Subordination Construction Loan

What this document covers

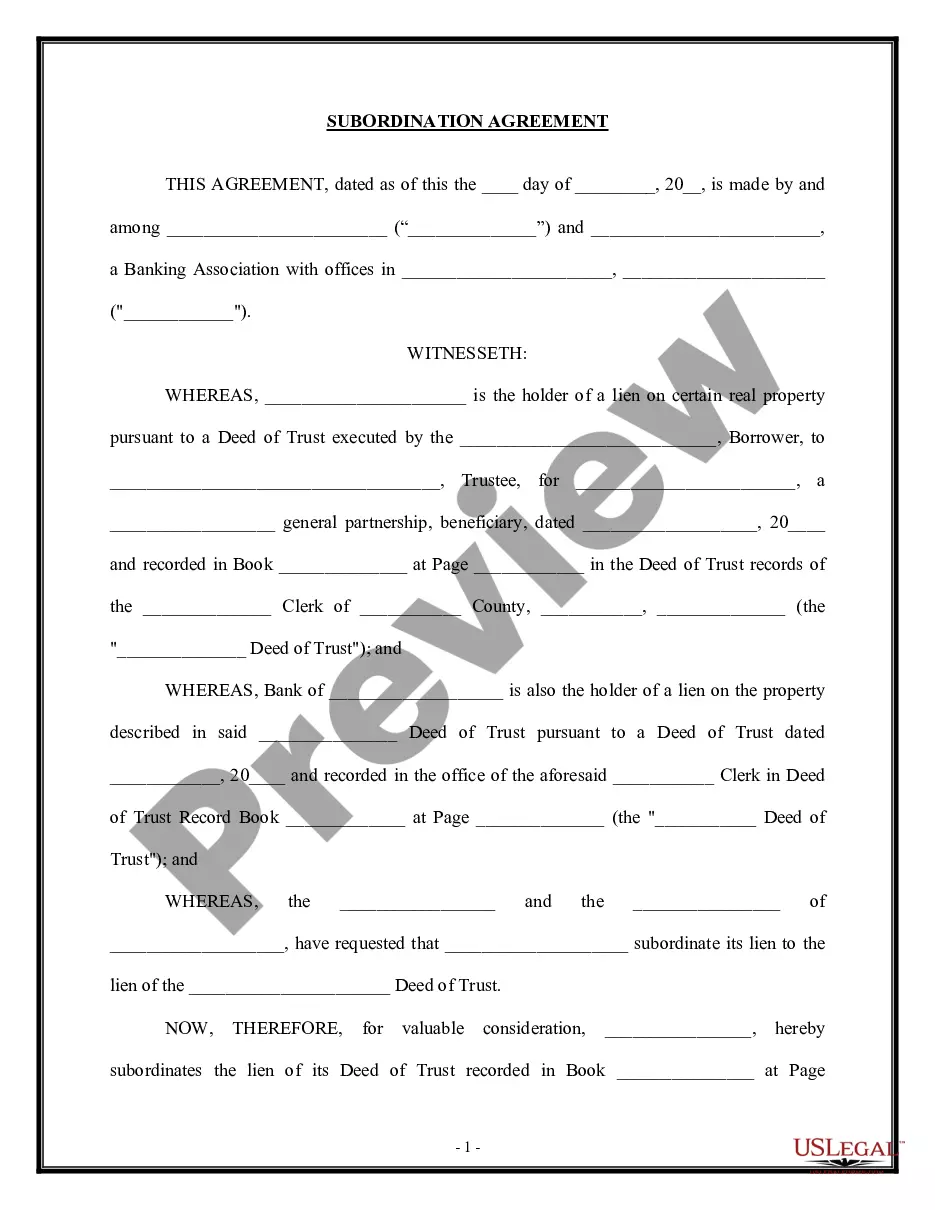

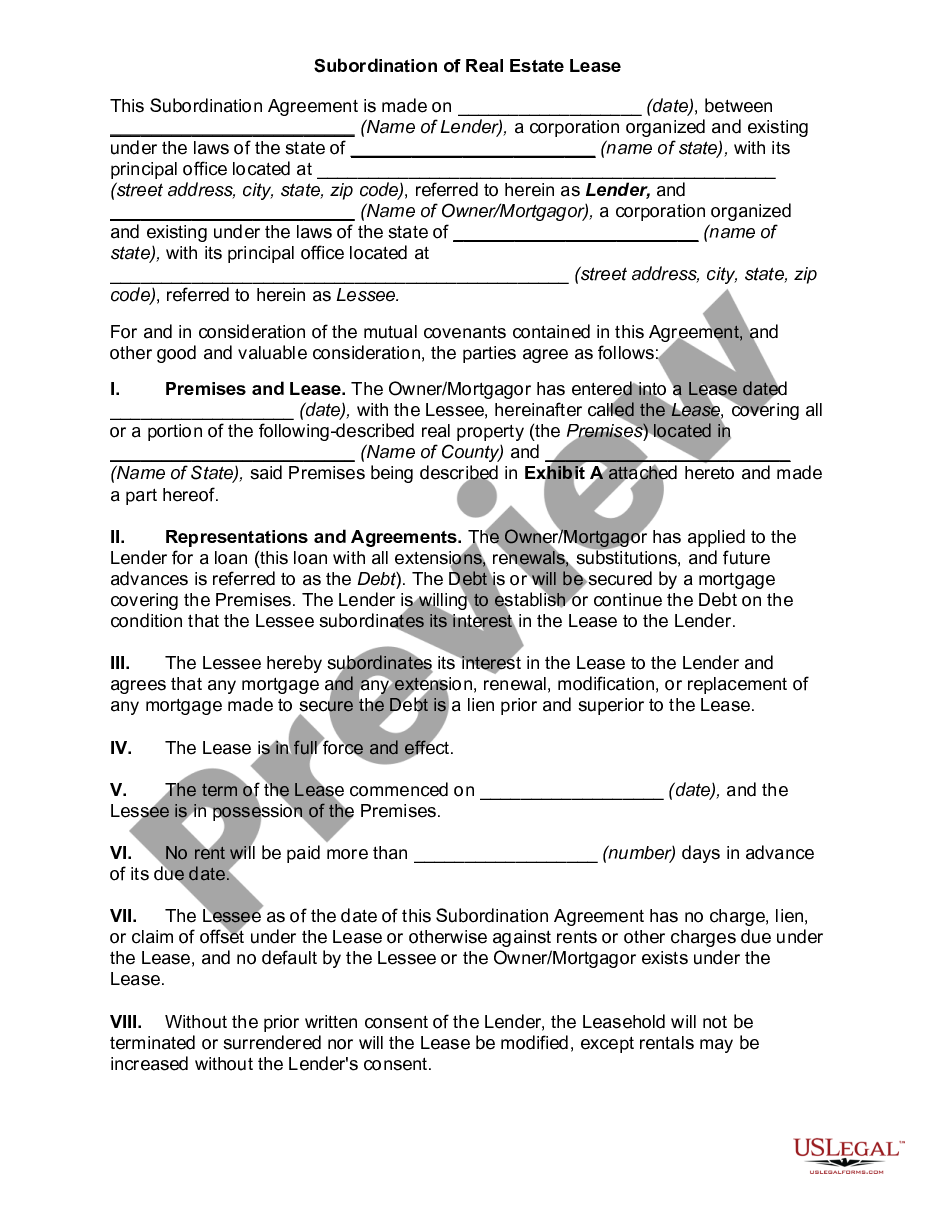

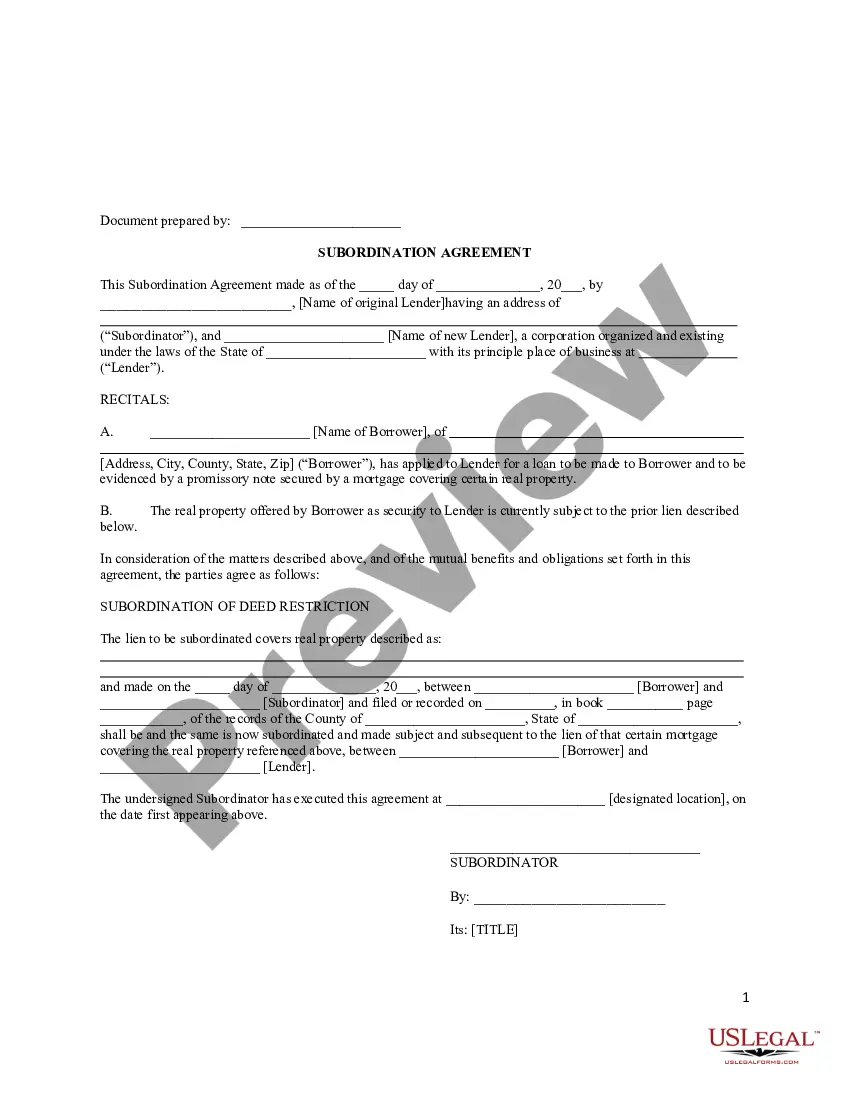

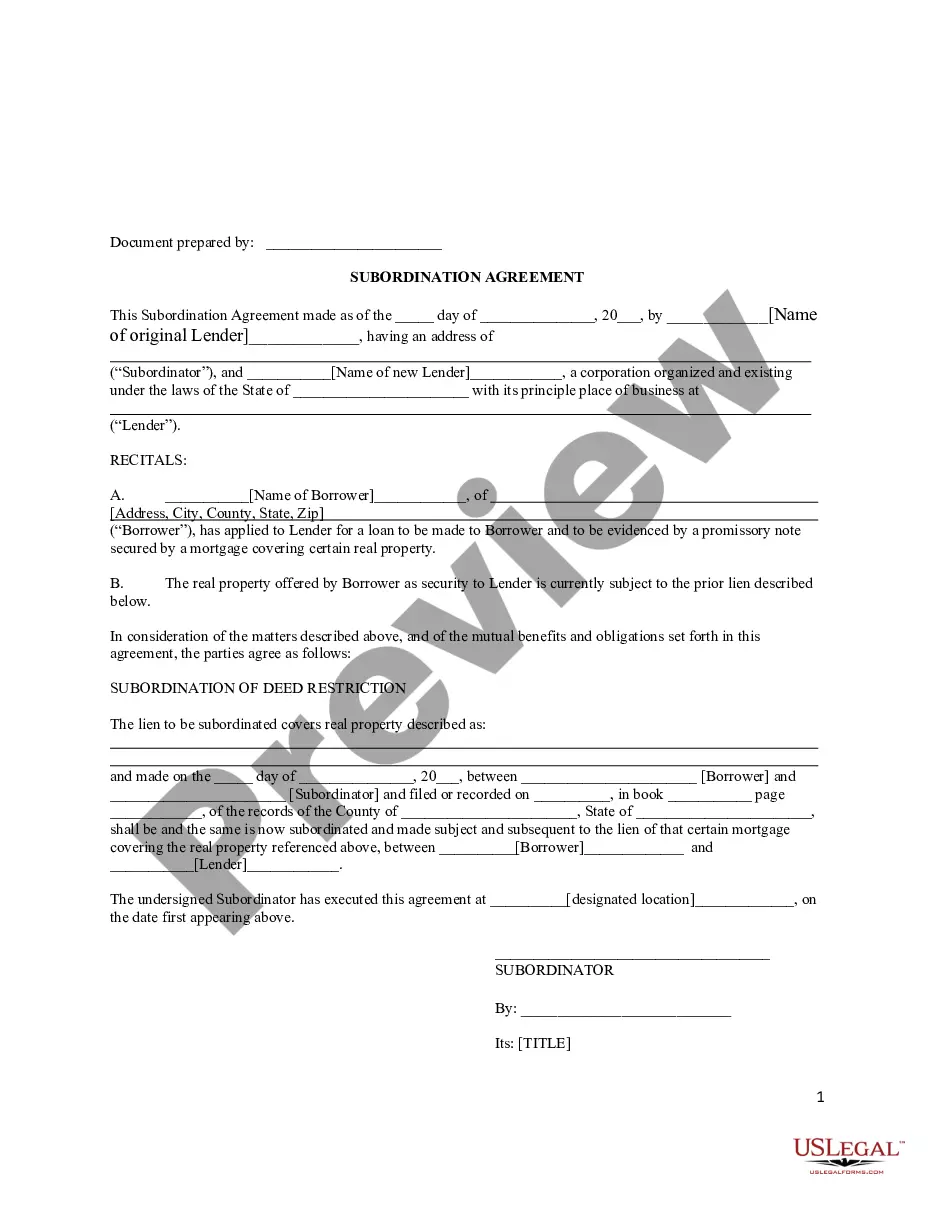

The Subordination Construction Loan form is a legal document that establishes the priorities of claims against property, specifically in relation to a construction loan mortgage. This form includes clauses that clarify the conditions under which a mortgage will take a subordinate position to a construction loan mortgage, allowing for financing to proceed without interference from existing liens. This form is crucial in real estate transactions involving construction financing, ensuring all parties understand their rights and obligations.

Main sections of this form

- Covenant of subordination, allowing the mortgage to be subordinate to a specified construction loan mortgage.

- Details regarding the loan amount, with a placeholder for entering the principal sum.

- Conditions for subordination, including stipulations regarding the default status of the mortgage.

- Provisions for the mortgagee's discretion in approving larger loan amounts.

When to use this document

