Qualified Personal Residence Trust One Term Holder

About this form

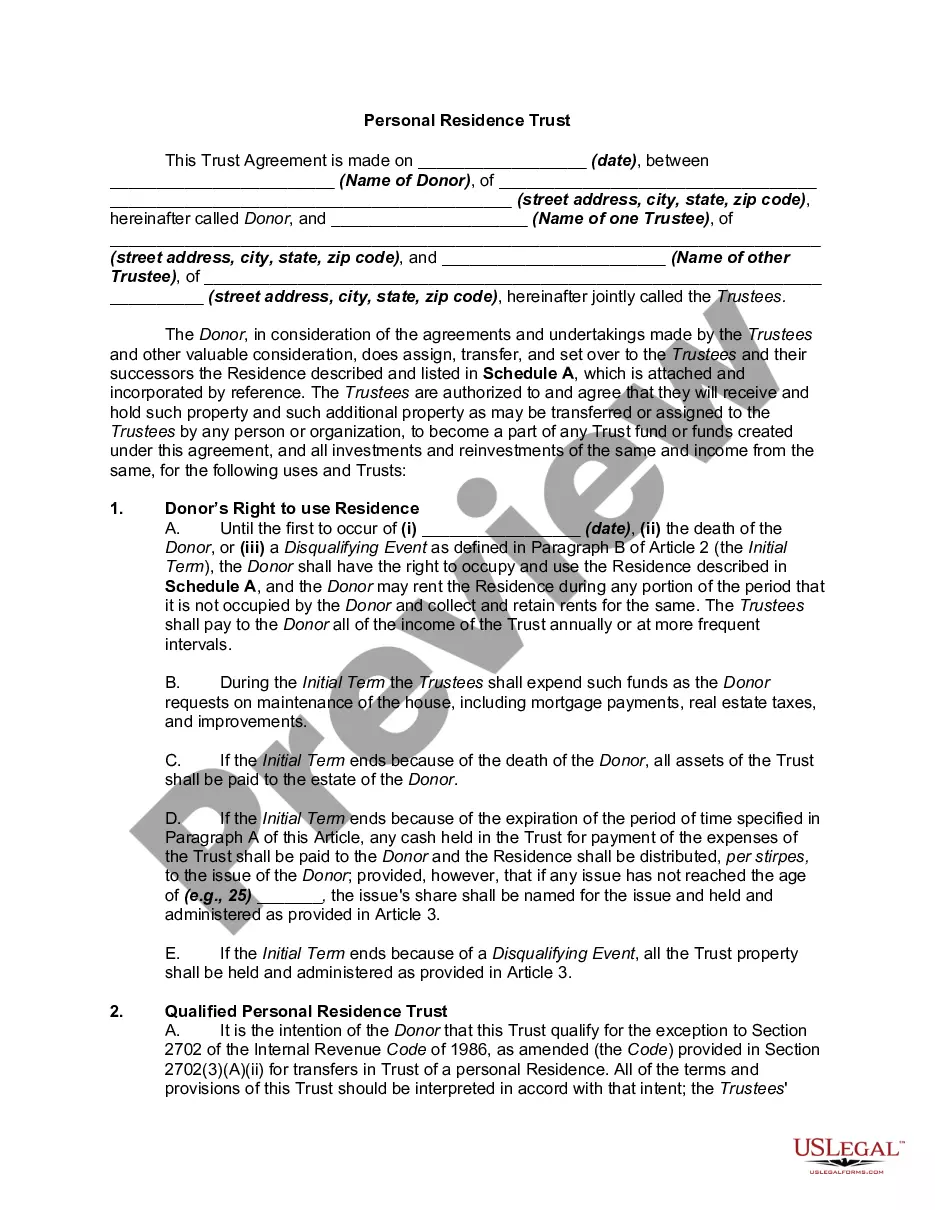

The Qualified Personal Residence Trust One Term Holder is a legal document used to establish a Qualified Personal Residence Trust (QPRT). This trust allows a donor to transfer a personal residence into a trust while retaining the right to live in it for a specified term. At the end of the term, the residence transfers to designated beneficiaries, usually the donor's children. This form offers significant tax advantages by allowing the donor to maintain control of the home while reducing the taxable value of their estate.

