Credit Inquiry

Overview of this form

The Credit Inquiry form is designed to facilitate the evaluation of a business's creditworthiness. This form allows businesses to report and request credit information, helping lenders or suppliers make informed decisions. Unlike standard credit applications, this form focuses specifically on credit history and payment behavior, ensuring a comprehensive assessment of credit reliability.

Key parts of this document

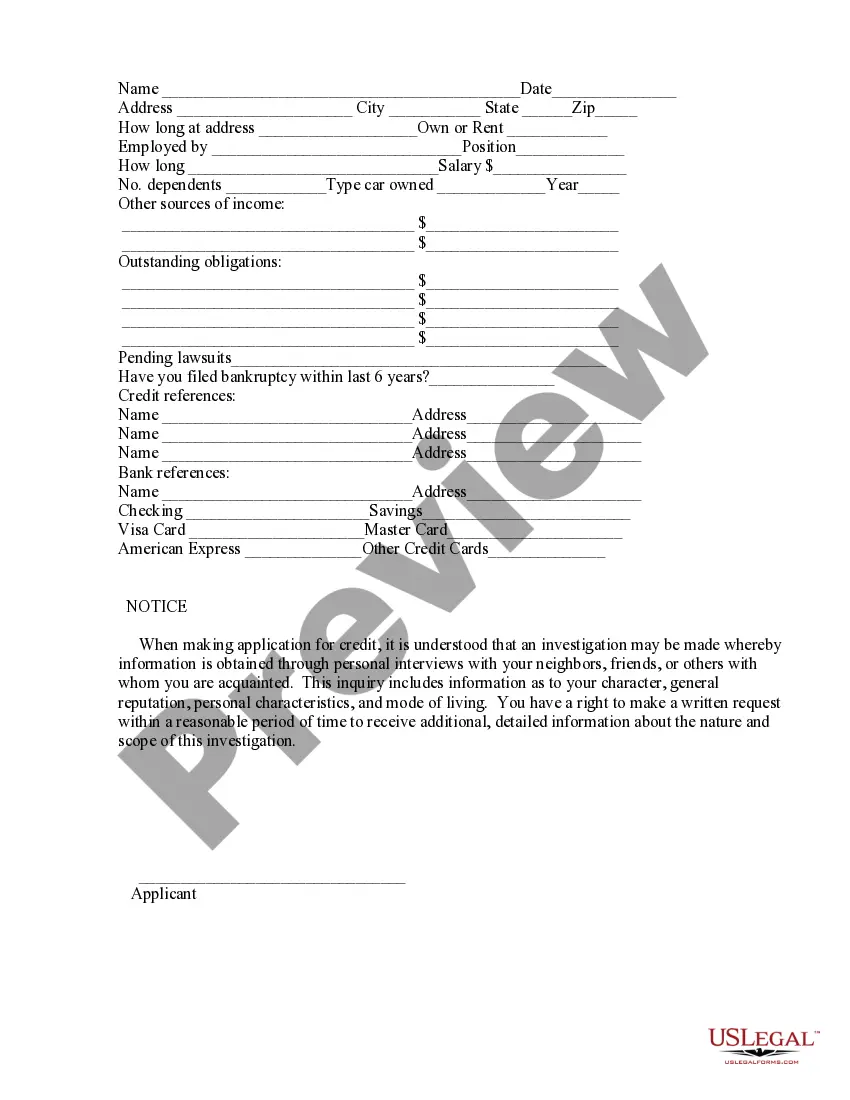

- Questions on payment history: Indicates whether payments have been made on time.

- Credit recommendations: Includes fields for suggestions regarding extending credit.

- Comments section: Provides space for any additional remarks relevant to the credit evaluation.

- Nature of the account: Allows classification of the account's status, including excellent or poor performance.

- Amount past due: Details any outstanding payment amounts that could affect credit decisions.

When this form is needed

This form should be used when a business seeks to evaluate the creditworthiness of another business or entity before deciding to extend credit. It is particularly useful in situations involving new credit applications, ongoing vendor relationships, or any instance where credit assessments are necessary to mitigate risk.

Intended users of this form

- Lending institutions that need to assess loan applications.

- Suppliers considering offering credit terms to customers.

- Businesses required to check the credit history of partners or clients.

- Account managers tasked with evaluating the risk of extending credit.

Instructions for completing this form

- Identify the businesses involved: Clearly state the names and addresses of both the creditor and the debtor.

- Select payment history indicators: Mark "Yes" or "No" for each payment history inquiry to reflect timely payments.

- Fill in the past due amounts: Enter any overdue payment amounts that may influence credit decisions.

- Add comments: Use the provided space to include any relevant information that could affect the credit assessment.

- Sign and date the form: Ensure all necessary parties sign the document to validate its contents.

Does this form need to be notarized?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Leaving sections blank: Ensure all relevant fields are filled out to avoid incomplete information.

- Providing inaccurate payment history: Double-check that payment records are correct to maintain credibility.

- Not obtaining necessary signatures: Ensure all required parties sign the form for validity.

Benefits of completing this form online

- Convenience: Access the form anytime and anywhere to complete your credit inquiry quickly.

- Editability: Easily make modifications to reflect current credit conditions without hassle.

- Reliability: Utilize forms prepared by licensed attorneys to ensure legal compliance and clarity in documentation.

Looking for another form?

Form popularity

FAQ

Letter of Explanation (LOE): credit inquiry explanation. Momina. The Inquiry letter is used to explain all credit inquiries in the last 120 days. When the lender pulls credit OR when credit is automatically pulled at borrower submission.

Begin the letter with the date, a salutation, and an introduction of the incident or issue. Provide a short but detailed description without having to add unnecessary terms and phrases. Provide an explanation of the steps you've taken to rectify the error or to complete the missing information.

Disputing hard inquiries on your credit report involves working with the credit reporting agencies and possibly the creditor that made the inquiry. Hard inquiries can't be removed, however, unless they're the result of identity theft. Otherwise, they'll have to fall off naturally, which happens after two years.

Give precise details of the situation or circumstances. Describe the facts that resulted in the current situation. Be truthful so that you may not find yourself in a difficult position. Provide supporting documents if they are available. Describe what you will do to make the correction.

According to FICO, Statistically, people with six inquiries or more on their credit reports can be up to eight times more likely to declare bankruptcy than people with no inquiries on their reports.

Facts. Include all the details with correct dates and dollar amounts. Resolution. Explain how and when the situation was resolved. Acknowledge. It's important that the letter outline why the problem won't arise again. Recognize if and how you could have avoided this mistake.

An acknowledgement of what happened. This demonstrates honesty and understanding of the necessity to repay the debt. A reason why it happened. Don't leave this to the underwriter's assumption. A statement of what is different now. Finally, if supporting documentation is available, include it.

Disputing hard inquiries on your credit report involves working with the credit reporting agencies and possibly the creditor that made the inquiry. Hard inquiries can't be removed, however, unless they're the result of identity theft. Otherwise, they'll have to fall off naturally, which happens after two years.

According to FICO, a hard inquiry from a lender will decrease your credit score five points or less. If you have a strong credit history and no other credit issues, you may find that your scores drop even less than that.