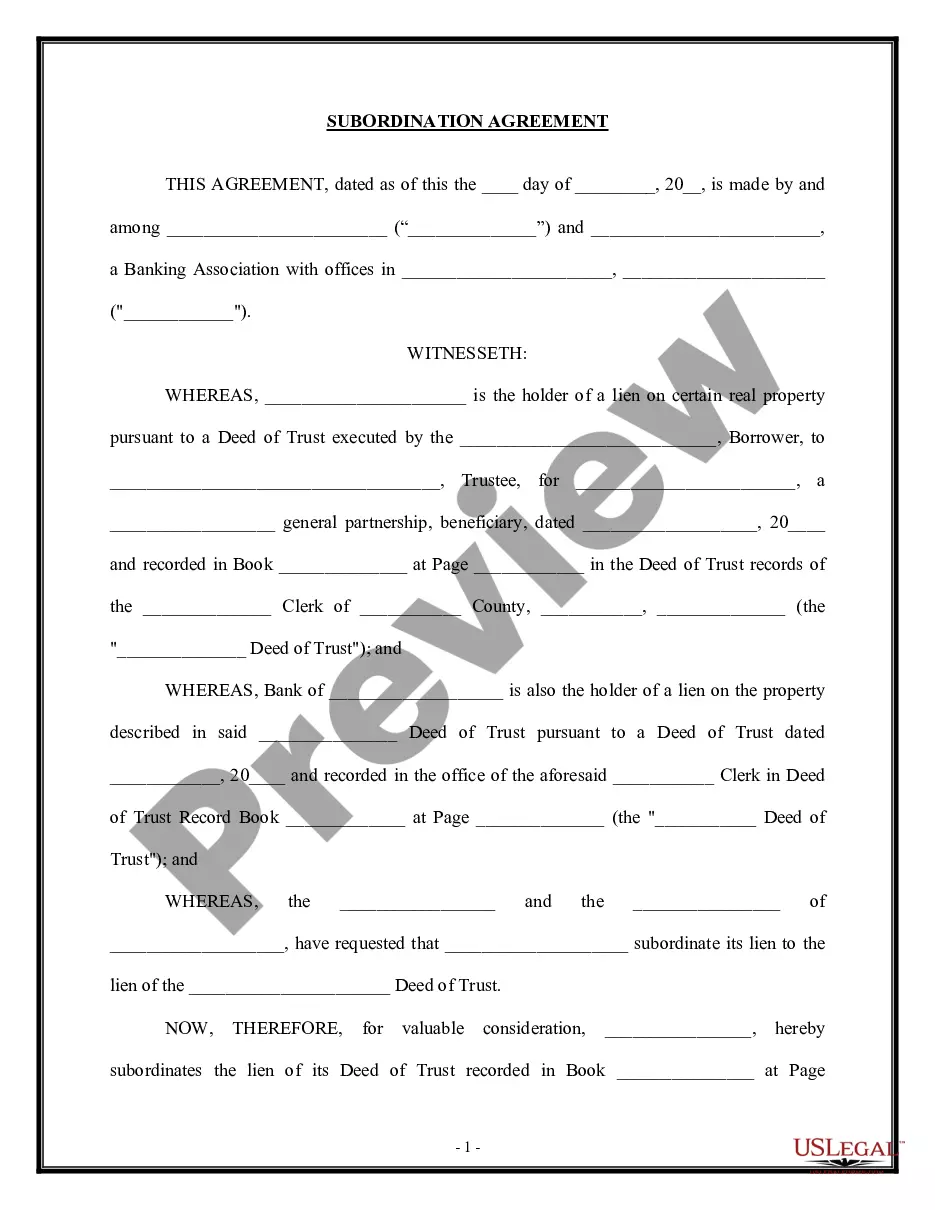

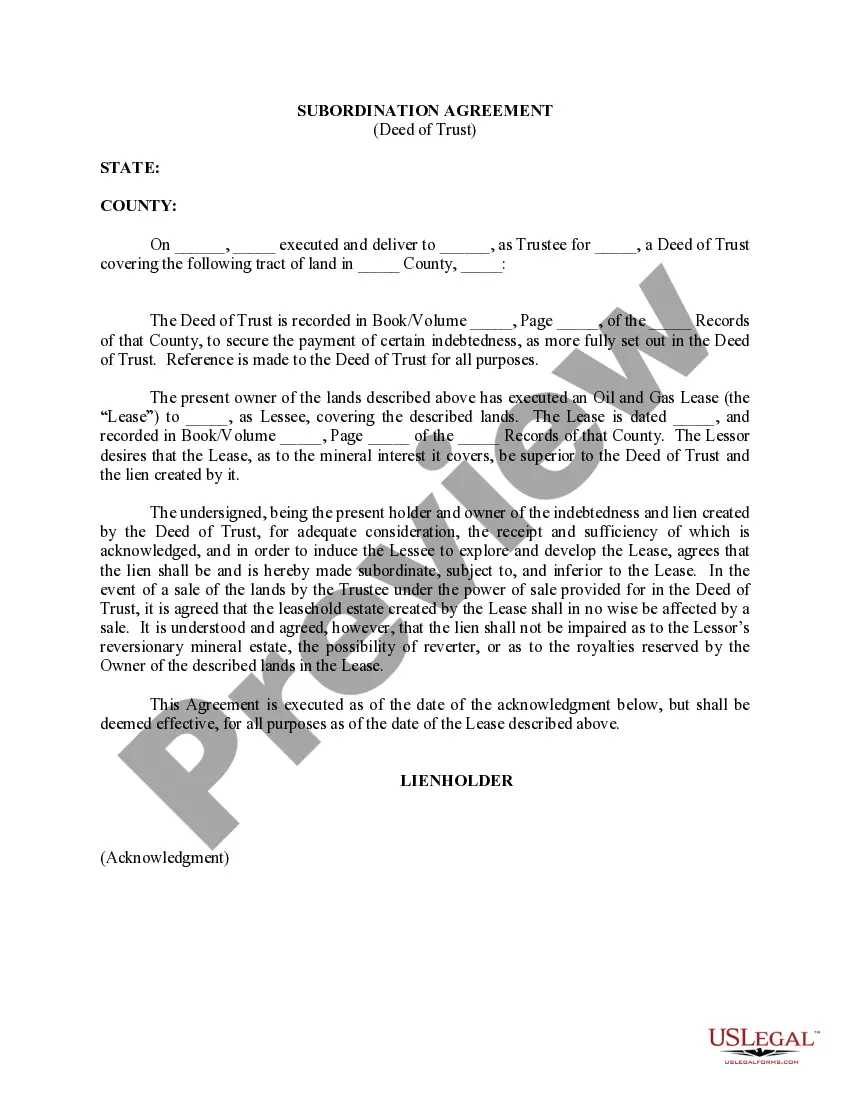

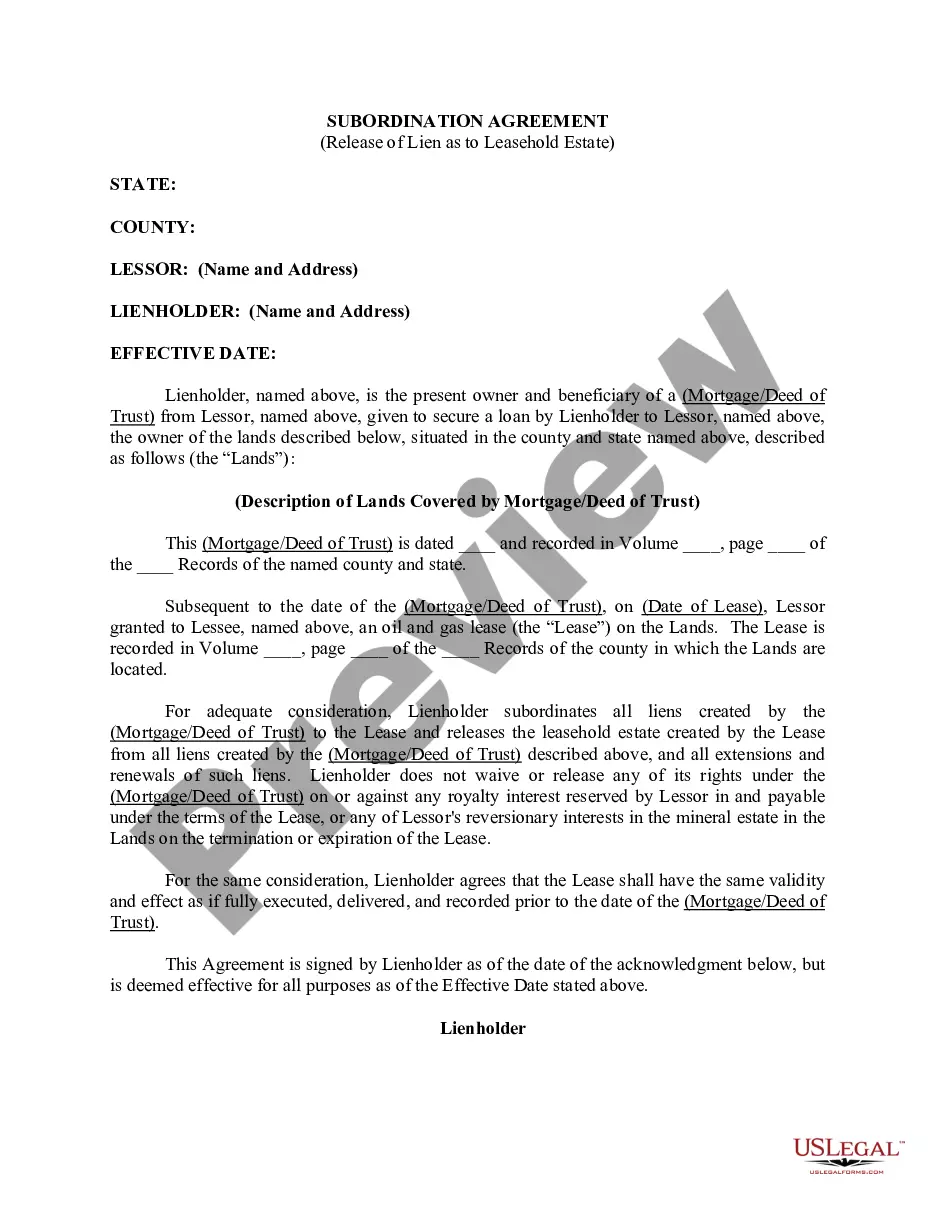

Security Interest Subordination Agreement