What’s included in this form

- Transferor and trustee identification: Names and addresses of the parties involved.

- Retained interest clause: Specifies the donor's retained rights and the irrevocability of the trust.

- Funding provisions: Details on the transfer of property into the trust and restrictions on additional contributions.

- Management of the residence: Outlines responsibilities for maintenance and expenses during the trust term.

- Trust termination: Specifies how and when the trust will terminate and how assets will be distributed.

When to use this document

This form is beneficial when a homeowner wants to reduce their estate tax liability while retaining the right to live in their home. It is particularly useful for parents transferring property to children and helps in estate planning, particularly when the value of a residence is significant. Using this form can also facilitate smooth transitions of property ownership upon the donor's passing.

Who should use this form

- Homeowners who wish to transfer their personal residence to their children or other beneficiaries.

- Individuals looking to prevent or minimize estate taxes associated with their property.

- Those who want to retain control and use of their home while ensuring a planned transfer of ownership.

Steps to complete this form

- Identify the parties: Enter the names and addresses of the transferor and trustee.

- Specify the property: Describe the residence being transferred, including its address.

- Set the term: Indicate the length of time that the transferor will retain the right to use the residence.

- Complete funding details: Provide information on any additional contributions to the trust.

- Sign and date the document: Ensure that the transferor and trustee sign the trust agreement.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, having the signatures notarized can enhance the validity of the document.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to accurately describe the property being transferred.

- Not specifying the term duration clearly.

- Omitting signatures or failing to date the trust agreement correctly.

- Not consulting with an attorney to ensure the trust complies with local laws.

Why complete this form online

- Convenience: Download and fill out the form at your own pace from anywhere.

- Editability: Easily make corrections or adjustments to the template as needed.

- Reliability: Access to forms created by licensed attorneys ensures legal compliance.

Quick recap

- The Qualified Personal Residence Trust allows for tax-efficient transfer of ownership of a primary residence.

- It helps maintain family control of property while reducing potential estate taxes.

- Proper completion and understanding of the trust's terms are crucial for legal validity.

Looking for another form?

Form popularity

FAQ

Because there's no limit on how long the QPRT must run, it's not uncommon to see QPRTs that were created 10 to 15 years ago finally expire today.

A Qualified Personal Residence Trust (QPRT) is a specific type of irrevocable trust that allows its creator to remove a personal home from his or her estate for the purpose of reducing the amount of gift tax that is incurred when transferring assets to a beneficiary.This tax can also be lowered with a unified credit.

A qualified personal residence trust (QPRT) is a trust to which a person (called the settlor, donor, or grantor) transfers his personal residence. The grantor reserves the right to live in the house for a period of years; this retained interest reduces the current value of the gift for gift tax purposes.

Specifically, a QPRT is an irrevocable grantor trust, which allows an individual to take advantage of the gift tax exemption by putting a personal residence, either primary or secondary, into a trust.Ultimately, a QPRT reduces estate tax to the grantor and benefits the grantor's heirs/beneficiaries.

Specifically, a QPRT is an irrevocable grantor trust, which allows an individual to take advantage of the gift tax exemption by putting a personal residence, either primary or secondary, into a trust. The grantor determines how long he will retain possession and use of the residence.

Why Create a QPRTYou can put in the Trust your primary residence or your vacation home. When you do that, you can quickly reduce your estate's size below the taxable threshold so that you don't pay any estate taxes when you pass the home to your heirs.Any appreciation in value in the house is not taxable.

Each taxpayer may have up to two QPRTs. Each QPRT may hold an interest in only one home. Therefore, if you wish to transfer your principal residence and a vacation home to a QPRT, you must create two separate trusts.

The QPRT transaction will be completely undone if you die before the retained income period ends. The value of the residence will be included in your taxable estate at its full fair market value as of the date of your death. Some other potential drawbacks should be considered as well.

A grantor may establish a QPRT for no more than two residences. The trusts can be funded using (1) a principal residence; (2) a vacation home or secondary residence; or (3) a fractional interest in either.