Acc. Errors and Past Due Notices

About this form

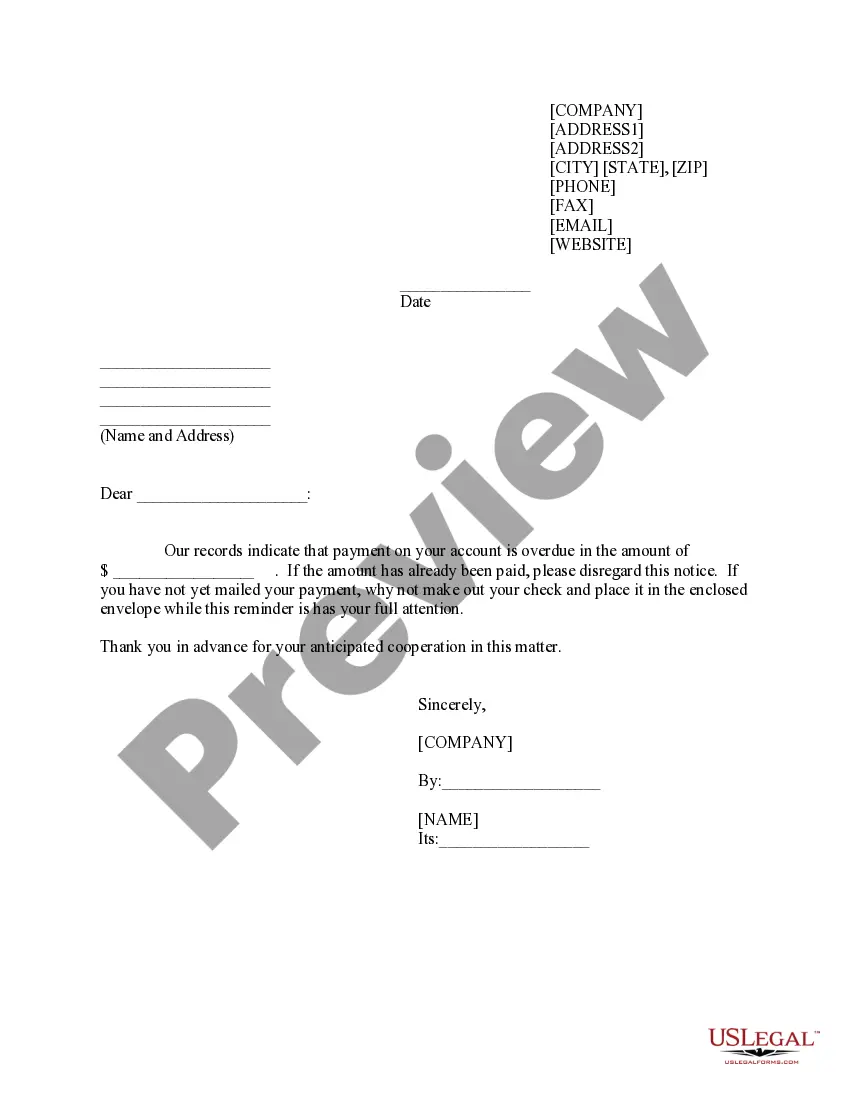

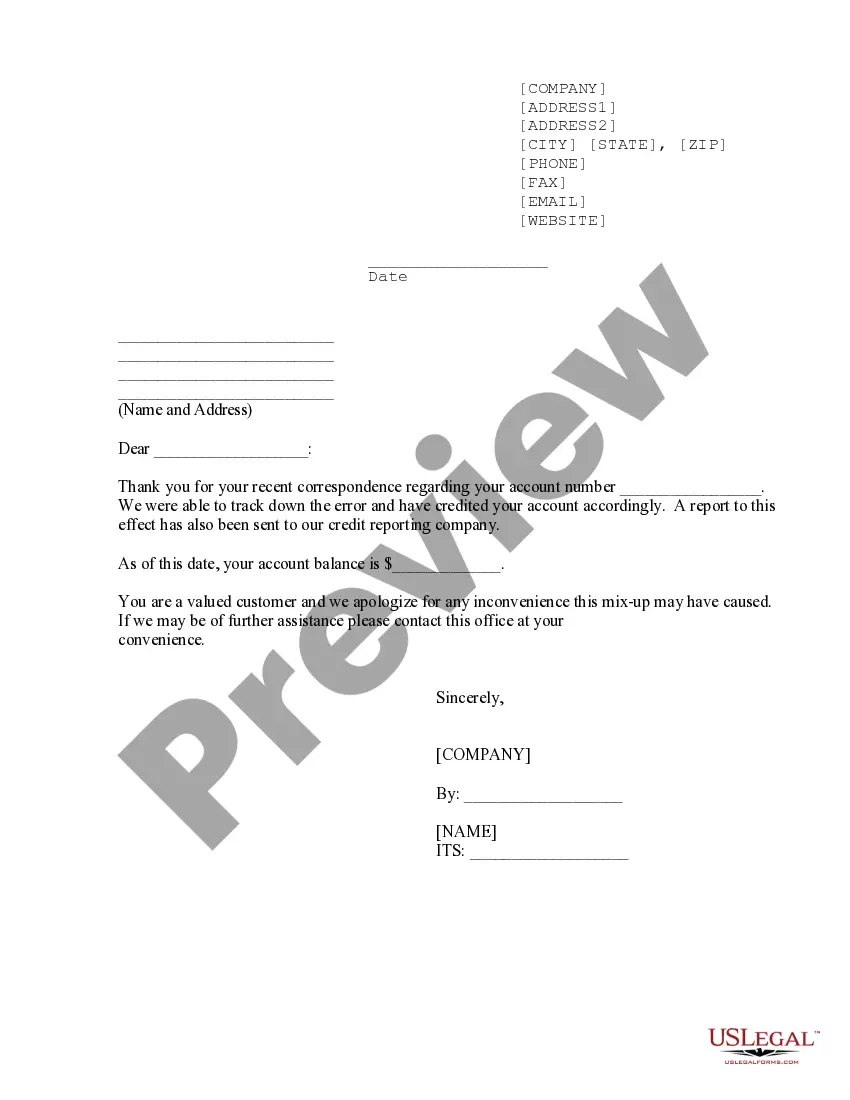

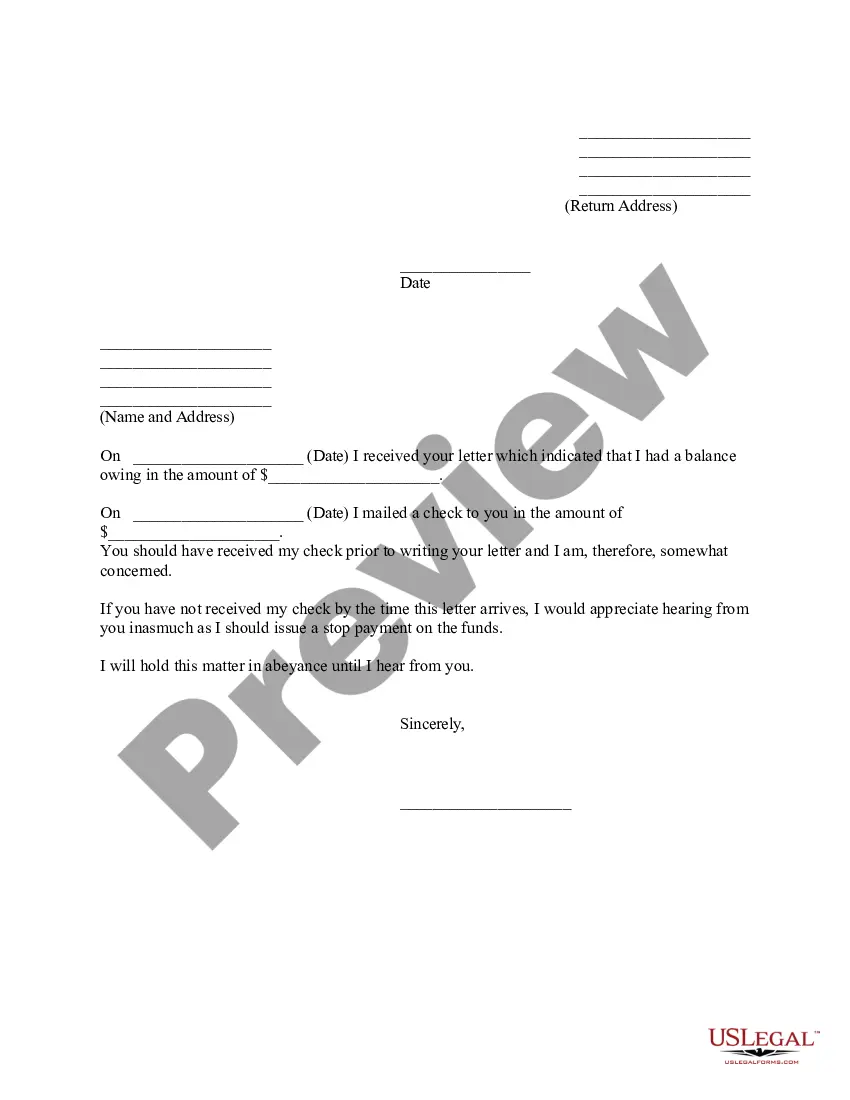

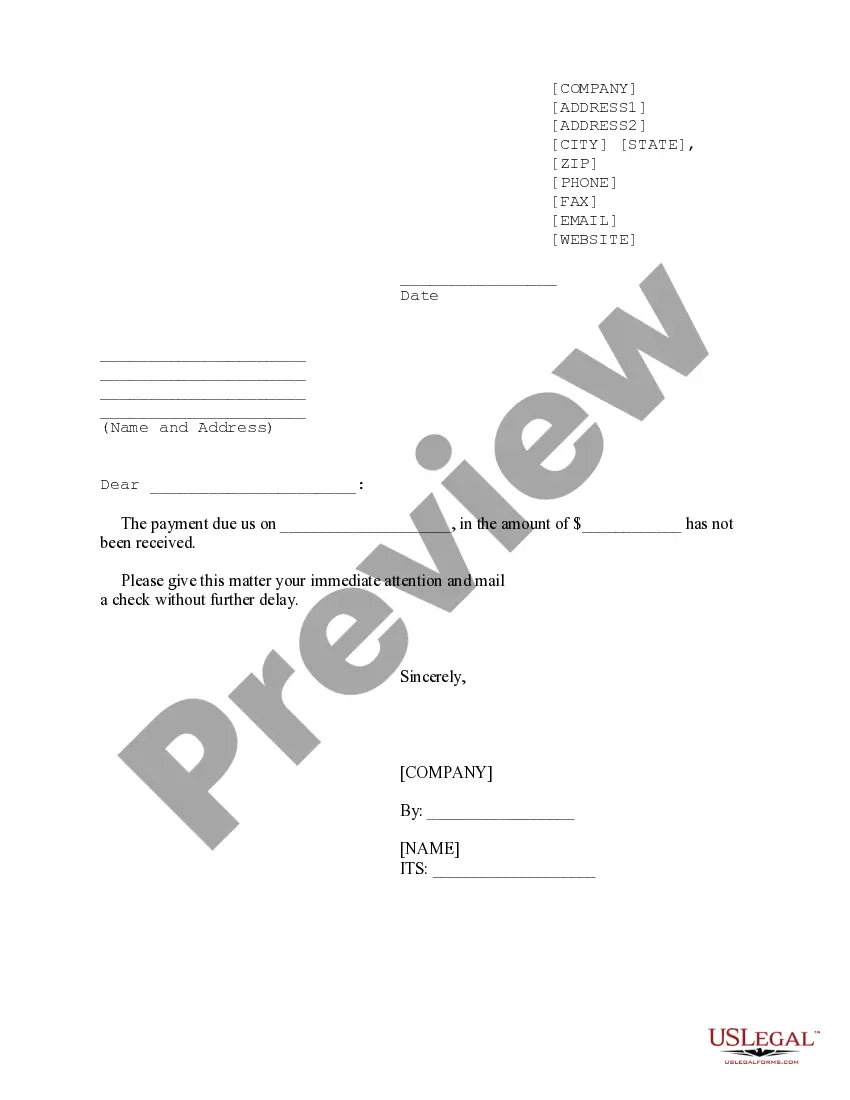

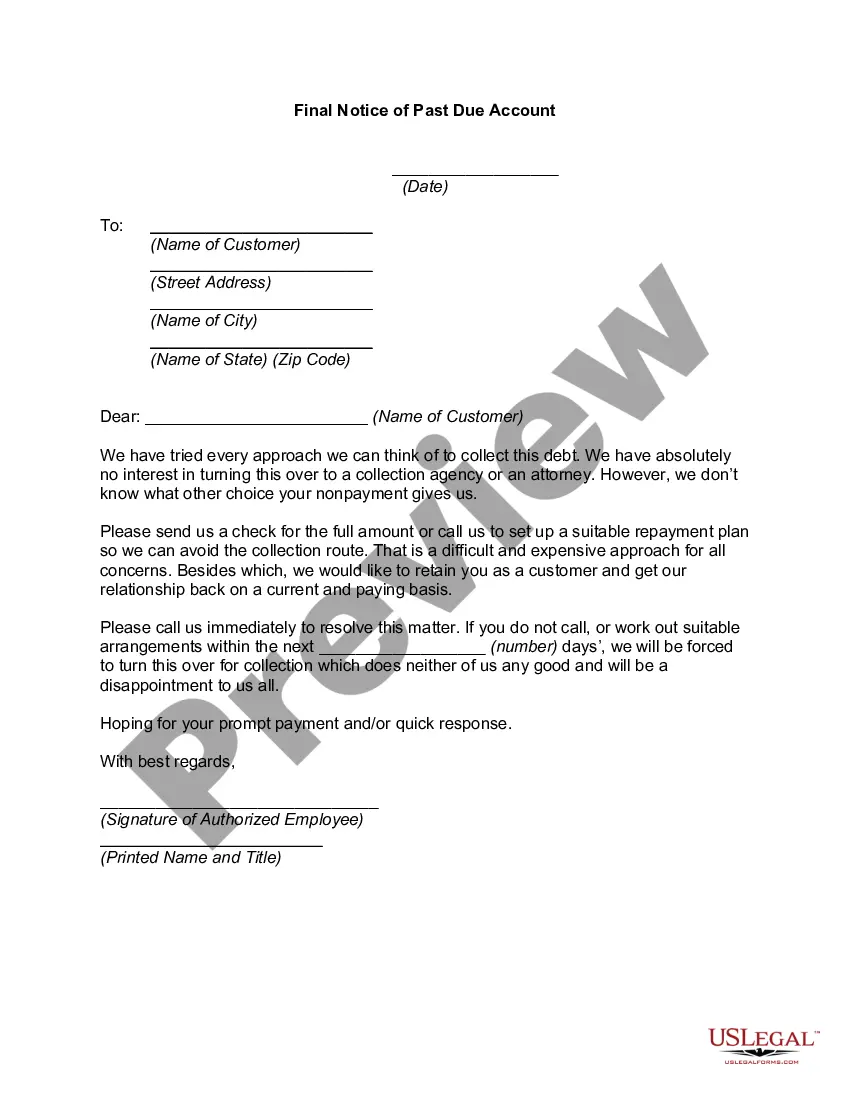

The Accumulated Errors and Past Due Notices form is a written communication used by businesses to address accounting mistakes that have led to incorrect billing or overdue payment notices. Unlike standard billing letters, this form specifically acknowledges errors in the accounting process, outlines the steps taken to rectify these mistakes, and re-establishes trust with the customer. It is crucial for maintaining good customer relationships and resolving payment discrepancies clearly and professionally.

Form components explained

- Header section containing the sender's address and contact information.

- Date field to indicate when the letter is being sent.

- Recipient's name and address to ensure correct delivery.

- A clear acknowledgment of the accounting error and an apology.

- Details about the nature of the error and measures taken to correct it.

- Assurance to the recipient that the problem will not recur.

