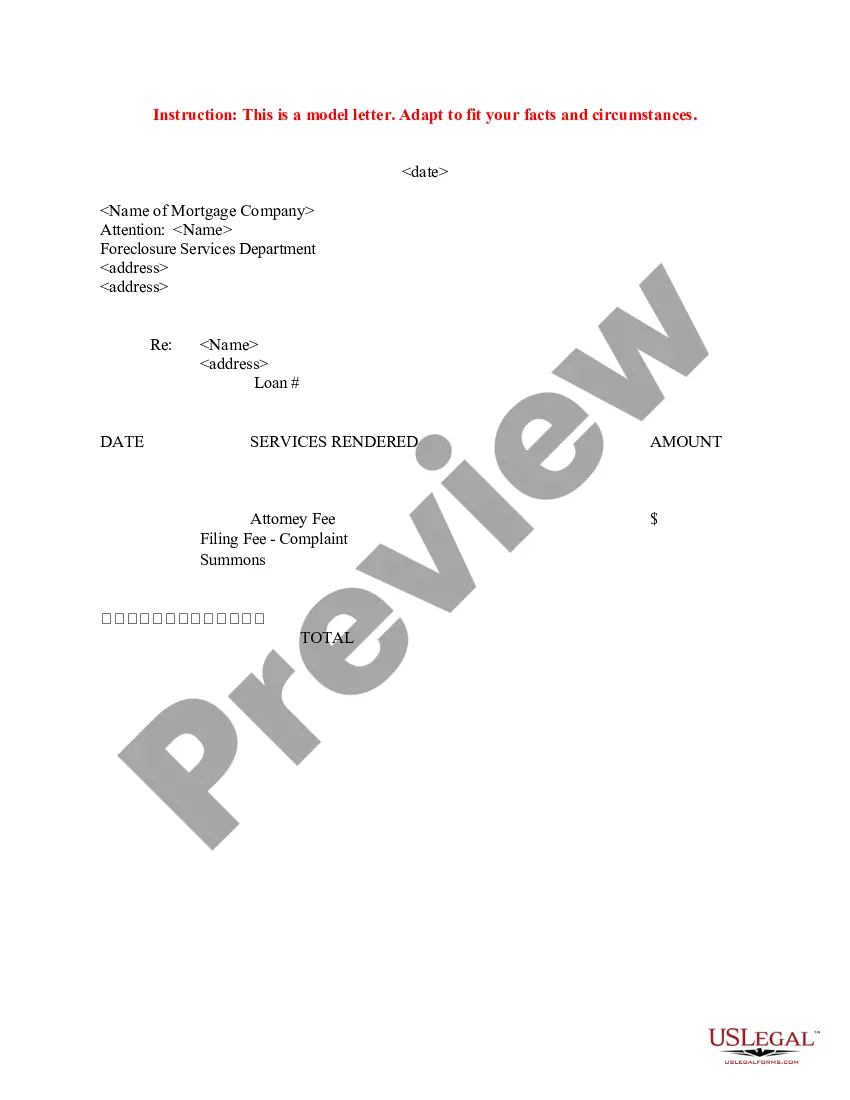

Sample Letter to Foreclosure Attorney - Payment Dispute

Overview of this form

The Sample Letter to Foreclosure Attorney - Payment Dispute is a template designed to assist individuals in addressing payment disputes with foreclosure attorneys. This form provides a structured way to formally request an itemization of payments and clarify any discrepancies in your account. Unlike other forms related to foreclosure, this letter specifically focuses on disputes regarding payments made, ensuring effective communication with your attorney.

