This package provides many different tools for a homeowner to prevent foreclosure of a home. The forms cover various means to obtain assistance at all stages of the foreclosure process. Purchase of this package is a savings of 63% over purchase of the forms individually! Included in this package are the following forms:

1. Letter to Lender for Produce the Note Request

2. Offer by Borrower of Deed in Lieu of Foreclosure

3. Motion to Dismiss Foreclosure Action and Notice of Motion

4. Petition or Complaint to Enjoin Nonjudicial Foreclosure Sale and for Declaratory Relief

5. Petition to Enjoin Foreclosure Sale and Seeking Ascertainment of Amount Owed on Note and Deed of Trust

6. Qualified Written RESPA Request to Dispute or Validate Debt

7. Request to Lender or Loan Servicer for Loan Modification Due to Financial Hardship - Requesting Change to Fixed Rate of Interest of Adjustable Rate

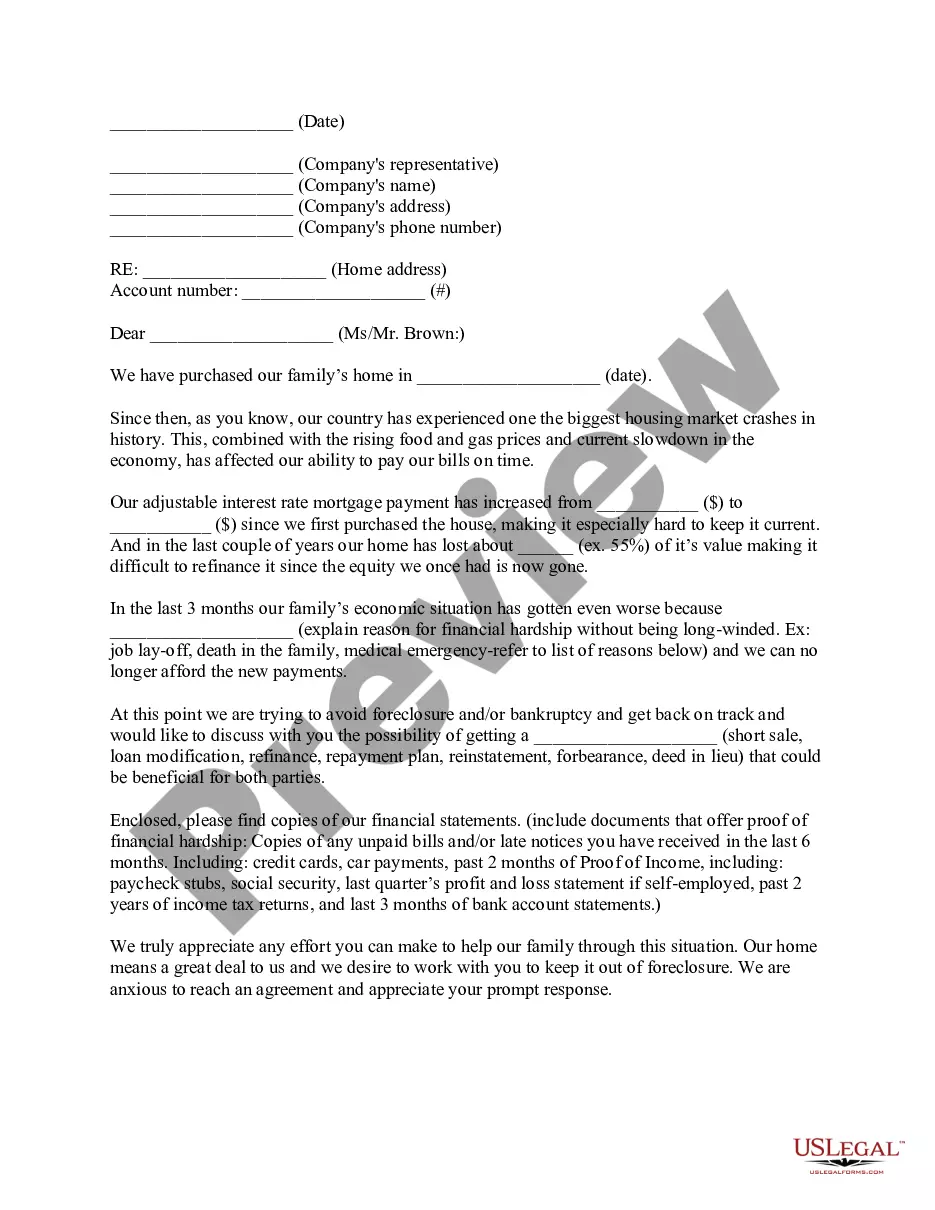

8. Hardship Letter to Mortgagor or Lender to Prevent Foreclosure

9. Sample Letter for Short Sale Request to Lender

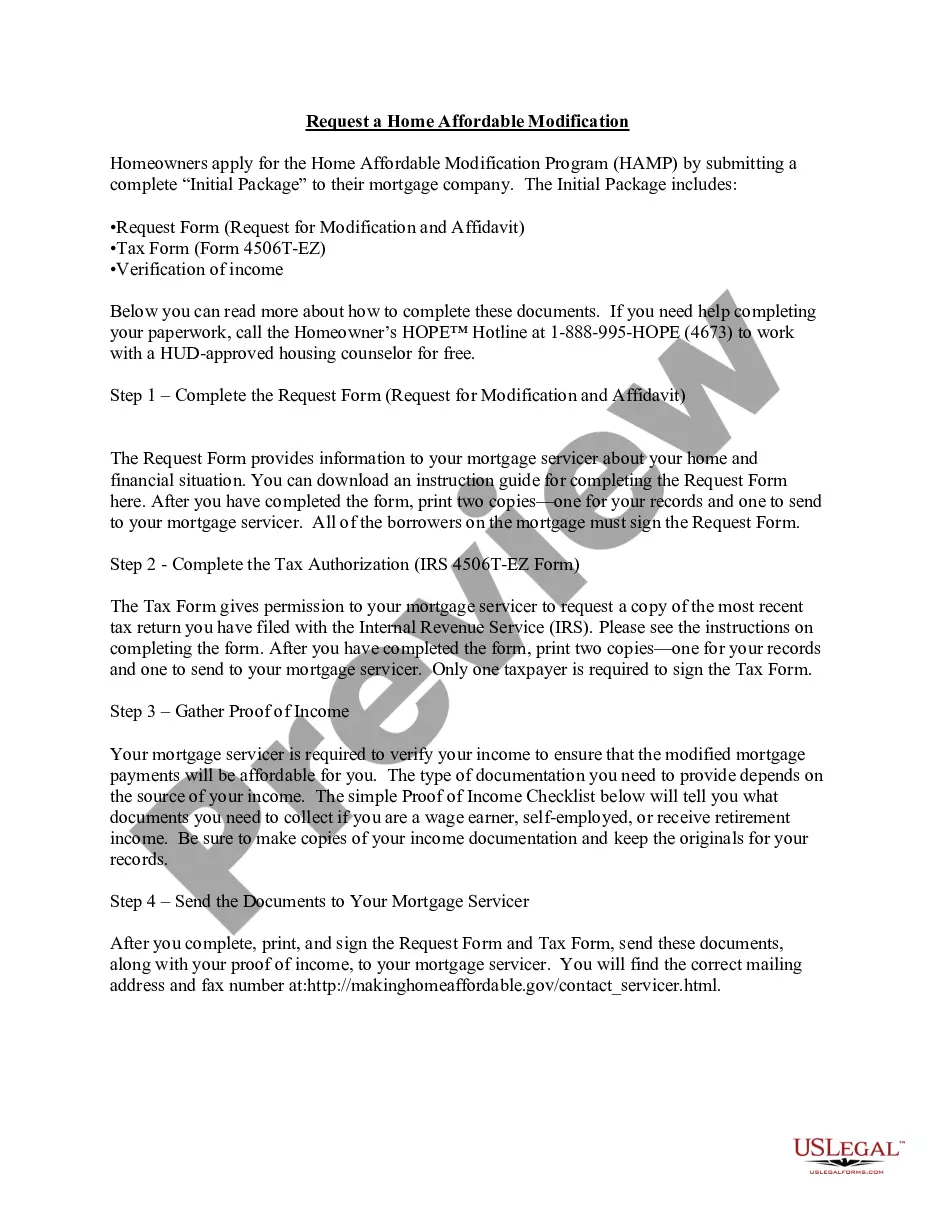

10. MHA Request for Short Sale