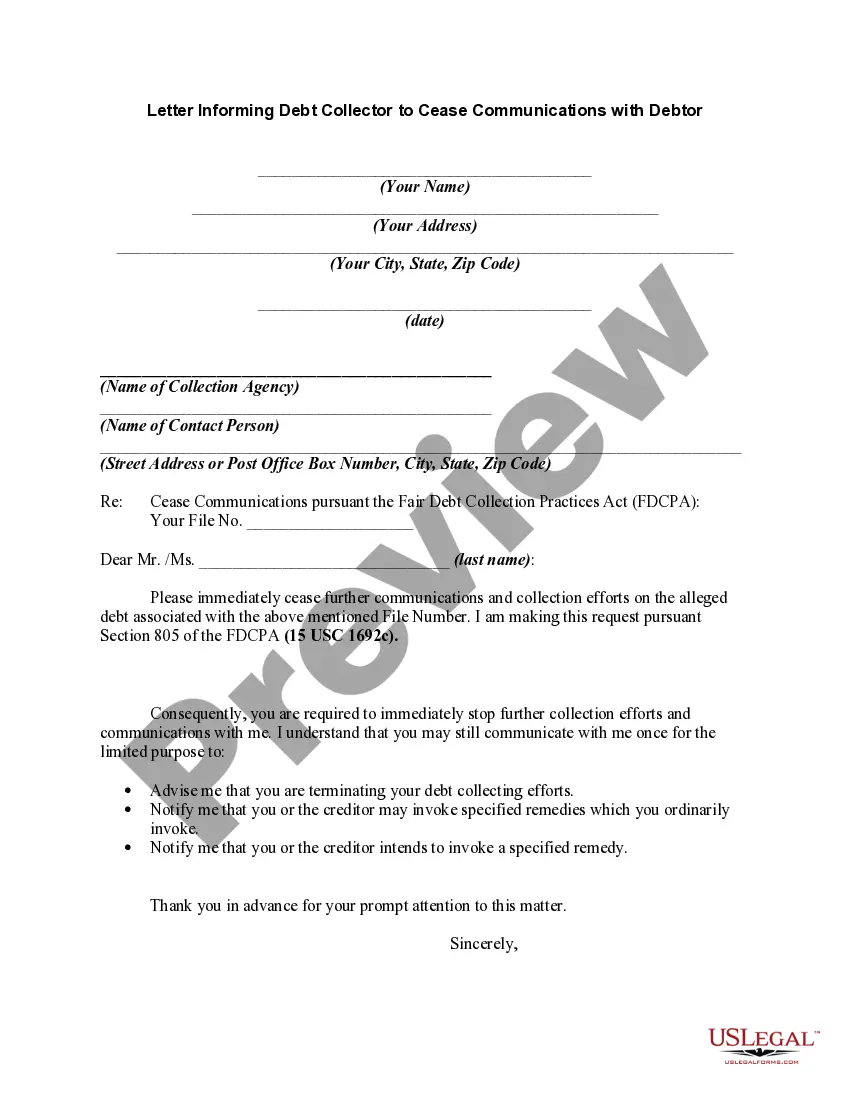

Section 805 communications telling debt collector to stop communicating with you

Overview of this form

This form is a written communication that informs a debt collector to cease all attempts to contact you regarding an alleged debt. By utilizing this Section 805 communication, you are exercising your rights under the Fair Debt Collection Practices Act (FDCPA). It differs from other debt-related letters by specifically mandating the end of all communications, unless permitted by the FDCPA for limited purposes.

Key parts of this document

- Your contact information: including your address and the date.

- The debt collector's information: including the company name and address.

- A clear statement requesting the cessation of communications.

- Provisions of the FDCPA that detail conditions under which communications may resume.