- Signature line for the company representative.

When to use this form

This form should be used when a business mistakenly sends past due notices to a customer due to an accounting error. It is appropriate in situations where payments have been received but not correctly recorded, leading to unnecessary confusion and potential customer dissatisfaction. Using this form helps clarify the situation and maintain a positive business relationship.

Intended users of this form

- Businesses and organizations that manage accounts payable and receivable.

- Accounting departments that need to notify clients of billing errors.

- Customer service teams looking to manage client relations effectively.

- Any company aiming to provide quality service and resolve disputes amicably.

Steps to complete this form

- Fill out the sender's address and contact information at the top of the form.

- Enter the date the letter is being sent.

- Include the recipient's name and address accurately.

- Personalize the letter by addressing the recipient directly and explaining the accounting error.

- Sign the letter on behalf of the company, indicating the representative's name and title.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately identify the error leading to billing discrepancies.

- Not personalizing the letter for the specific customer.

- Omitting important contact information that could facilitate communication.

- Using unclear language that may confuse the recipient.

Why complete this form online

- Convenience of accessibility and quick downloads directly from your device.

- Easy to edit and customize to fit your specific business scenario.

- Reliable format provided by licensed attorneys ensures legal compliance.

Looking for another form?

Form popularity

FAQ

The normal method to handle immaterial discrepancies is to create a suspense account on the balance sheet or net out the minor amount on the income statement as "other."

The best way to handle a discrepancy is to take the time to research it and determine exactly what it is, what account it's for, and the best way to reconcile it. This is what is commonly referred to as adjustments and reclassifications.

An error of omission happens when you forget to enter a transaction in the books. You may forget to enter an invoice you've paid or the sale of a service. For example, a copywriter buys a new business laptop but forgets to enter the purchase in the books.

Reasons Behind Bookkeeping Discrepancies Error of Omission ? A financial transaction that is not recorded or is completely omitted. Error of Original Entry ? Recording of the wrong amount for a transaction. Error of Duplication ? Recording of the same transaction more than once.

We're writing to inform you that your account is now 30 days past due. The amount of $xx was due on insert date. We sent you a past due notice on insert date and did not receive a reply. This matter requires your urgent attention.

A restatement is the revision of a company's financial statements to correct an error.

A discrepancy is an accounting error that was not caused intentionally. An accounting error can include discrepancies in dollar figures, or might be an error in using accounting policy incorrectly (i.e., a compliance error).

The best way to correct errors in accounting is to add a correcting entry. A correcting entry is a journal entry used to correct a previous mistake. The type of correcting entry depends on: GAAP (generally accepted accounting practices) guidelines.