Key components of this form

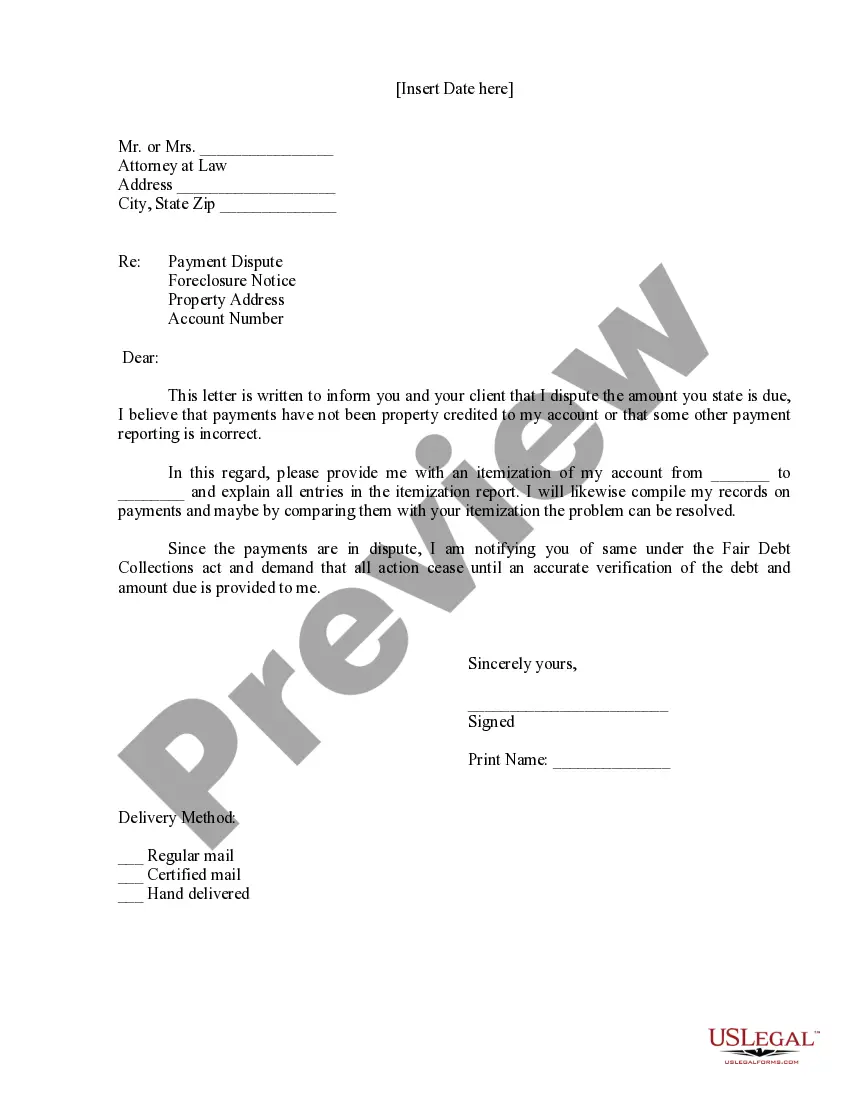

- Date of the letter

- Recipient's name and address (Attorney at Law)

