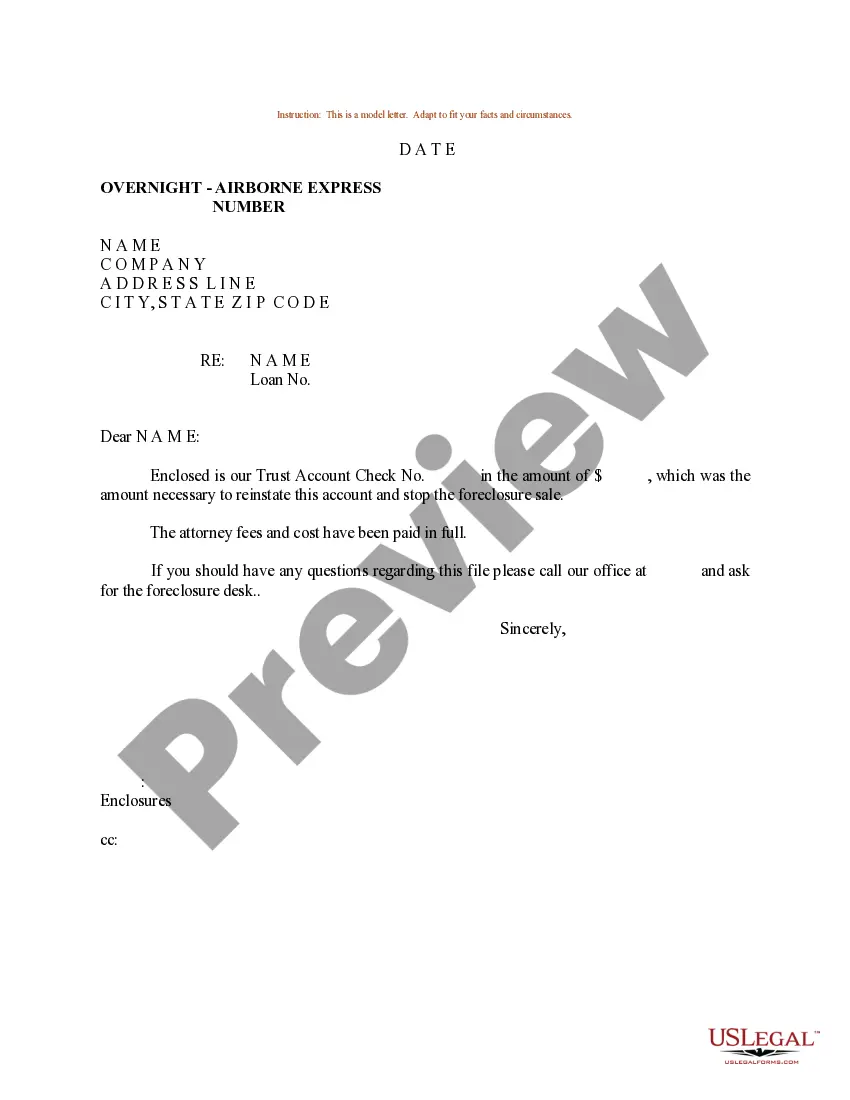

Sample Letter to Foreclosure Attorney - General Demand to Stop Foreclosure and Reasons

What this document covers

This form is a sample letter designed to communicate a formal demand to a foreclosure attorney. It aims to request the cessation of foreclosure proceedings by outlining specific reasons for the request. This document serves as a critical step for someone facing foreclosure, differentiating itself from other legal forms that may not directly address creditor communication or specific defenses under the Fair Debt Collection Act.

