UCC-1 for Real Estate

What is this form?

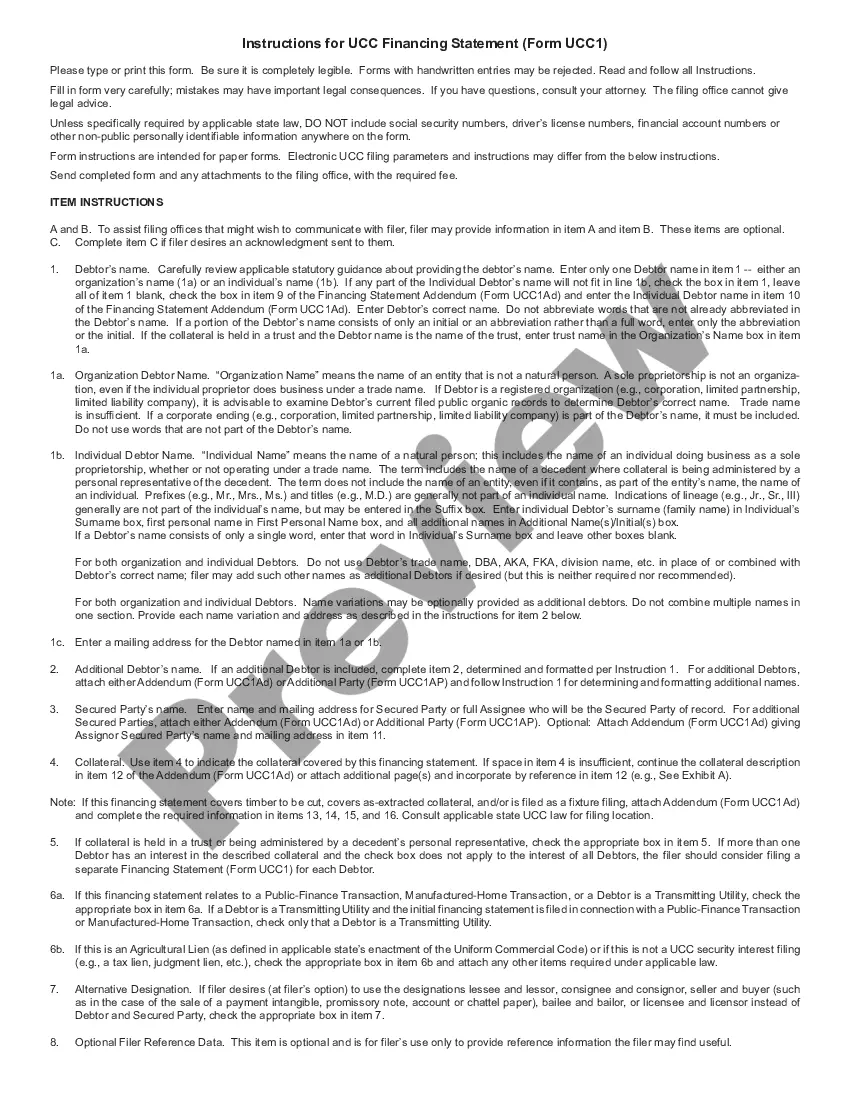

The UCC-1 for Real Estate is a legal document used to file a financing statement that secures a lender's interest in the personal property of a borrower. Unlike other forms that may pertain to general property liens, this specific form is crucial for establishing security interests in real estate by notifying other creditors about the lender's claim, thus helping to protect their investment.