This form is typically used when a property owner intends to secure a construction loan and needs to ensure that the lender's mortgage will rank below that of the construction loan. It is particularly relevant in situations where existing mortgages may complicate the financing or construction process, making it essential to clarify the order of claims on the property before proceeding with construction.

Who this form is for

This form is intended for:

- Property owners seeking construction financing.

- Mortgage lenders who need to establish priorities for their loans.

- Real estate professionals facilitating construction projects.

- Developers who require clarification of loan terms and subordinations.

Instructions for completing this form

- Identify the parties involved, including the mortgagee and borrower.

- Specify the total amount of the construction loan in the designated field.

- Review the subordination clauses to understand the obligations outlined.

- Ensure the mortgage is not in default before proceeding with the completion.

- Have all parties sign and date the document to make it legally binding.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, verifying your jurisdiction's requirements before finalization is always recommended to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to accurately complete the loan amount field, which could lead to confusion about financing terms.

- Not reviewing the implications of subordination, potentially leading to disputes later.

- Neglecting to confirm that the original mortgage is not in default.

- Overlooking signatures from all required parties, affecting the document's validity.

Benefits of completing this form online

- Convenience: Easily downloadable and accessible at any time from the comfort of your home.

- Editability: Customize the form as needed to fit specific transaction details.

- Reliability: Created by licensed attorneys, ensuring that you have a legally sound document.

Looking for another form?

Form popularity

FAQ

When you get a mortgage loan, the lender will likely include a subordination clause essentially stating that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender if a homeowner defaults.

A subordination agreement prioritizes debts, ranking one behind another for purposes of collecting repayment from a debtor in the event of foreclosure or bankruptcy. A second-in-line creditor collects only when and if the priority creditor has been fully paid.

The party that primarily benefits from a subordination clause in real estate is the lender. However, if you decide to pursue a second mortgage, then the subordination clause prioritizes the first lender's repayment and contract rights. The most common application of subordination clauses is when refinancing a property.

Purpose of a Subordination Agreement A subordination agreement is generally used when there are two mortgages and the mortgagor needs to refinance the first mortgage. It acknowledges that one party's interest or claim is superior to another in case the borrower's assets need to be liquidated to repay debts.

Despite its technical-sounding name, the subordination agreement has one simple purpose. It assigns your new mortgage to first lien position, making it possible to refinance with a home equity loan or line of credit. Signing your agreement is a positive step forward in your refinancing journey.

A subordination clause is a clause in an agreement which states that the current claim on any debts will take priority over any other claims formed in other agreements made in the future.

The lender may require a subordination agreement to protect its interests in the event that the borrower deposits additional liens on the property, such as if the borrower were to take out a second mortgage.

Subordinate financing is debt financing that is ranked behind that held by secured lenders in terms of the order in which the debt is repaid. "Subordinate" financing implies that the debt ranks behind the first secured lender, and means that the secured lenders will be paid back before subordinate debt holders.