Key parts of this document

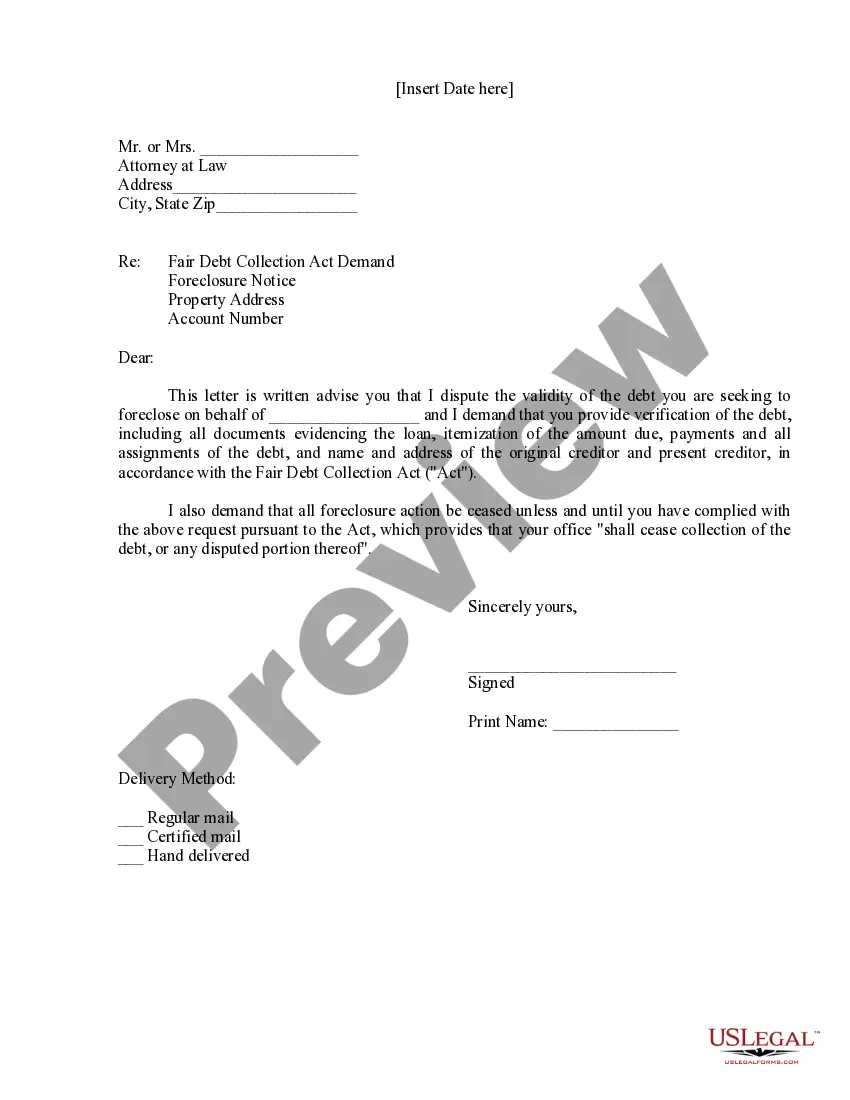

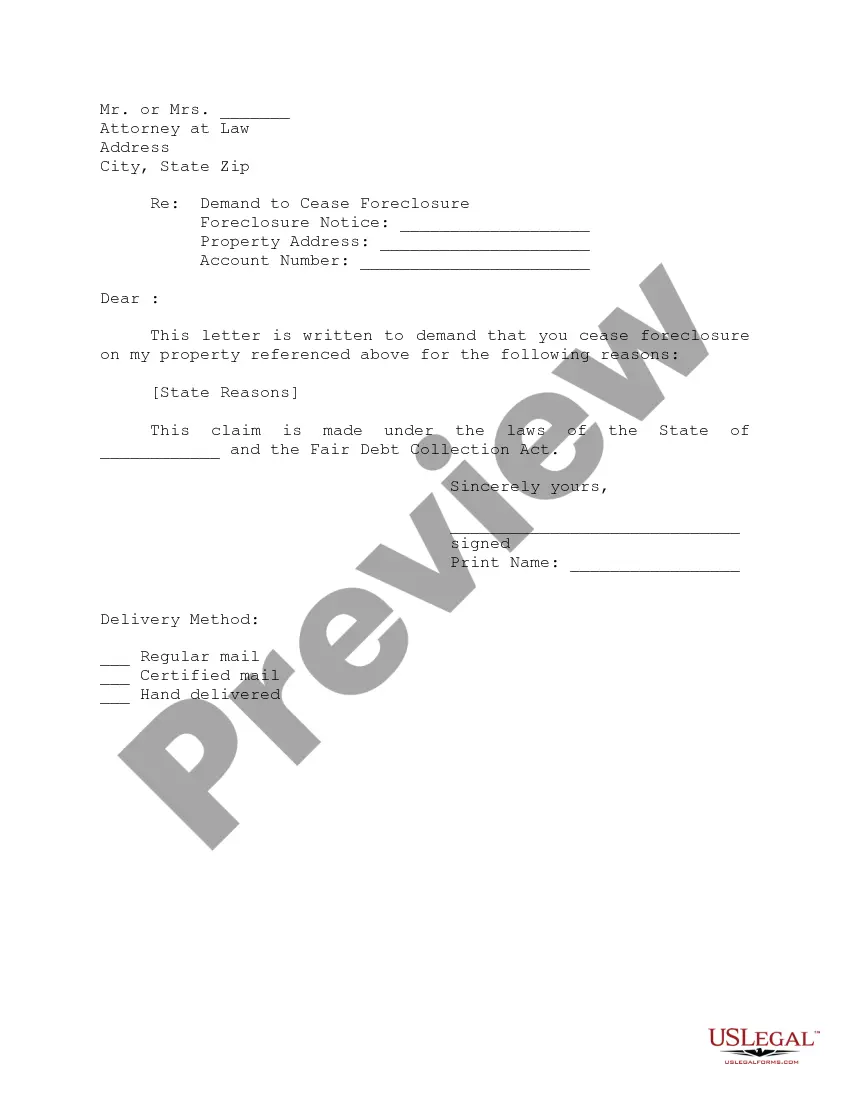

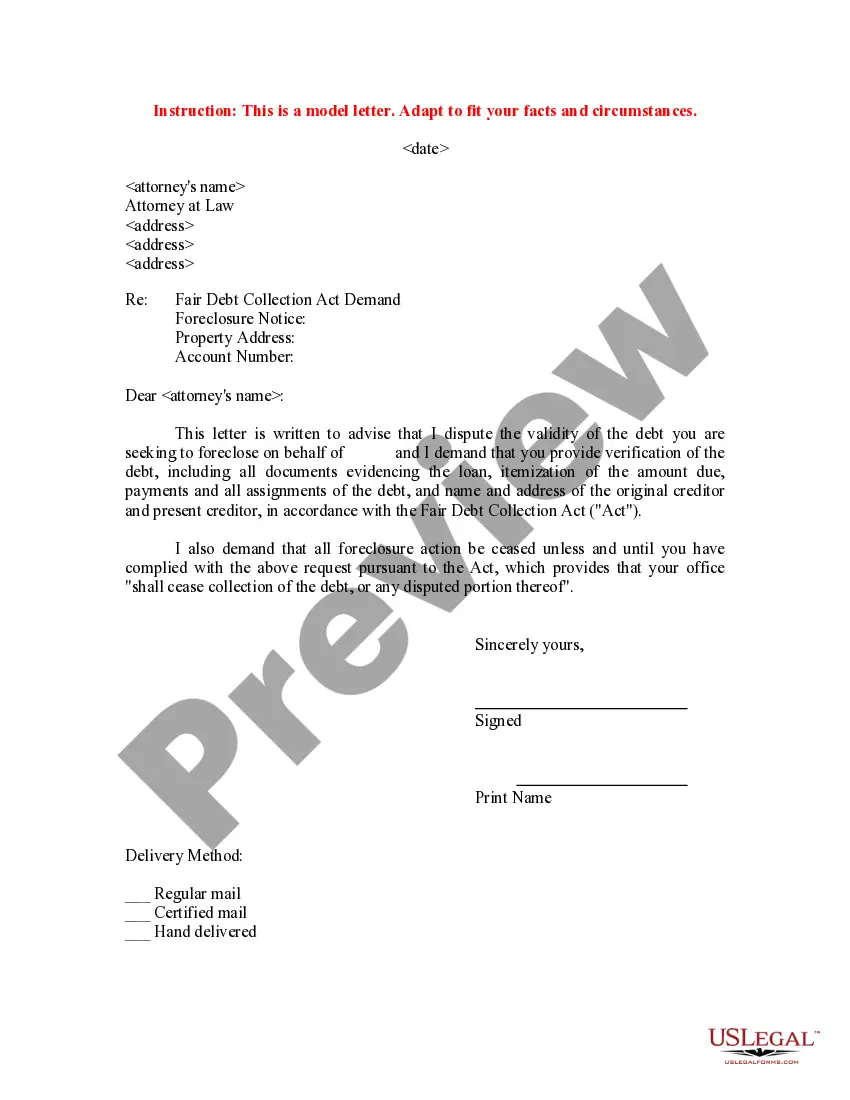

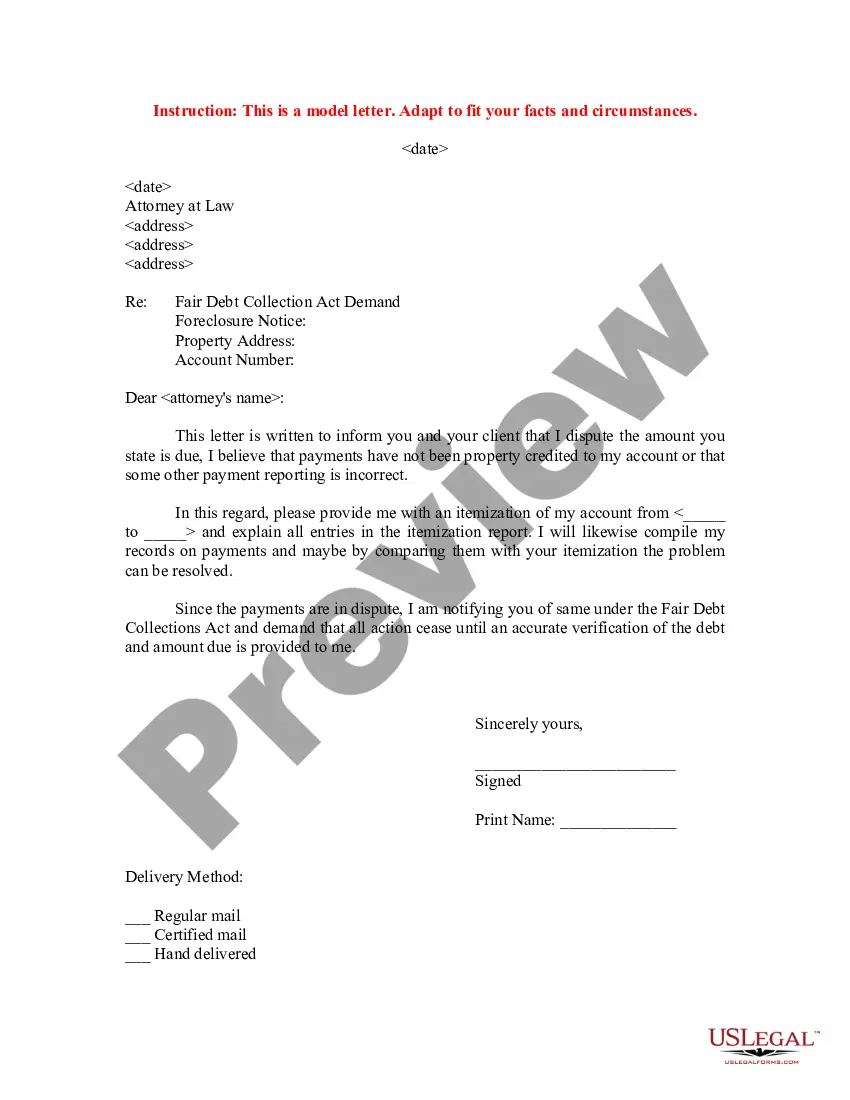

- Date of the letter.

- Attorney's name and firm details.

- Subject line referencing the Fair Debt Collection Act demand.

- A clear statement outlining the demand to stop foreclosure.

- Reasoning supporting the demand.

When this form is needed

This letter should be used by individuals who have received notice of foreclosure and wish to formally request that the foreclosure proceedings be halted. It can be particularly relevant in situations where a borrower believes that their rights under the Fair Debt Collection Act have not been upheld or when there are grounds for disputing the foreclosure process.

Intended users of this form

This form is intended for:

- Homeowners facing foreclosure.

- Individuals seeking to communicate formally with their foreclosure attorney.

- Borrowers who believe they have a legitimate reason to stop foreclosure proceedings.

How to prepare this document

- Insert the current date at the top of the letter.

- Fill in the attorney's name, firm, and address details.

- Include a subject line that clearly states the nature of the letter.

- Draft a clear demand to stop the foreclosure proceedings.