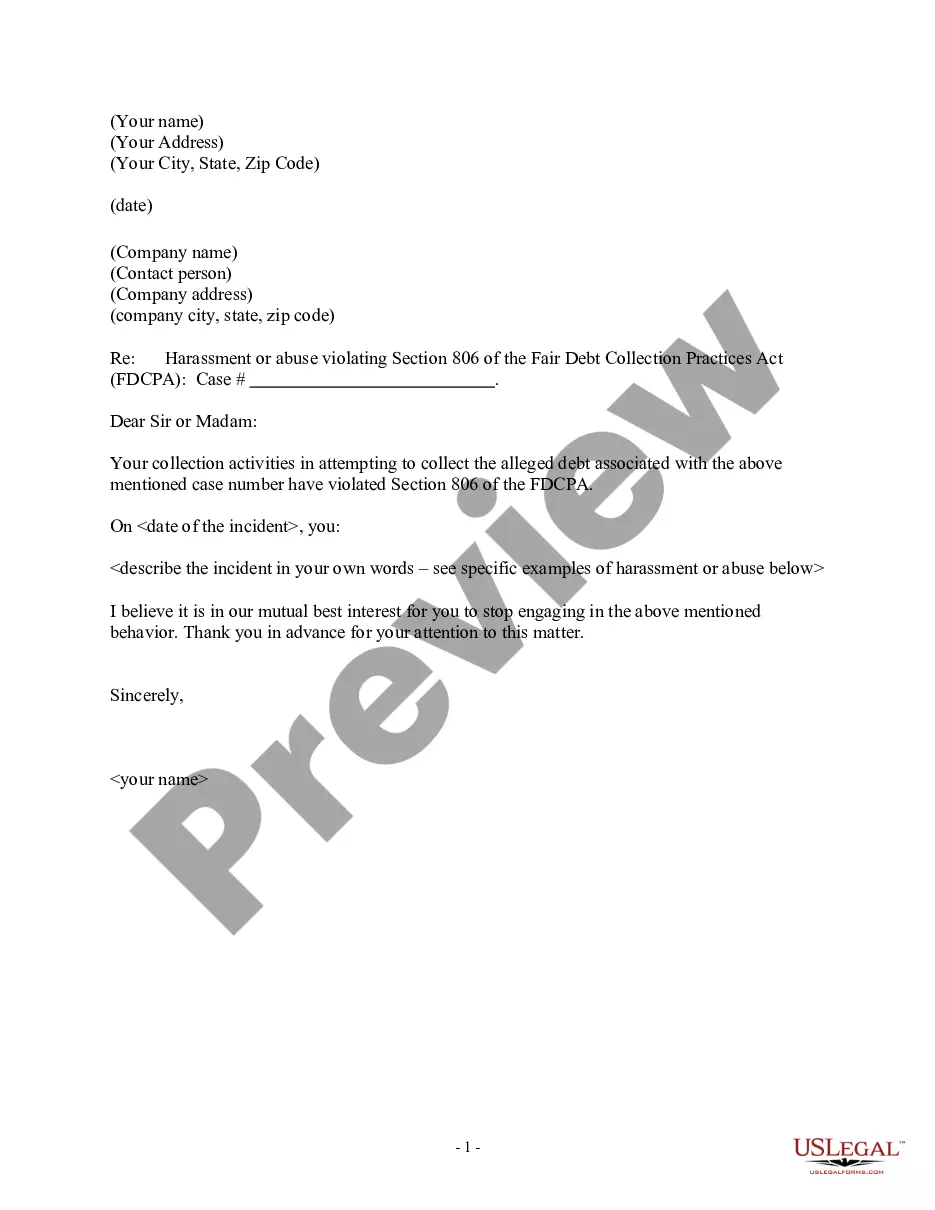

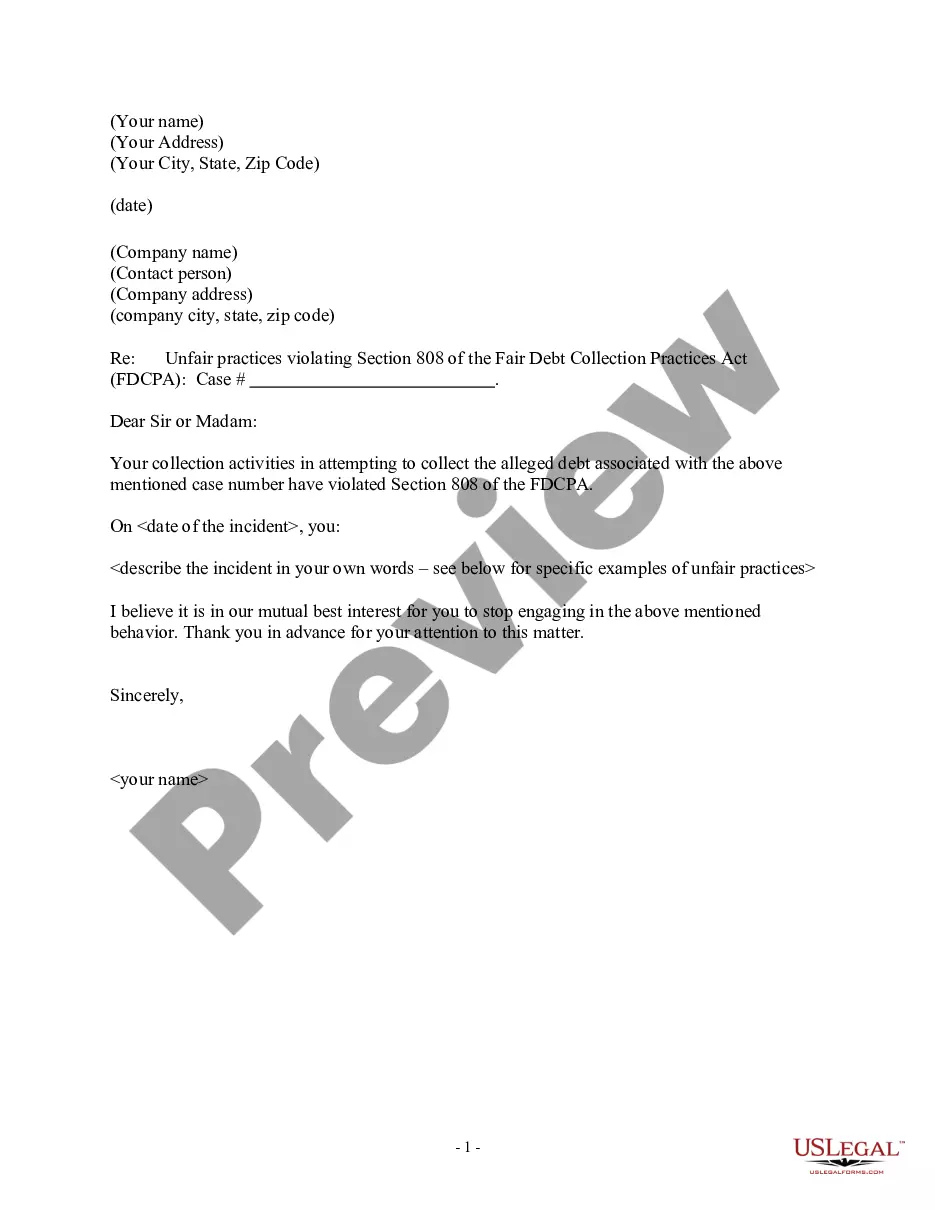

- Follow-up letters to reinforce your cease communication request and articulate potential violations.

- Signature section to validate the document.

When this form is needed

You should use this form when you wish to stop a debt collector from contacting you about an alleged debt. This can be particularly important if you find the communications are causing you stress, if you believe the debt is invalid, or if you simply prefer not to engage with the collector. This form is your formal way of demanding that they respect your request under federal law.

Who can use this document

- Individuals who are being contacted by debt collectors regarding alleged debts.

- Consumers who wish to assert their rights under the FDCPA.

- People who have found debt collection efforts to be invasive or distressing.

- Anyone who disputes the validity of a debt and seeks to stop further communication with collectors.

Steps to complete this form

- Enter your address and the date at the top of the letter.

- Fill in the debt collector's name and address.

- Select and copy the appropriate wording from the follow-up letter section to clearly communicate your request.

- Sign the letter to authenticate your demand.

- Mail the completed form via certified or registered mail to ensure delivery confirmation.

Notarization guidance

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to send the letter via certified mail, which can complicate proof of communication.

- Not including specific details about the alleged debt, which can lead to confusion.

- Neglecting to keep a copy of the letter for your records.

- Using vague language instead of the required legal terminology as specified in the FDCPA.

Why complete this form online

- Convenient and straightforward access to legal documents without the need for legal consultation.

- Editable and customizable format allows you to tailor the letter to your specific situation.

- Reliable templates drafted and reviewed by licensed attorneys to ensure compliance with legal standards.

Legal use & context

- This form is legally recognized under the FDCPA, which governs debt collection practices in the United States.

