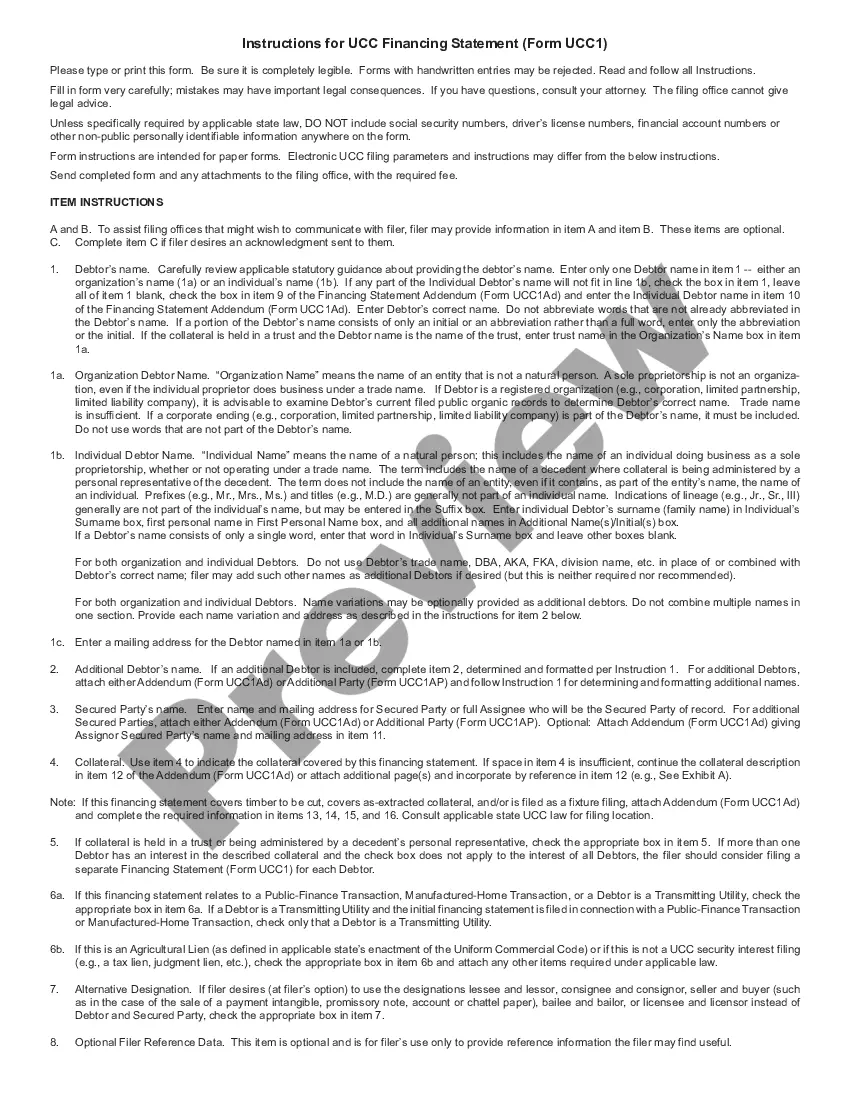

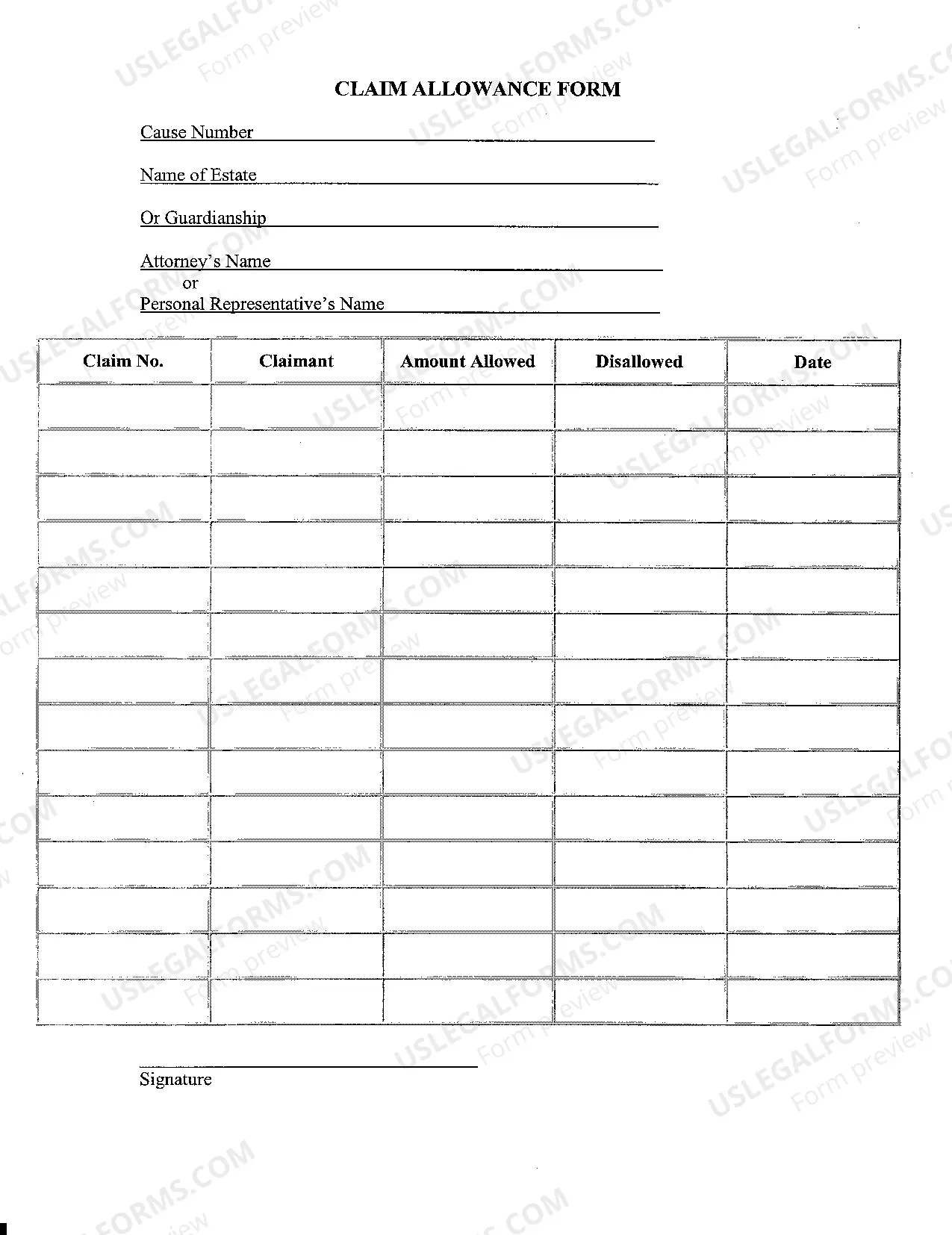

UCC Schedule

Understanding this form

The UCC Schedule is a document that serves as an attachment to the UCC-1 Financing Statement. Its purpose is to list all the property that is covered under the financing statement. This form is essential for creditors, as it clarifies the personal and real property that secures a loan, providing protection in the event of default.

Form components explained

- Schedule of property covered by the financing statement.

- Borrower's alternative provisions for the UCC Schedule.

- Detailed definitions of equipment and collateral involved in the financing.

- Rights regarding income, rents, and profits associated with the property.

- Insurance and eminent domain rights related to the mortgaged property.

When this form is needed

This form is typically used when a borrower is seeking a loan secured by personal property or real estate. It is necessary for lenders to identify the collateral. Use the UCC Schedule to clearly outline all items that a financing statement secures in order to avoid disputes over property covered by the loan.

Who can use this document

- Lenders seeking to establish a secured interest in personal or real property.

- Borrowers who are obtaining financing through loans secured by their assets.

- Attorneys or legal professionals involved in drafting financing statements.

- Business owners needing to clarify the collateral tied to their financing agreements.

Instructions for completing this form

- Identify the parties involved: borrower (debtor) and lender (secured party).

- List all items of collateral and property being secured under the financing statement.

- Include any provisions or stipulations that may alter the terms of the UCC Schedule.

- Review the completed document for accuracy, ensuring all necessary details are included.

- Secure signatures from all parties to validate the document.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to thoroughly list all collateral covered by the financing statement.

- Not including alternative provisions that may affect the secured property.

- Incomplete signatures or dates that could render the document invalid.

- Neglecting to check local state requirements before submission.

Benefits of using this form online

- Convenient access to downloadable forms without the need for in-person visits.

- Editability allows for customization specific to your legal needs.

- Reliable templates crafted by licensed attorneys to ensure legal compliance.

Legal use & context

- The UCC Schedule is used in secured transactions to clarify the assets involved.

- Proper use of this form helps in preventing disputes over property rights.