What’s included in this form

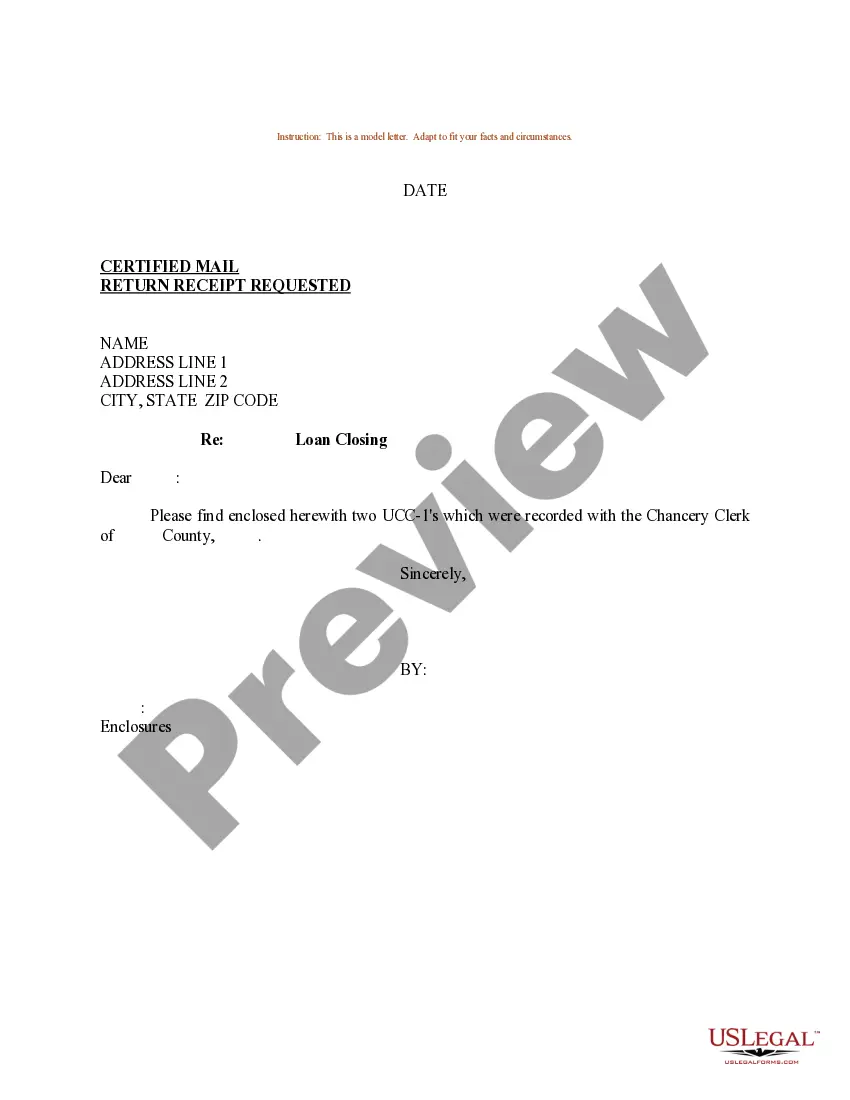

- Date: The date when the form is completed.

- Private: Indicates the confidentiality of the information.

- Certified Mail Return Receipt Requested: Ensures that documentation of delivery is retained.

- Name: The name of the individual or entity involved in the transaction.

- Address Line 1: The mailing address for communication.

- Address Line 2: Additional mailing address details if necessary.

- City, State, Zip Code: The location details required for the recipient.

Situations where this form applies

This form should be used when a lender wants to secure a lien on a borrower's real estate through a UCC filing. It is commonly employed during real estate transactions, especially when financing is involved, to provide public notice of the lender's claim to the property being financed. Completing this form is essential to protect the lender's interest in case of default or bankruptcy.

Who needs this form

- Lenders seeking to secure their interest in a borrower's real estate.

- Borrowers who are refinancing existing loans or obtaining new loans using real estate as collateral.

- Real estate professionals who are involved in transactions that require financing statements.

Steps to complete this form

- Identify the parties involved, including their names and addresses.

- Specify the date on which the form is completed.

- Indicate that the mailing method is certified mail with return receipt to ensure proof of delivery.

- Fill in the recipient's mailing address, including city, state, and zip code.

- Review the information for accuracy before submission.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. It is important to verify if your state's regulations require any additional acknowledgments or signatures to ensure its legality.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include accurate and complete addresses for all parties.

- Not specifying the correct date, which can affect the validity of the filing.

- Omitting the mailing method requirement, which is crucial for legal accountability.

- Neglecting to check specific state filing requirements, which can impact enforceability.

Advantages of online completion

- Convenient access to necessary forms without the need for in-person visits.

- Editable formats to allow for easy customization to meet specific needs.

- Reliable templates drafted by licensed attorneys, ensuring legal compliance.

Looking for another form?

Form popularity

FAQ

UCC-1 Filings Explained If you're approved for a small-business loan, a lender might file a UCC financing statement or a UCC-1 filing. This is just a legal form that allows for the lender to announce lien on a secured loan.

What does UCC stand for? UCC stands for Uniform Commercial Code. The UCC is a set of laws concerning commercial transactions, such as the sale of goods. It also covers secured transactions, where a lender gains the right to foreclose on a borrower's collateral should the borrower default on the loan.

Having a UCC filed on your business credit report can have negative effects in general on your overall credit risk, scoring and other associated risk analysis, (across all three business credit bureaus) and can even kill your chances at getting financing for your business.

A UCC filing, also known as a UCC lien or a UCC-1, is a financing statement which lenders can file against your business with your secretary of state.This might be a piece of equipment, a vehicle, property, or even a blanket lien naming all your assets.

A UCC-1 financing statementalso sometimes referred to as a 'UCC-1 filing,' a 'UCC lien,' or simply a 'UCC-1'is a form that creditors use to create a lien against a debtor's property.

The UCC is a model code sponsored by the American Law Institute and the Uniform Law Commission that governs commercial transactions and has been enacted, in one form or another, in each of the 50 states. Generally, Articles 3 and 9 of the UCC are relevant to mortgage loans.

As the word Uniform in its title suggests, a primary purpose of the UCC is to make business activities more predictable and efficient by making business laws highly consistent across all American states.

A UCC lien is a claim against your business assets under the U.S. Uniform Commercial Code.If you borrow money, a UCC filing simply lets the lender establish a priority claim on your assets. If your company goes belly up, the lien makes it easier for the lender to collect its due.

In general, Article 9 of the Uniform Commercial Code applies only to security interests in personal property and fixtures, not liens on real property.