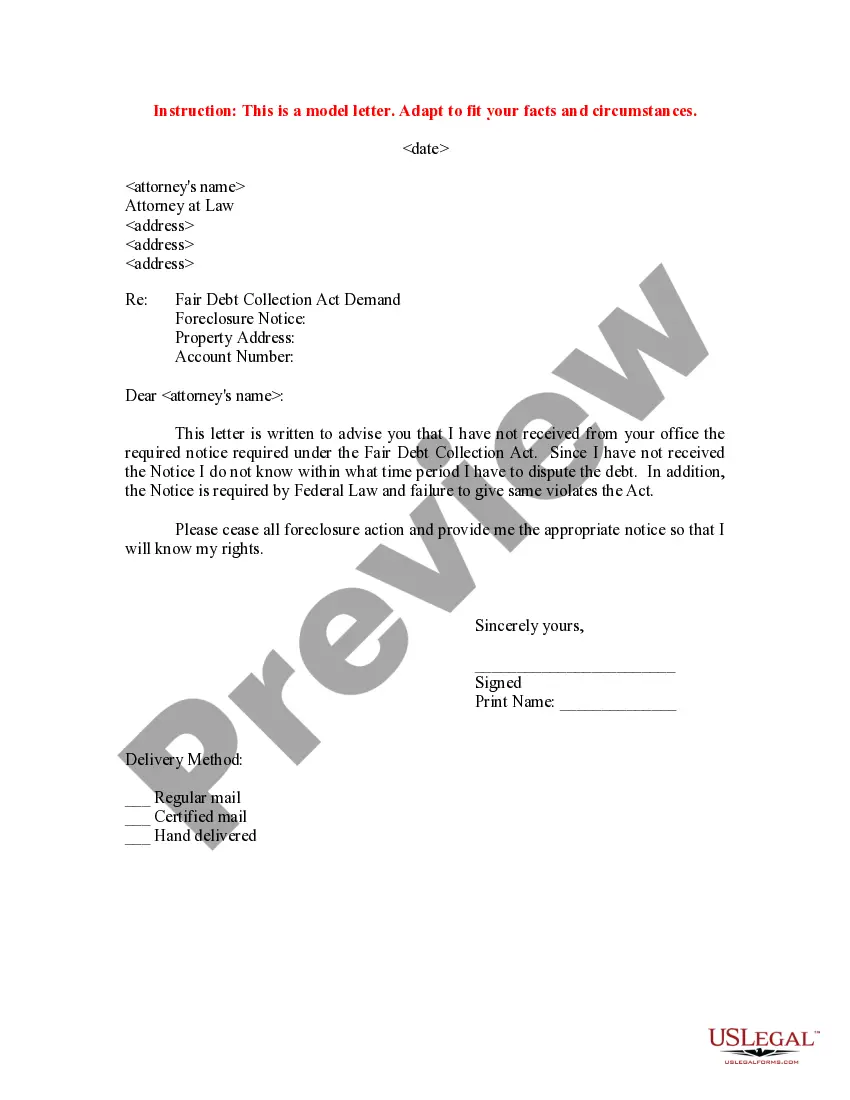

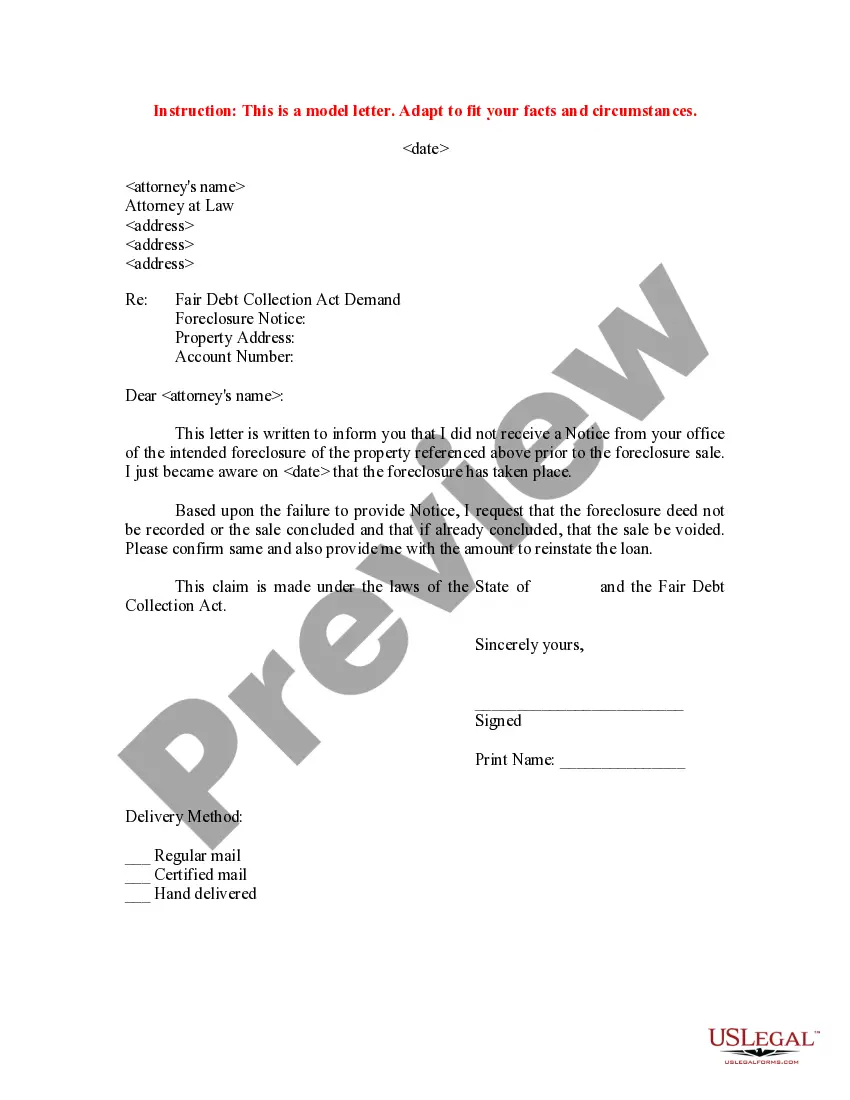

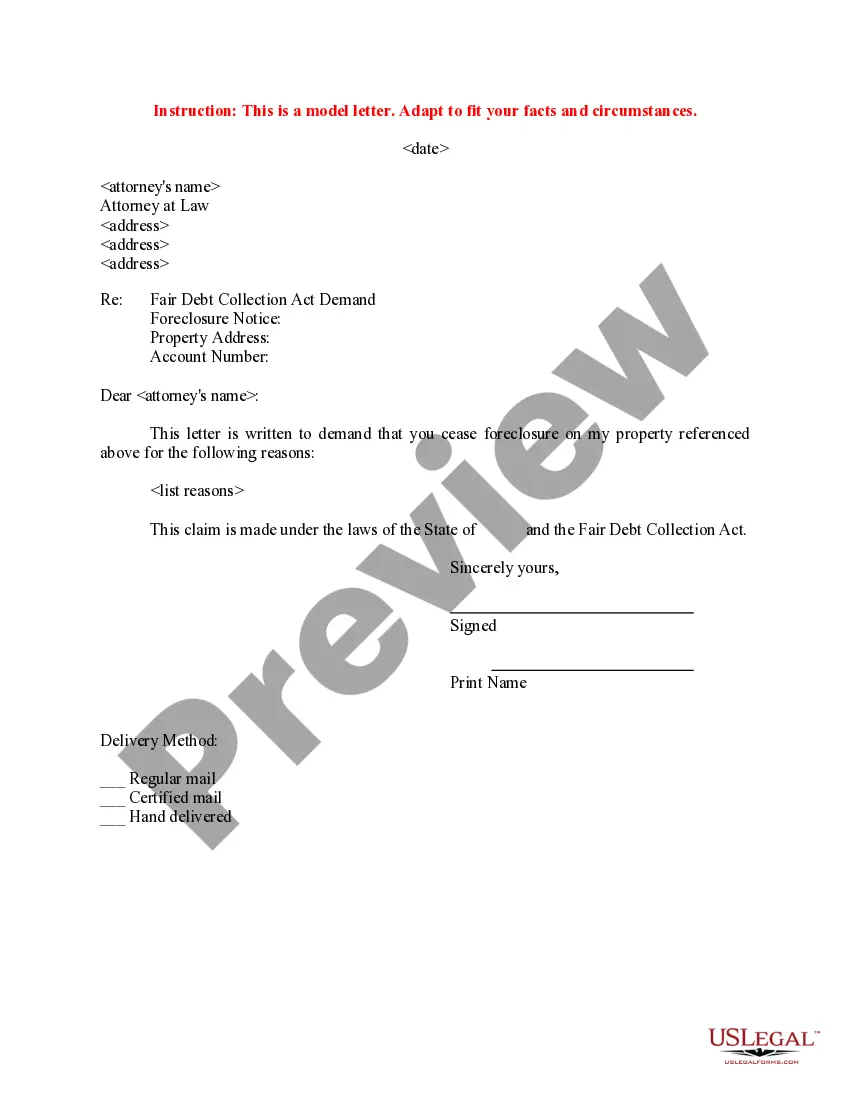

- Subject line referencing the Fair Debt Collection Act

- Request for an itemization of payments

- Space for signature and printed name

- Delivery method selection options

Common use cases

This form should be used whenever a property owner believes there is an error in their payment history regarding a foreclosure situation. It is particularly useful when you need clarification on the payments made to your attorney or when you're seeking documentation to support your case before proceeding further in a foreclosure process.

Who this form is for

- Homeowners facing foreclosure who have questions about payment records

- Individuals receiving communications from foreclosure attorneys

- Anyone who wants to ensure accurate record-keeping of payments made

Instructions for completing this form

- Enter the date of writing the letter.

- Fill in the attorney's name and complete address.

- Specify the date range for which you are requesting an itemization of your payments.

- Sign the letter and print your name for identification.

- Select your preferred delivery method (regular mail, certified mail, hand delivery).

Notarization guidance

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include the correct date range for the payment itemization.

- Not providing sufficient detail in the request for clarification.

- Ineffectively specifying the attorney's contact information.

- Not signing the letter before sending.

Why complete this form online

- Easy access to a professionally drafted letter template.

- Time-saving downloadable format for immediate use.

- Edit and customize the letter to fit your specific situation.

- Reliable and accurate, created by licensed attorneys.

Looking for another form?

