Miller Trust Forms for Medicaid

What this document covers

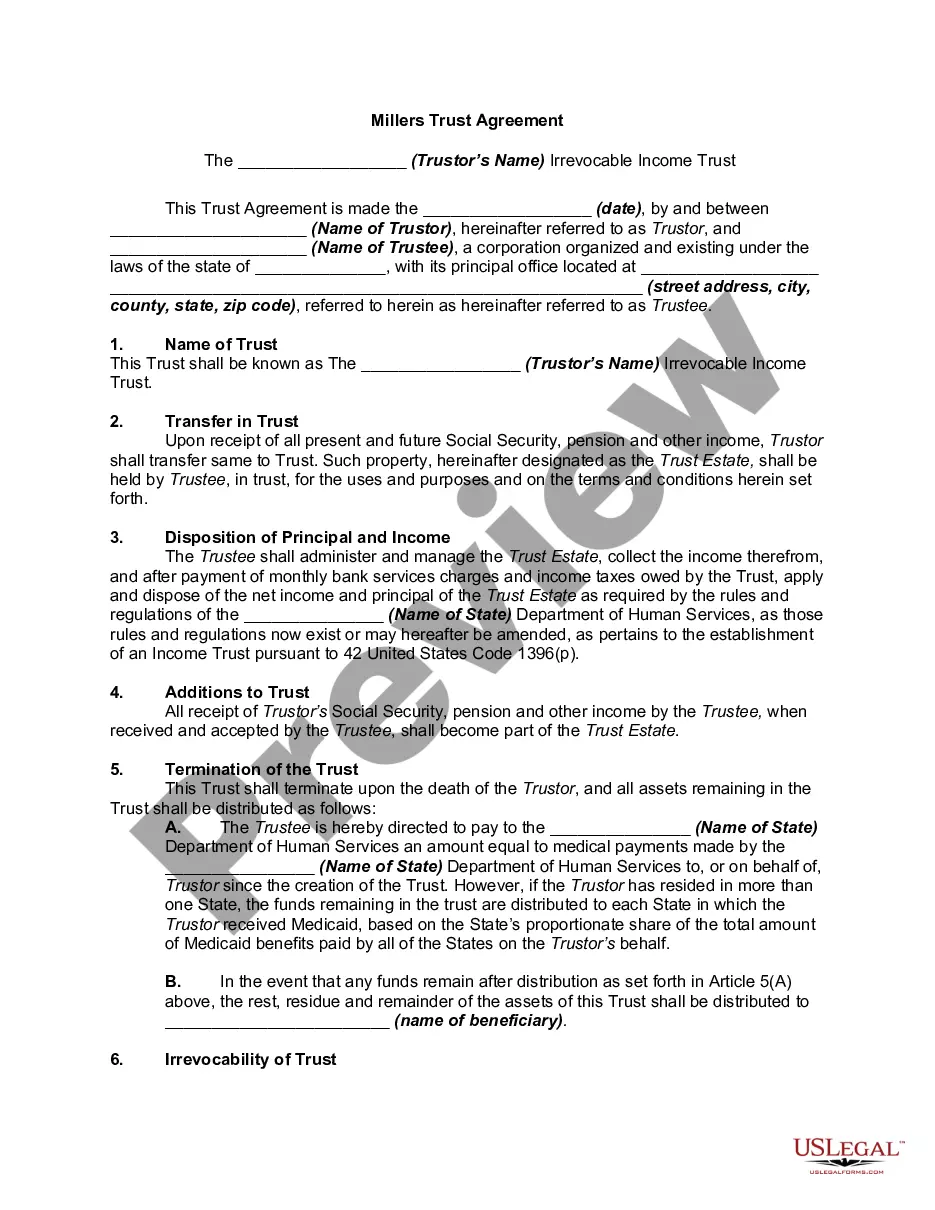

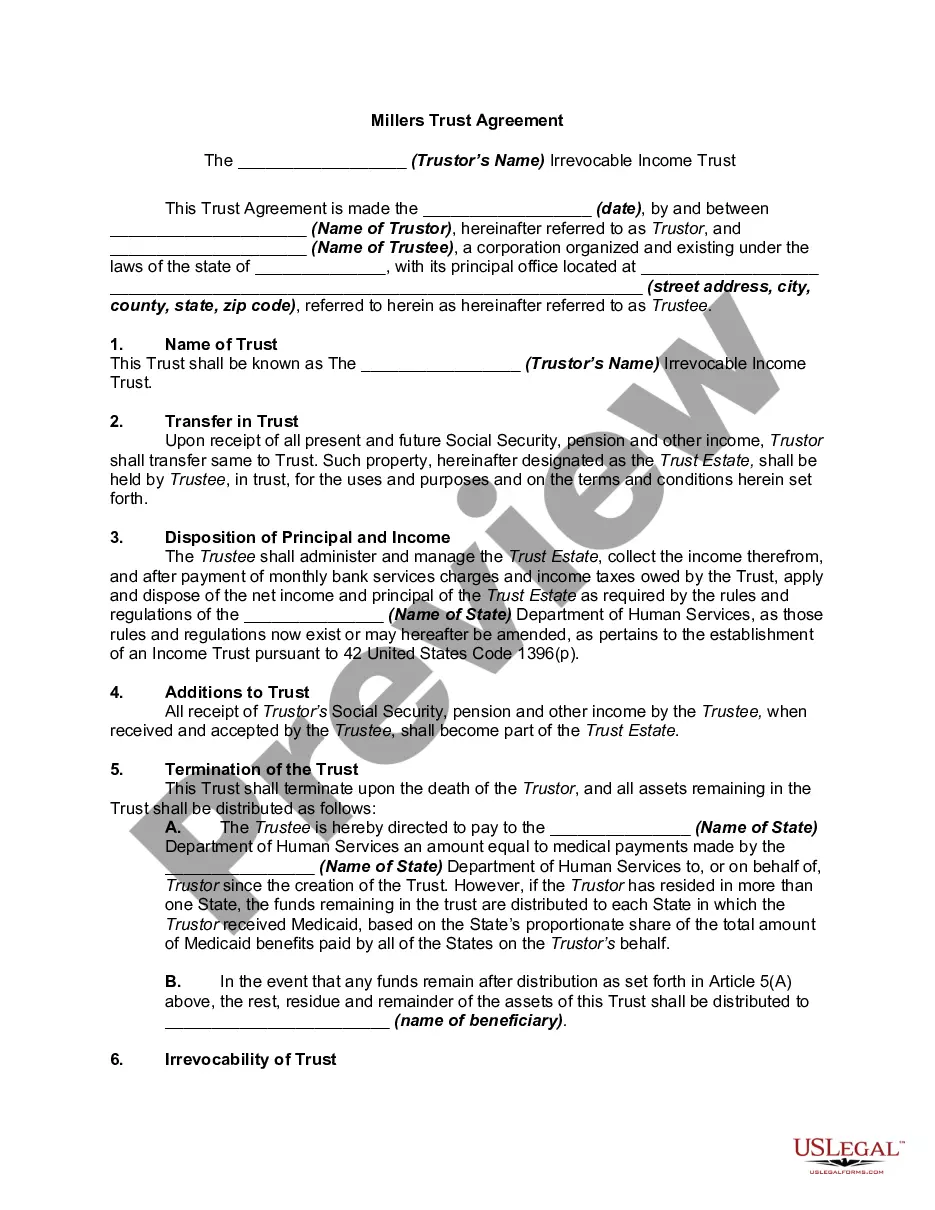

The Miller Trust Forms for Medicaid are legal documents that create an irrevocable income trust designed to help individuals in qualifying for Medicaid benefits while protecting their income and assets. This form facilitates the transfer of income into a trust, making it possible to meet Medicaid's financial requirements, which can be crucial for individuals needing long-term care without liquidating their assets. It distinguishes itself from other trust forms by being specifically tailored for Medicaid planning under 42 U.S.C. 1396(p).

Key parts of this document

- Name of Trust: Identifies the trust created by the Trustor.

- Transfer in Trust: Describes how income is transferred into the trust.

- Disposition of Principal and Income: Outlines how the trust's assets will be managed and distributed upon the Trustor's death.

- Irrevocability of Trust: States that the trust cannot be amended or terminated without specific agreements.

- Powers of Trustee: Defines the authority given to the trustee over the trust assets.

- Accounting: Details the trustee's obligations regarding record-keeping and reporting to the Trustor and state authorities.

When to use this form

This form should be used when an individual needs to establish a Miller Trust to qualify for Medicaid benefits. Situations may include cases where the Trustor receives income that exceeds Medicaid's allowable limits. By diverting this income into the trust, the Trustor can meet eligibility requirements for benefits that cover long-term healthcare without losing needed assets.

Who this form is for

- Individuals seeking Medicaid benefits who have income exceeding state limits.

- Individuals looking to protect their assets while still qualifying for necessary healthcare services.

- Family members or caregivers of individuals who need long-term care support.

