Miller Trust Forms for Assisted Living

About this form

The Miller Trust Forms for Assisted Living is a legal document that establishes an irrevocable income trust, which is specifically designed to manage assets for individuals receiving Medicaid benefits. This form allows the trustor to transfer income, such as Social Security and pensions, into the trust while ensuring that these funds are utilized according to legal guidelines for assisted living arrangements. Unlike other types of trusts, this form specifically adheres to Medicaid requirements enabling beneficiaries to qualify for necessary medical assistance.

What’s included in this form

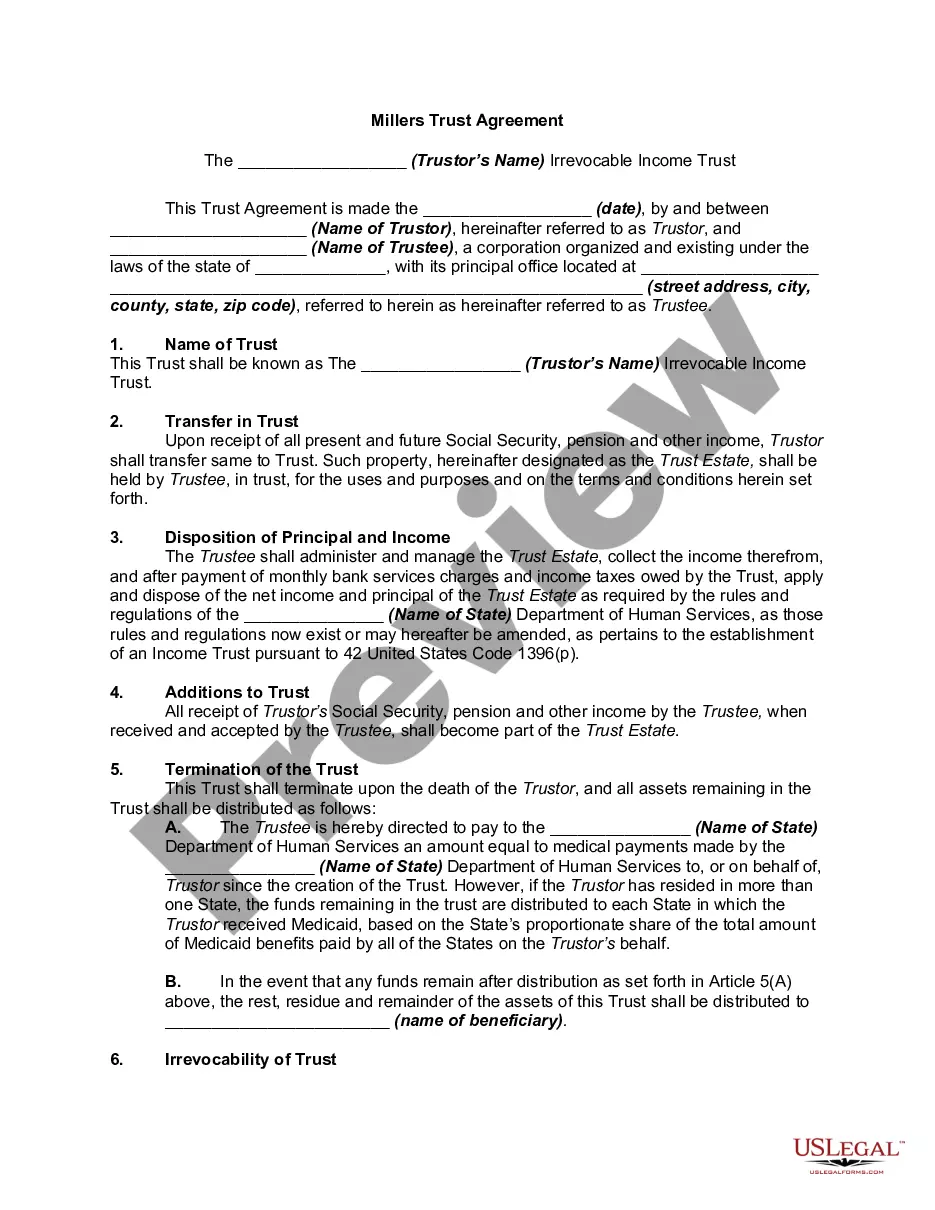

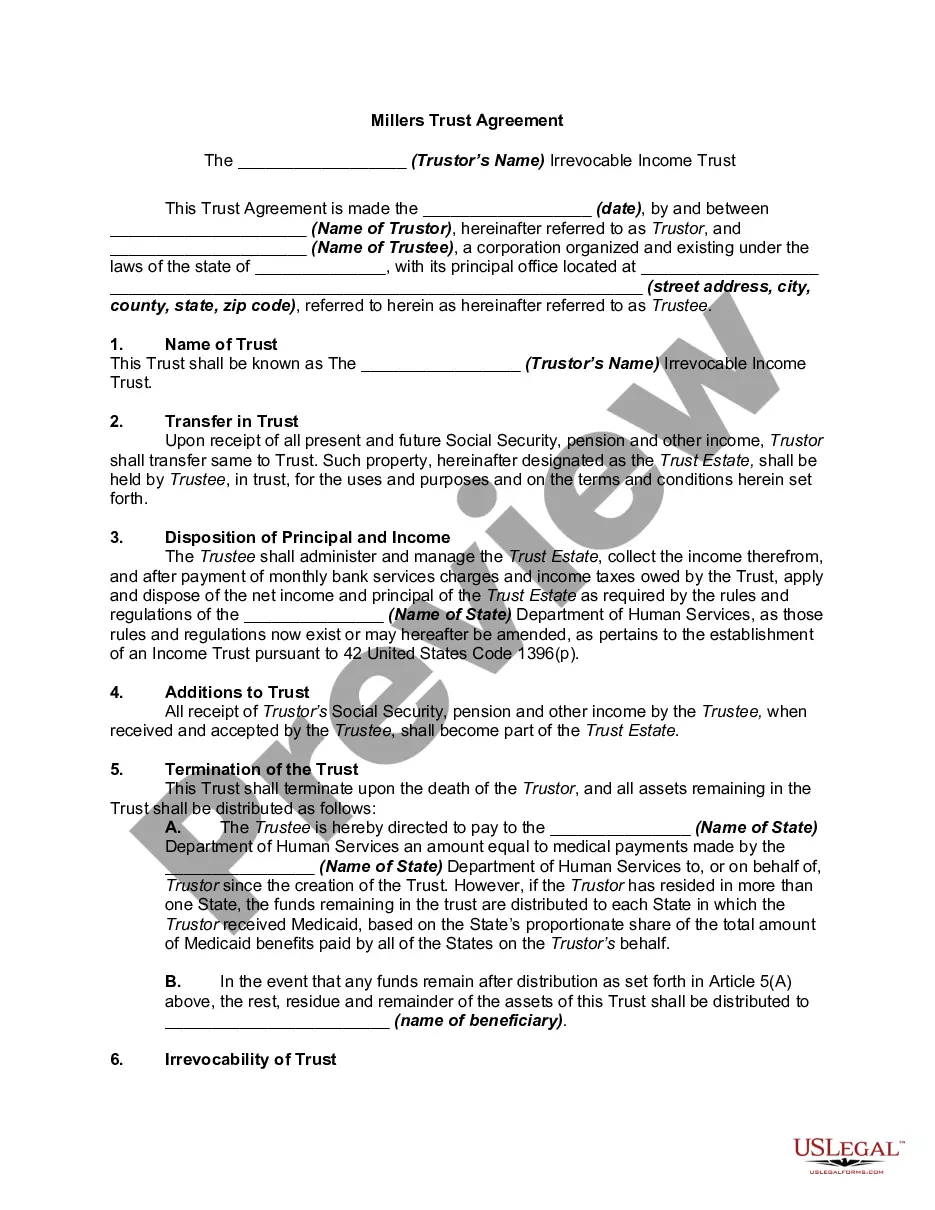

- Name of Trust: Defines the official title of the trust created by the trustor.