What this document covers

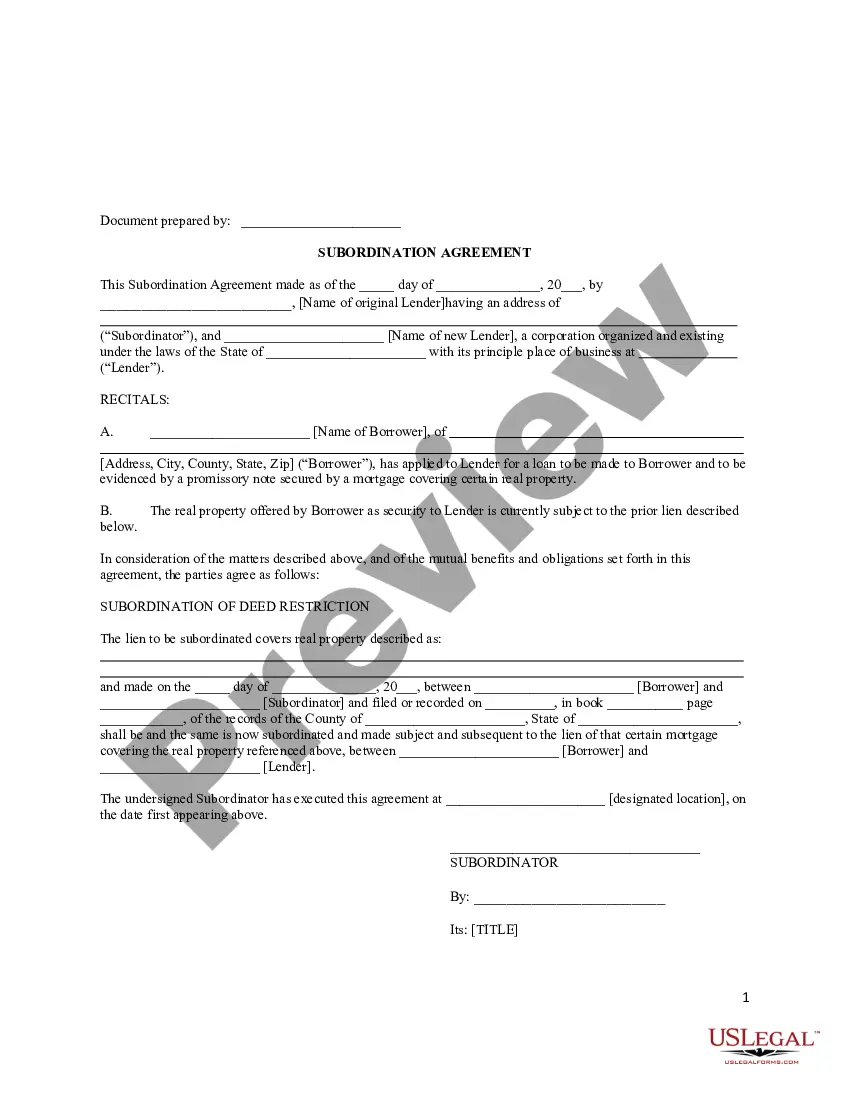

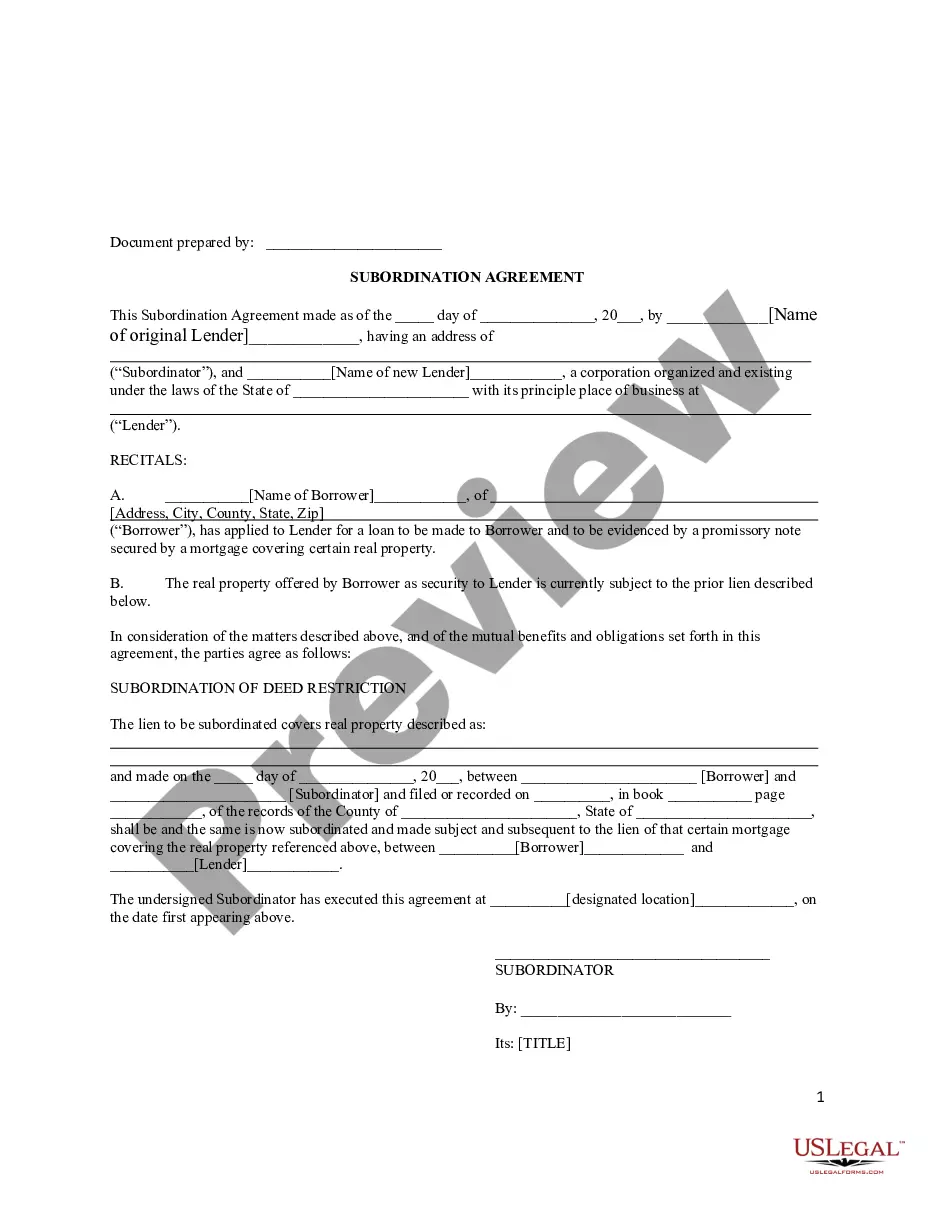

The Security Interest Subordination Agreement is a legal document that establishes the priority of claims on collateral between creditors. This agreement is necessary when a creditor agrees to subordinate their security interests to those of another lender, usually to facilitate a loan or credit extension. It differs from other security agreements in that it specifically addresses the ranking of claims on the same collateral.

