Virginia Non-Foreign Affidavit Under IRC 1445

What this document covers

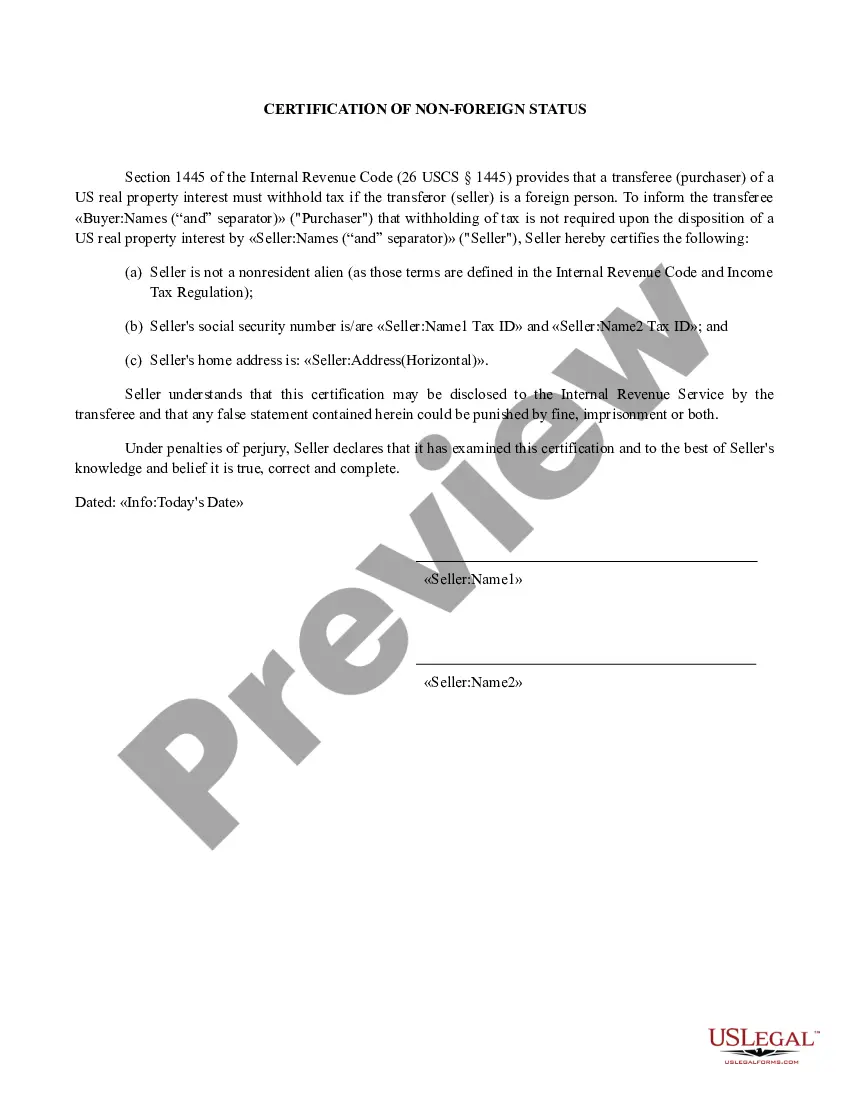

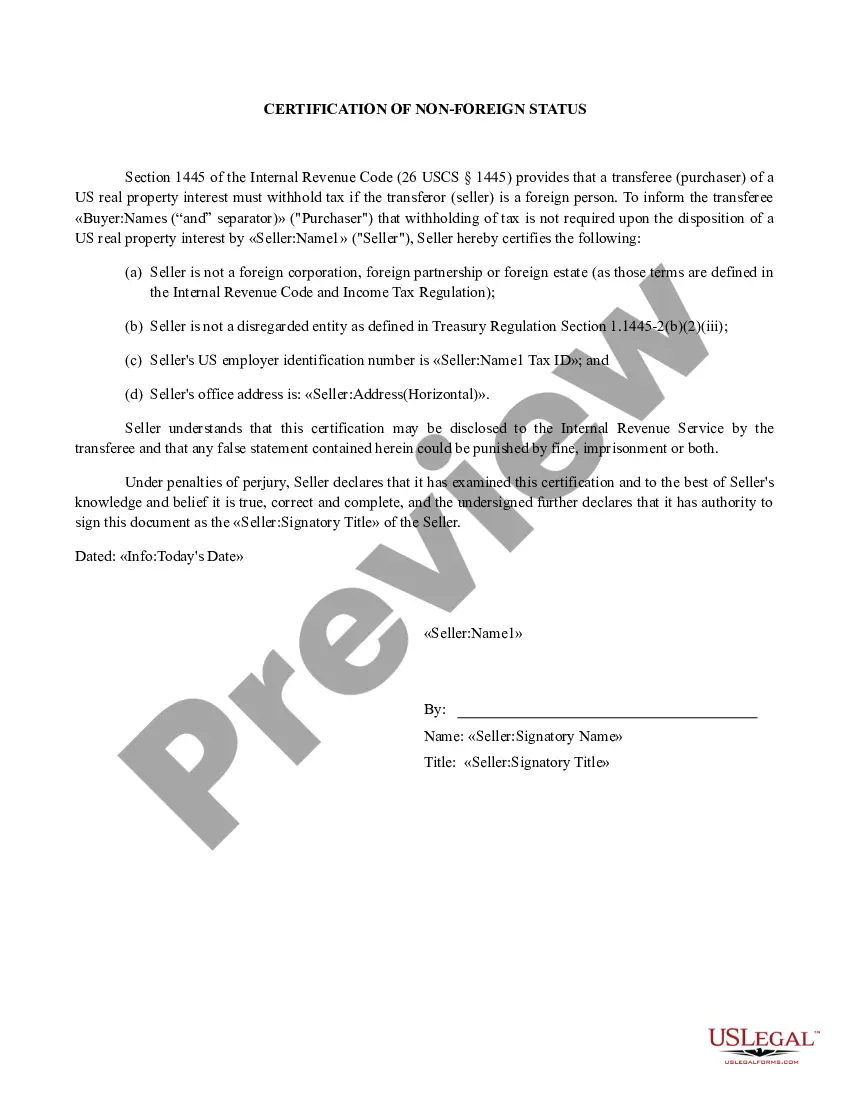

The Non-Foreign Affidavit Under IRC 1445 is a legal document for sellers of real property to confirm they are not considered foreign persons under the Internal Revenue Code. This affidavit is essential to avoid tax withholding that typically applies to foreign sellers when property is transferred. Unlike other affidavits, this form specifically caters to real estate transactions and provides a straightforward declaration regarding the seller's tax status.

Key components of this form

- Identification of the seller(s) and property being sold.

- Declaration that the seller(s) is/are not a foreign person under IRC Section 1445.

- Affidavit's purpose to establish non-foreign seller status for tax withholding exemptions.

- Seller(s) signatory information and date of signing.

- Notary section for official witnessing of the seller's signatures.

When to use this form

This form should be used during the sale of real property when the seller needs to certify their non-foreign status under the Internal Revenue Code. It is required when the buyer or transferee must obtain proof that the seller is exempt from the 15 percent withholding tax mandated for foreign entities. This affidavit is typically utilized in residential and commercial real estate transactions in the United States.

Intended users of this form

This form is intended for:

- Individuals or entities selling real estate in the U.S.

- Property sellers who are United States citizens or residents.

- Those completing a real estate transaction that requires proof of non-foreign seller status.