Form popularity

FAQ

A hardship letter should Start by stating the purpose of the letter whether it is a loan modification or a short sale so the lender knows what homeowners want. It should say something like I need to restructure my mortgage and obtain a lower, fixed interest rate2026, in a way that force them to find out why.

Financial hardship typically refers to a situation in which a person cannot keep up with debt payments and bills or if the amount you need to pay each month is more than the amount you earn, due to a circumstance beyond your control.

Some of the most common types of hardship are: job loss, pay reduction, underemployment, declining business revenue, death of a coborrower, illness, injury, and divorce.

I am writing to dispute a billing error in the amount of $______ on my account. The amount is inaccurate because describe the problem. I am requesting that the error be corrected, that any finance and other charges related to the disputed amount be credited as well, and that I receive an accurate statement.

Tell the Story. Your letter should start with an introduction of who you are and what kind of loan you are applying for. Lead into your story with something like "We want to explain our foreclosure from six years ago." Then, launch right into the details that led you to lose your home.

Your name, address, phone number and account number. The type of debt resolution you're seeking. Your financial situation that has caused you to fall behind in your payments. A detailed budget and your plan for making payments (if you want to keep your home)

Hardship Examples. There are a variety of situations that may qualify as a hardship. Keep it original. Be honest. Keep it concise. Don't cast blame or shirk responsibility. Don't use jargon or fancy words. Keep your objectives in mind. Provide the creditor an action plan.