Key components of this form

- Date of the agreement and identified parties involved.

- Definition of collateral that secures the loans.

- Clause for the creditor's subordination of their rights to the bank.

- Provisions regarding the modification of senior debt by the bank.

- Default conditions and remedies available to the bank.

- Governing law and jurisdiction for enforcement of the agreement.

Common use cases

This agreement is used when a debtor seeks to secure financing from a bank, but there is an existing creditor with a claim on the same collateral. It allows the bank to have a superior claim, encouraging them to provide the loan by ensuring their financial interest is prioritized in case of default.

Who should use this form

- Creditors who are willing to subordinate their security interests.

- Debtors seeking additional financing while having existing secured debts.

- Banks or financial institutions extending credit in exchange for secured collateral.

Completing this form step by step

- Identify the date the agreement is being signed.

- Clearly state the names and addresses of all parties involved: the creditor, debtor, and bank.

- Detail the collateral being subordinated in Exhibit A.

- Include signatures and printed names of the creditor and debtor.

- Ensure the agreement is governed by the correct state law indicated in the form.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, verifying state requirements is recommended to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to accurately specify the collateral in Exhibit A.

- Not obtaining all necessary signatures before finalizing the document.

- Overlooking the governing law clause, which may differ by state.

Benefits of completing this form online

- Instant access to a professionally drafted agreement that saves time and legal costs.

- Editable fields that allow for easy customization based on specific needs.

- Secure storage and retrieval options for completed forms.

Legal use & context

- This agreement is enforceable in a court of law, provided it is executed correctly.

- Subordination agreements serve to clarify the order of claims in insolvency proceedings.

- Any alterations to the terms must be documented in writing and signed by all parties.

Main things to remember

- The Security Interest Subordination Agreement prioritizes the bankâs claims over those of other creditors.

- Proper execution and customization are essential for legal validity.

- Understanding the implications and benefits of this agreement can enhance financial negotiations.

Looking for another form?

Form popularity

FAQ

When a Borrower wishes to refinance the property, they must request a subordination request to the Lender. The Lender will subordinate their loan only when there is no cash out as part of the refinance.

Subordination agreements are prepared by your lender. The process occurs internally if you only have one lender. When your mortgage and home equity line or loan have different lenders, both financial institutions work together to draft the necessary paperwork.

: placement in a lower class, rank, or position : the act or process of subordinating someone or something or the state of being subordinated As a prescriptive text, moreover, the Bible has been interpreted as justifying the subordination of women to men.

But as property values are going up and the demand for refinance isn't as much, it seems that the subordination process has gotten a little easier. Typically, it takes two to three weeks to get the resubordination paperwork through, and it is likely to set you back $200 to $300.

A subordination agreement is a legal document that establishes one debt as ranking behind another in priority for collecting repayment from a debtor. The priority of debts can become extremely important when a debtor defaults on payments or declares bankruptcy.

Resubordination is the process of keeping the first mortgage in first place, ahead of other mortgages. When you refinance your first mortgage, the lender will insist on resubordinating the home equity loan or line of credit. The equity lender isn't required to resubordinate.

Subordination is the process of ranking home loans (mortgage, HELOC or home equity loan) by order of importance.Through subordination, lenders assign a lien position to these loans. Generally, your mortgage is assigned the first lien position while your HELOC becomes the second lien.

Subordination is the process of ranking home loans (mortgage, HELOC or home equity loan) by order of importance.Through subordination, lenders assign a lien position to these loans. Generally, your mortgage is assigned the first lien position while your HELOC becomes the second lien.

Unless there is a subordination agreement, it is virtually impossible to refinance your first mortgage. The document agreeing to the subordination must be signed by the lender and the borrower and requires notarization.