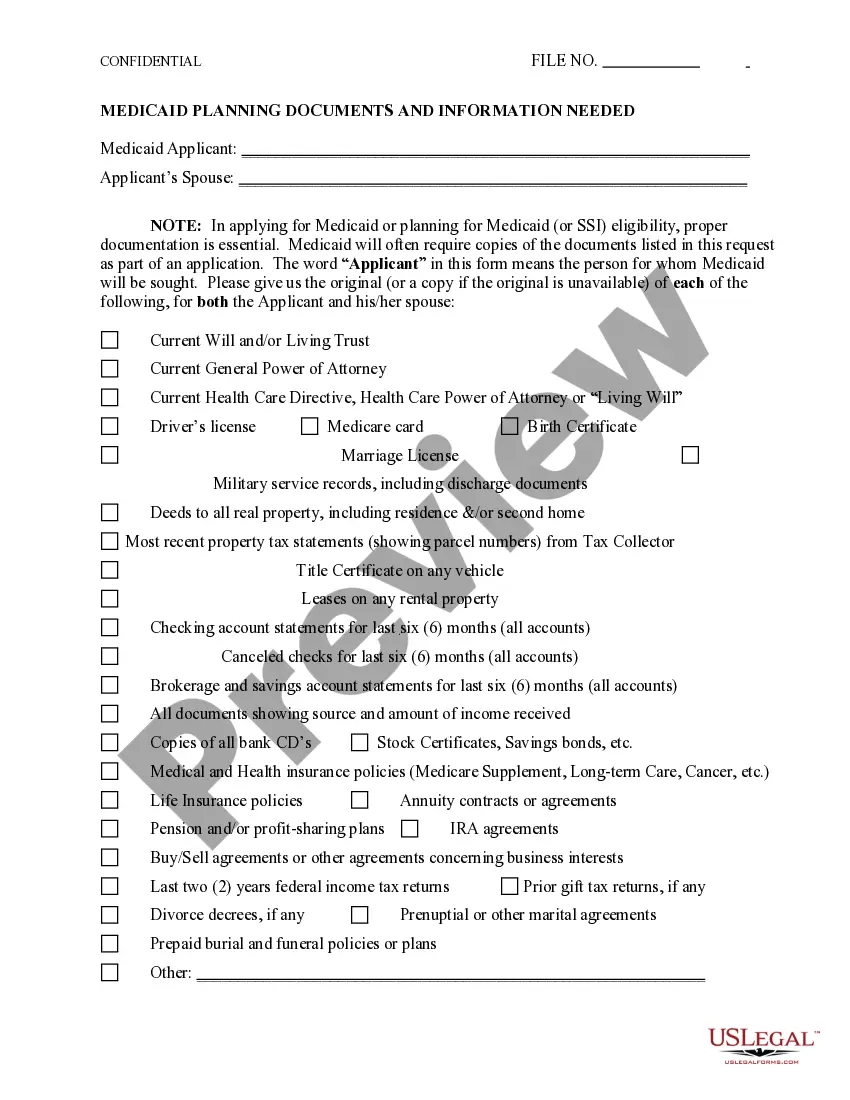

Instructions for completing this form

- Identify the parties: Clearly state the names of the Trustor and Trustee.

- Specify the property: Outline the income and assets being transferred into the trust.

- Enter dates and signatures: Provide the date of creation and make sure all parties sign the document.

- Detail the disposition: Specify how remaining assets will be handled after the Trustor's death and according to state law.

- Complete the accounting provisions: Ensure record-keeping requirements align with state regulations.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, check your state's requirements to confirm if notarization is necessary for legal validity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to correctly identify all parties involved, leading to legal issues later.

- Not transferring the correct income or assets, which can invalidate the trust's intent.

- Neglecting to signature requirements, including both the Trustor and Trustee.

Benefits of completing this form online

- Convenience: Download the form anytime from anywhere, making it easy to start your Medicaid planning.

- Editability: Fill in your details directly online before printing.

- Reliability: All forms are drafted by licensed attorneys, ensuring legal compliance.

Looking for another form?

Form popularity

FAQ

Miller trusts can be used to pay for a small monthly allowance, Medicare premiums and medical expenses that are not covered by Medicaid or Medicare.If there are any remaining funds after the state takes its allowed portion, these funds can go to the beneficiaries that are named in the trust.

In order to establish a Miller Trust, a bank account must be set up and a trust document drawn up. The person setting up the Income Diversion Trust (the grantor, also called a settlor) can be the Medicaid applicant, his/her guardian or power of attorney.

Some Medicaid professionals include the cost of establishing this type of trust as a package deal with other Medicaid planning services. However, on average, solely setting up a QIT runs approximately $400 to $500, but may run as high as $1,000 or $2,000.

Establishing the Miller Trust Bank Account National Bank of Arizona is exceptionally cooperative in establishing these trusts. Once the bank account is opened in the name of the trust, the next step is to write social security and the pension payers and ask them to direct deposit future checks into the bank account.

The Miller trust can pay the Medicaid recipient a small personal needs allowance, and the trust can also be used to pay the recipient's spouse a monthly allowance.If there is any money left in the trust when the recipient dies, Medicaid has a right to the money to recover the cost of care.

Sometimes referred to as Qualifying Income Trusts, Qualified Income Trusts, or Miller Trusts (based upon a court case with the same name), they are used when a Medicaid applicant has too much income to qualify for Medicaid but not enough to pay for nursing home care or other long-term care costs.

Payments. Miller trusts can be used to pay for a small monthly allowance, Medicare premiums and medical expenses that are not covered by Medicaid or Medicare.If there are any remaining funds after the state takes its allowed portion, these funds can go to the beneficiaries that are named in the trust.

A Miller trust does not use an EIN.)Note: Miller Trusts are treated as grantor trusts under IRC § 671. Page 2. 4) The individual establishing the trust must have a Power of Attorney or legal guardianship to act on behalf of the member.