- This form increases the lender's security in the event of borrower default.

Quick recap

- The UCC Schedule is vital for fully documenting secured financing agreements.

- Understanding the contents and requirements of the form ensures legal protection.

- Utilizing this form can facilitate smoother financial transactions between borrowers and lenders.

Looking for another form?

Form popularity

FAQ

In all cases, you should file a UCC-1 with the secretary of state's office in the state where the debtor is incorporated or organized (if a business), or lives (if an individual).

UCC-1 Financing Statements do not have to be signed by either the Debtor or Secured Party; however, they must be authorized.Although the UCC-1 Financing Statement does not require signatures, any attachment such as the legal description or special terms and conditions may require the signature of the Debtor.

Having a UCC filed on your business credit report can have negative effects in general on your overall credit risk, scoring and other associated risk analysis, (across all three business credit bureaus) and can even kill your chances at getting financing for your business.

Filer Information. Name and phone number of contact at filer. Email contact at filer. Debtor Information. Organization or individual's name. Mailing address. Secured Party Information. Organization or individual's name. Mailing address. Collateral Information. Description of collateral.

A UCC filing is a legal notice a lender files with the secretary of state when they have a security interest against one of your assets. It gives notice that the lender has an interest, or lien, against the asset being used by you to secure the financing. The term UCC filing comes from the uniform commercial code.

In all cases, you should file a UCC-1 with the secretary of state's office in the state where the debtor is incorporated or organized (if a business), or lives (if an individual).

Why file a UCC-3 form? The UCC-3 is the Swiss-Army-Knife of forms. Unlike a UCC 1, a UCC 3 can be used for multiple purposes. The actions one can take are Amendment, Assignment, Continuation, and Termination.

A UCC filing is a legal notice a lender files with the secretary of state when they have a security interest against one of your assets. It gives notice that the lender has an interest, or lien, against the asset being used by you to secure the financing. The term UCC filing comes from the uniform commercial code.

A UCC lien is a claim against your business assets under the U.S. Uniform Commercial Code.If you borrow money, a UCC filing simply lets the lender establish a priority claim on your assets. If your company goes belly up, the lien makes it easier for the lender to collect its due.