How to complete this form

- Begin by identifying all sellers and their contact information, including taxpayer identification numbers.

- Clearly specify the property being sold, including its address and legal description.

- Provide a declaration stating that the seller(s) is/are not a foreign person according to IRS definitions.

- Ensure all sellers sign and date the affidavit.

- Complete the notary section to officially witness the signing of the affidavit.

Does this form need to be notarized?

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all sellers' information if there are multiple parties involved.

- Omitting the proper legal description of the property being sold.

- Not including or inaccurately providing taxpayer identification numbers.

- Forgetting to sign and date the form after completion.

- Neglecting the notary certification, which is essential for legal validity.

Advantages of online completion

- Convenience: Access and complete the form from anywhere at any time.

- Editability: Easily make necessary changes before finalizing the document.

- Reliability: Use a template crafted by licensed attorneys to ensure compliance with legal requirements.

- Instant download: Obtain your affidavit right after completion, avoiding delays.

Legal use & context

- This affidavit serves as a protective measure against unwarranted tax withholding on real estate sales.

- The accuracy of the information provided is crucial, as false declarations could lead to penalties.

- Local laws may have additional requirements or variations in related forms.

Quick recap

- The Non-Foreign Affidavit under IRC 1445 is vital for sellers to confirm non-foreign status.