- Transfer in Trust: Details the transfer of income into the trust for management by the trustee.

- Disposition of Principal and Income: Outlines how the trust estate will be administered and the conditions for distributing assets upon termination.

- Termination of the Trust: Specifies the conditions under which the trust will end and how remaining assets will be distributed.

- Irrevocability of Trust: States that the trust cannot be amended or revoked unless both parties agree.

- Powers of Trustee: Describes the authority granted to the trustee to manage the trust assets.

- Accounting: Details the requirements for annual reporting and account management by the trustee.

When to use this form

This form is commonly used when an individual wishes to establish a trust to manage their income for the purpose of qualifying for Medicaid benefits while ensuring that funds are available for assisted living costs. It is particularly relevant for those who want to protect their assets from being depleted by medical expenses and who may need long-term care.

Who needs this form

- Individuals planning for assisted living who receive government benefits.

- Persons with substantial income needing to qualify for Medicaid assistance.

- Families looking to protect assets from medical expenses while meeting eligibility requirements for social services.

- Those desiring to set clear terms for the management and distribution of their trust funds.

How to prepare this document

- Identify the parties involved by entering the names of the trustor and trustee.

- Specify the name of the trust and relevant dates associated with the formation.

- Detail all income sources that will be transferred into the trust.

- Outline how the income and principal will be managed and distributed upon termination of the trust.

- Ensure that the trust is signed and acknowledged in accordance with state requirements.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, having the document notarized can provide an additional level of verification and security, ensuring that the trust is acknowledged and recognized legally.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide complete information about all income sources.

- Not following state-specific requirements leading to invalidation of the trust.

- Overlooking necessary signatures or acknowledgments needed for legality.

- Neglecting to clarify the distribution terms clearly, which can lead to disputes.

Benefits of completing this form online

- Convenient access to legal forms from anywhere, saving time and effort.

- Immediate download capability allows for prompt action on legal needs.

- Editability ensures that all specific details can be tailored to individual circumstances.

- Reliability due to forms being created by licensed attorneys to meet legal standards.

Summary of main points

- The Miller Trust Forms for Assisted Living allow for the management of income to qualify for Medicaid benefits.

- It is crucial to comply with state regulations when using this form to ensure compliance and validity.

- Properly completed trusts protect assets from being depleted by medical expenses.

- Online availability offers convenience, reliability, and the ability to customize forms easily.

Looking for another form?

Form popularity

FAQ

Some Medicaid professionals include the cost of establishing this type of trust as a package deal with other Medicaid planning services. However, on average, solely setting up a QIT runs approximately $400 to $500, but may run as high as $1,000 or $2,000.

What Is A Qualified Income Trust (QIT)? If an individual's income is over the limit to qualify for Medicaid long-term care services (including nursing home care), a Qualified Income Trust (QIT) allows an individual to become eligible by placing income into an account each month that the individual needs Medicaid.

Some Medicaid professionals include the cost of establishing this type of trust as a package deal with other Medicaid planning services. However, on average, solely setting up a QIT runs approximately $400 to $500, but may run as high as $1,000 or $2,000.

Sometimes referred to as Qualifying Income Trusts, Qualified Income Trusts, or Miller Trusts (based upon a court case with the same name), they are used when a Medicaid applicant has too much income to qualify for Medicaid but not enough to pay for nursing home care or other long-term care costs.

Payments. Miller trusts can be used to pay for a small monthly allowance, Medicare premiums and medical expenses that are not covered by Medicaid or Medicare.If there are any remaining funds after the state takes its allowed portion, these funds can go to the beneficiaries that are named in the trust.

The Miller trust can pay the Medicaid recipient a small personal needs allowance, and the trust can also be used to pay the recipient's spouse a monthly allowance.If there is any money left in the trust when the recipient dies, Medicaid has a right to the money to recover the cost of care.

Miller trusts can be used to pay for a small monthly allowance, Medicare premiums and medical expenses that are not covered by Medicaid or Medicare.If there are any remaining funds after the state takes its allowed portion, these funds can go to the beneficiaries that are named in the trust.