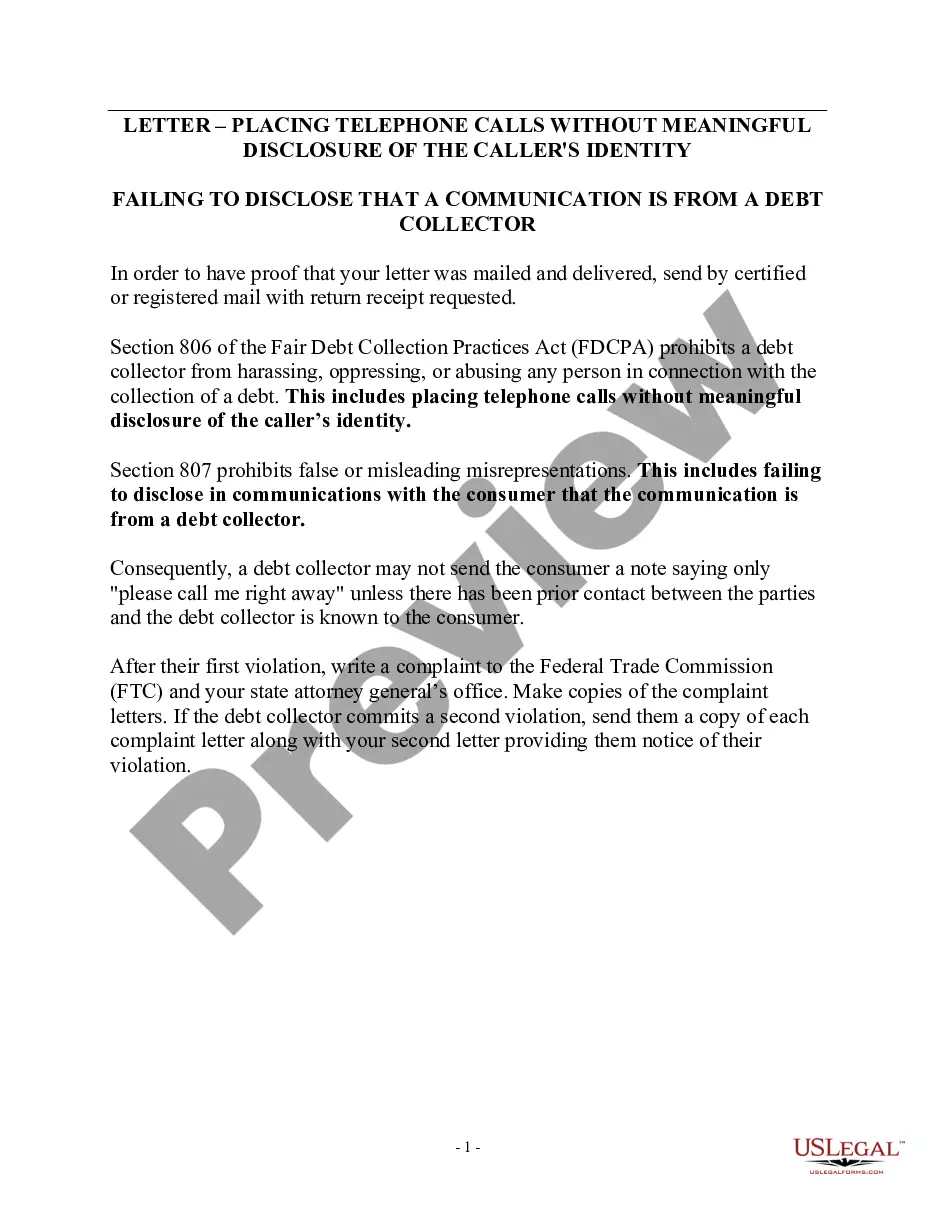

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Debt Collectors Can't Call You Repeatedly to Harass You This means that while the FDCPA doesn't place a specific limit on the number of calls debt collectors can make, it prohibits them from calling you multiple times just to harass you. (15 U.S. Code §? 1692d).

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

A debt validation letter should include the name of your creditor, how much you supposedly owe, and information on how to dispute the debt. After receiving a debt validation letter, you have 30 days to dispute the debt and request written evidence of it from the debt collector.

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

If, within the 30-day period, the consumer disputes in writing any portion of the debt or requests the name and address of the original creditor, the collector must stop all collection efforts until he or she mails the consumer a copy of a judgment or verification of the debt, or the name and address of the original

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.