- Notarization is required for the affidavit to be valid.

- This form is applicable in multiple jurisdictions and must comply with local real estate laws.

Looking for another form?

Form popularity

FAQ

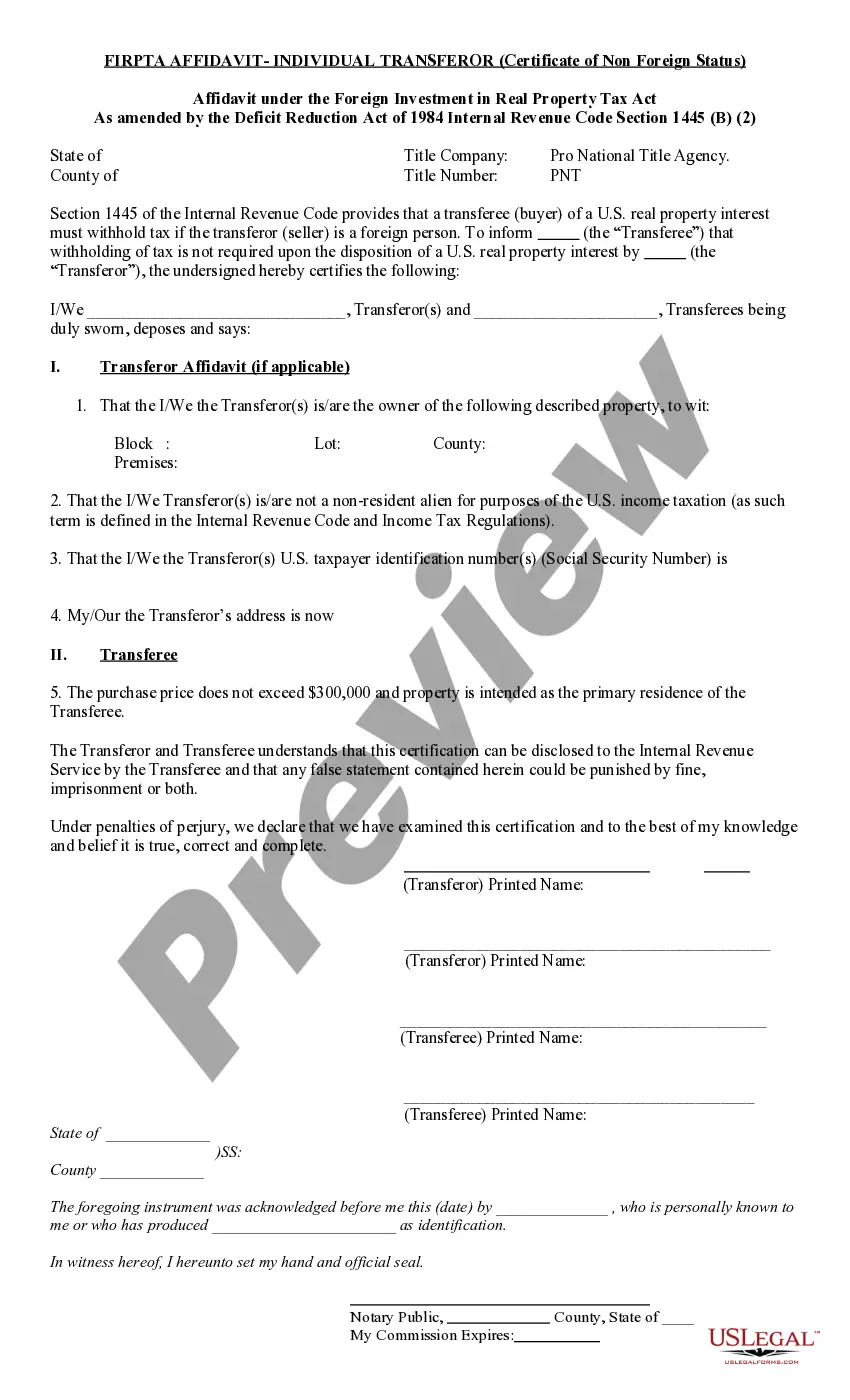

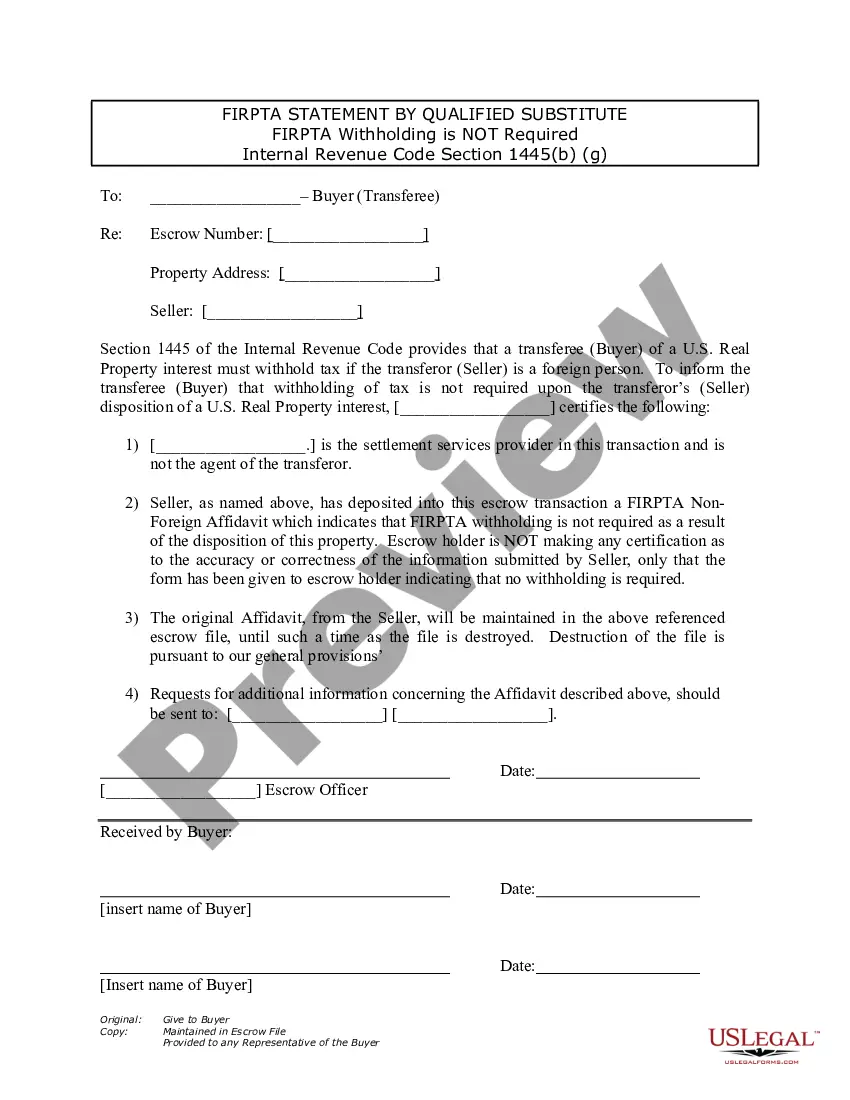

This document, included in the seller's opening package, requests that the seller swears under penalty of perjury that they are not a non-resident alien for purposes of United States income taxation. A Seller unable to complete this affidavit may be subject to withholding up to 15%.

In most cases, the purchaser of a U.S. real property interest must deduct and withhold ten percent of the amount realized by the foreign seller. However, the amount withheld should not exceed the seller's maximum tax liability.

What Is a Certification of Non-Foreign Status? With a Certification of Non-Foreign Status, the seller of real estate is certifying under penalty of perjury, that the seller is not foreign. Therefore, the seller and the transaction will not have the withholding requirements.

The only other way to avoid FIRPTA is via a withholding certificate. If FIRPTA withholding exceeds the maximum tax liability realized on the sale of the real property, sellers can appeal to the IRS for a lower withholding amount.

Persons purchasing U.S. real property interests (transferees) from foreign persons, certain purchasers' agents, and settlement officers are required to withhold 15% (10% for dispositions before February 17, 2016) of the amount realized on the disposition (special rules for foreign corporations).

FIRPTA Exemptions The sales price is $300,000 or less, and. The buyer signs affidavit at or before closing stating they intend to use property for personal purposes for at least 50% of time property occupied for the each of the first two 12 month periods immediately after closing.

The Foreign Investment in Real Property Transfer Act (FIRPTA) requires any buyer of a U.S. real property interest to withhold ten percent of the amount realized by a foreign seller. 26 USC § 1445(a).

You or a member of your family must have definite plans to reside at the property for at least 50% of the number of days the property is used by any person during each of the first two 12-month periods following the date of transfer.