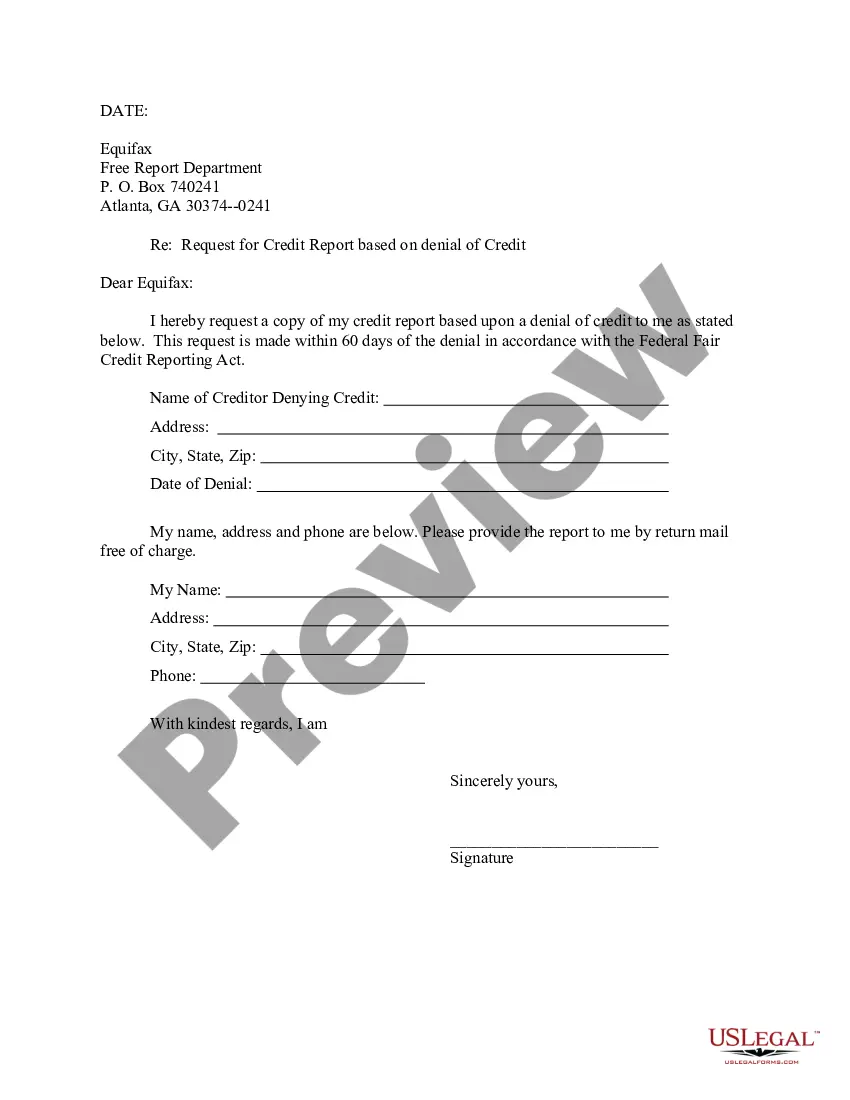

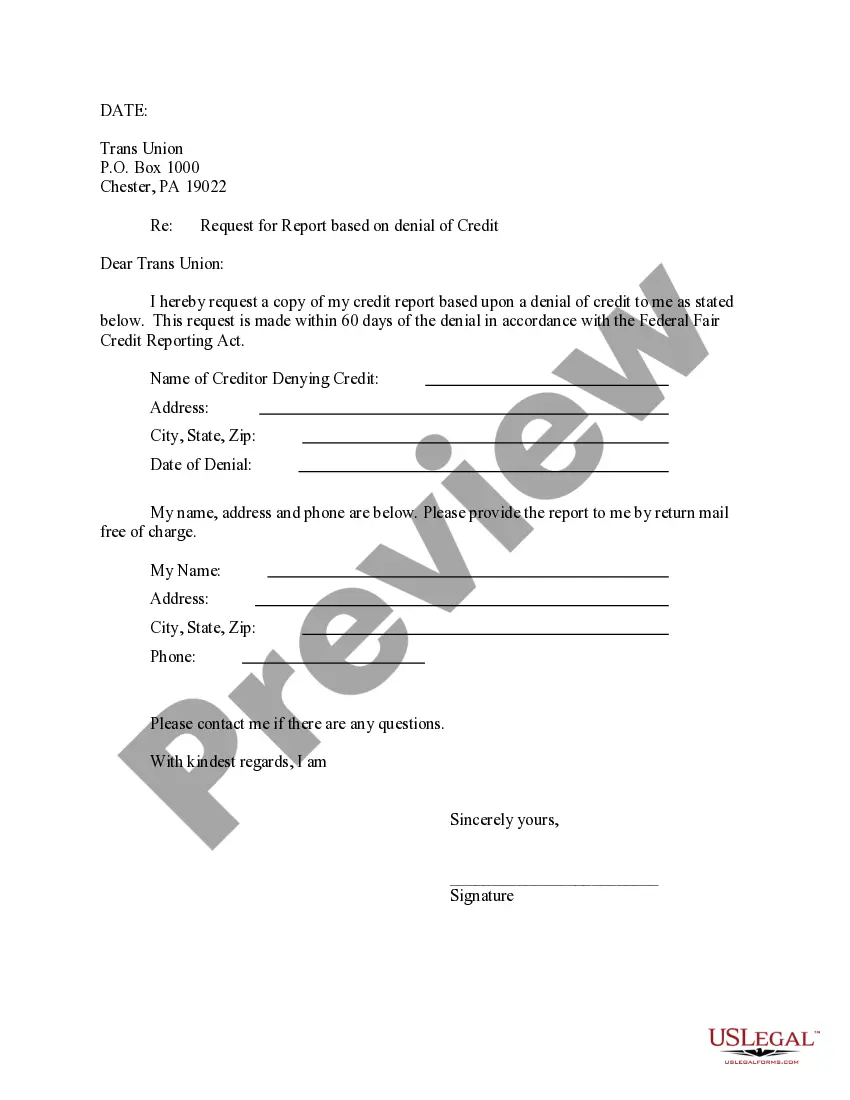

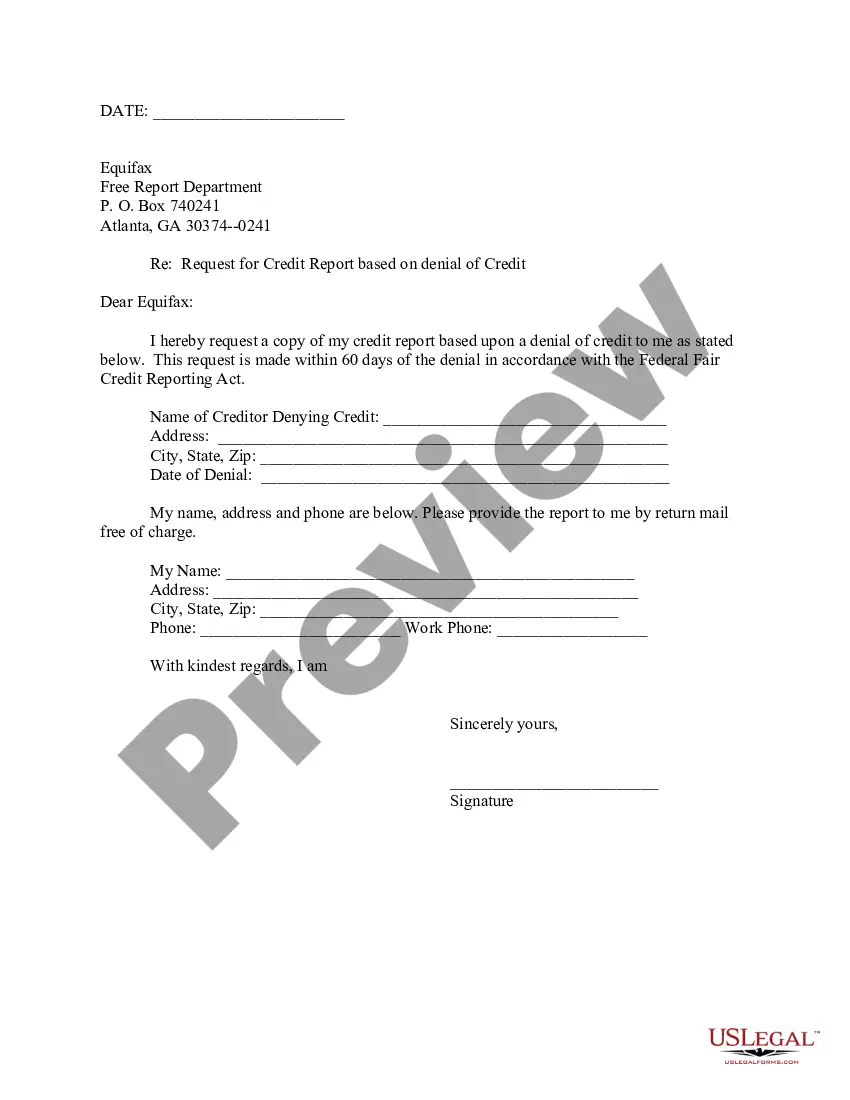

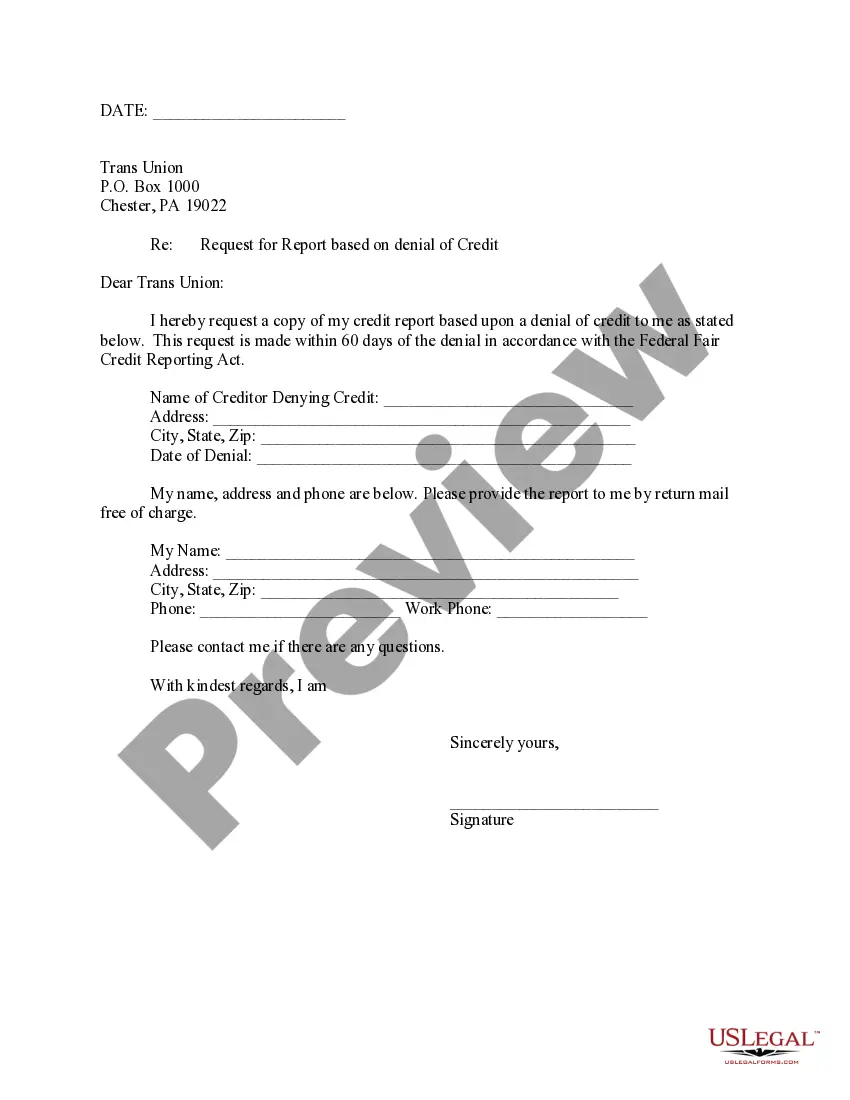

Sample Letter for Request for Free Credit Report Based on Denial of Credit

About this form

This Sample Letter for Request for Free Credit Report Based on Denial of Credit allows individuals to formally request their free credit report from a credit reporting agency after experiencing a denial of credit. This form is important for consumers who wish to check their credit history and identify any potential issues affecting their credit score. It differs from regular credit report requests as it specifically relates to a recent credit denial, ensuring eligibility for a free report under the Fair Credit Reporting Act (FCRA).

Form components explained

- Return address: Includes the sender's name and address for mailing purposes.

- Date: The date of the letter for record-keeping.

- Recipient details: Information about the credit agency to which the request is addressed.

- Request statement: A clear request for a free credit report due to credit denial within the last 60 days.

- Signature: The sender's name for identity verification.

Common use cases