- Consumers have the right to cease communications with debt collectors under federal law.

- Non-compliance by the debt collector after receiving this notice can be grounds for legal action.

Looking for another form?

Form popularity

FAQ

The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone.

Write a Letter Requesting To Cease Communications. Document All Contact and Harassment. File a Complaint With the FTC. File a Complaint With Your State's Agency. Consider Suing the Debt Collection Agency for Harassment.

The FDCPA prohibits debt collectors from calling you repeatedly, using profane language, making threats, or otherwise harassing you. If a debt collector is constantly calling you and causing you stress, sending a cease and desist letter can stop the collector from harassing you.

Answer the phone and explain you're not the person they're looking for. Tell them that the number they're calling is not the right one. Send a cease and desist letter to request that they stop contacting you.

Yes. The federal Fair Debt Collection Practices Act specifically gives you the right to sue a debt collector for harassment. If a debt collector is found to have engaged in harassing behavior, you are entitled to up to $1,000 in damages, along with court costs and attorney fees.

You have the right to tell a debt collector to stop communicating with you. To stop communication, send a letter to the debt collector and keep a copy of the letter. If you don't want a debt collector to contact you again, write a letter to the debt collector saying so.

Debt Collectors Can't Call You Repeatedly to Harass You This means that while the FDCPA doesn't place a specific limit on the number of calls debt collectors can make, it prohibits them from calling you multiple times just to harass you. (15 U.S. Code § 1692d).

Of course, if the debt is invalid or does not apply to you, you have every right to stop the debt collection letters coming to your home. You can do this by writing to the collector and telling him/her that the debt they are trying to pursue is not owed by you.

How Long Can a Debt Collector Pursue an Old Debt? Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collect debts. In most states, they run between four and six years after the last payment was made on the debt.