- Provide detailed reasons for your request, citing any relevant laws.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, signing this letter can introduce additional credibility when presenting your case to the attorney or court.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to address the letter to the correct attorney.

- Omitting important details regarding the reasons for the demand.

- Neglecting to proofread for clarity and grammatical errors.

Benefits of using this form online

- Convenient access to a professionally drafted template.

- Editability to customize your specific situation easily.

- Rapid download and print options for immediate use.

Legal use & context

- This form serves as an initial step in challenging foreclosure proceedings.

- It may not guarantee the cessation of foreclosure but initiates formal communication.

- Rights under the Fair Debt Collection Act should be cited accurately to strengthen your position.

Looking for another form?

Form popularity

FAQ

If you're facing foreclosure, you might be able to stop the process by filing for bankruptcy, applying for a loan modification, or filing a lawsuit.You can potentially file for bankruptcy or file a lawsuit against the foreclosing party (the "bank") to possibly stop the foreclosure entirely, or at least delay it.

Gather your loan documents and set up a case file. Learn about your legal rights. Organize your financial information. Review your budget. Know your options. Call your servicer. Contact a HUD-approved housing counselor.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

File for Bankruptcy. Modify your loan. Get a Deed in Lieu of Foreclosure. File a Lawsuit. Sell Your House Quickly.

Bringing the loan current means that you pay the total amount past due. You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees.Unfortunately, this option isn't viable for most people, because most people don't have the money to bring their loan current.

You can bring your loan current and stave off the foreclosure sale filing by paying the past due amount, plus penalties.You typically have to reinstate at least five days before the lender's deadline or risk the lender rejecting your payment and proceeding with a sale.

A reinstatement is the simplest solution for a foreclosure, however it is often the most difficult. The homeowner simply requests the total amount owed to the mortgage company to date and pays it.

Phase 1: Payment Default. Phase 2: Notice of Default. Phase 3: Notice of Trustee's Sale. Phase 4: Trustee's Sale. Phase 5: Real Estate Owned (REO) Phase 6: Eviction. The Bottom Line.