This form should be used when an individual has been denied credit, such as for a loan, credit card, or mortgage application, within the last 60 days. It allows the person to request their free credit report, which can help identify the reason for the denial and provide opportunities for correction if there are errors or fraudulent activities reflected in their credit history.

Intended users of this form

- Individuals who have recently been denied credit.

- Anyone wanting to access their credit report following a credit denial.

- Consumers seeking to understand their credit situation or fix potential issues with their credit history.

How to prepare this document

- Provide your return address: Fill in your name and complete address for report delivery.

- Enter the date: Write the current date to document when the request is made.

- Fill in recipient's details: Include the name and address of the credit reporting agency.

- State your request: Clearly indicate that you are requesting a free credit report due to a recent credit denial.

- Sign the letter: At the bottom, include your full name to authenticate the request.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Not including a return address, making it difficult for the agency to send the report.

- Failing to state the reason for the request, which can lead to delays or denials.

- Not signing the letter, rendering the request invalid.

- Missing the 60-day window after credit denial to request the free report.

Why use this form online

- Convenience: Easily download and complete the form from home at any time.

- Editability: Make changes quickly to suit your particular needs.

- Reliability: Ensure you have the correct structure and language for a formal request.

Legal use & context

- This form is compliant with the Fair Credit Reporting Act, which entitles individuals to access their credit reports after being denied credit.

- Using this form helps ensure consumers are informed of their credit status and able to take corrective actions if necessary.

- Requesting a free credit report is a critical step in managing personal finances and understanding credit health.

Summary of main points

- This form is for requesting a free credit report after a credit denial.

- Understanding your credit report can help address issues that may affect future credit requests.

- It is essential to complete the form accurately to ensure the request is processed without delays.

Looking for another form?

Form popularity

FAQ

Why Can't I Get My Report Online? The most common reasons for being unable to access your credit reports online is being unable to remember key pieces of information. The other issue may be that the address you entered when requesting the report does not match the address the credit bureau has on file.

Credit report with the account in question circled and/or highlighted. Birth certificate. Social Security card. Passport (if you have one) the page showing your photo and the number.

If your credit dispute is rejected, the Fair Credit Reporting Act gives you the right to add a 100-word consumer statement to your report explaining your position.

Tell the credit reporting company, in writing, what information you think is inaccurate. Tell the information provider (that is, the person, company, or organization that provides information about you to a credit reporting company), in writing, that you dispute an item in your credit report.

Equifax. Experian or call 1-866-200-6020. TransUnion.

Does a 609 Letter Really Improve My Credit? There's no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit reportit's just another method of doing so. If the dispute is valid, the credit bureaus will remove the negative item.

The credit report you get when you're denied credit is in addition to the annual credit report that you can order once a year from the three credit bureaus through AnnualCreditReport.com.

How long information is kept by credit reference agencies. Information about you is usually held on your file for six years. Some information may be held for longer, for example, where a court has ordered that a bankruptcy restrictions order should last more than six years.

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.