Texas Financing

Overview of this form

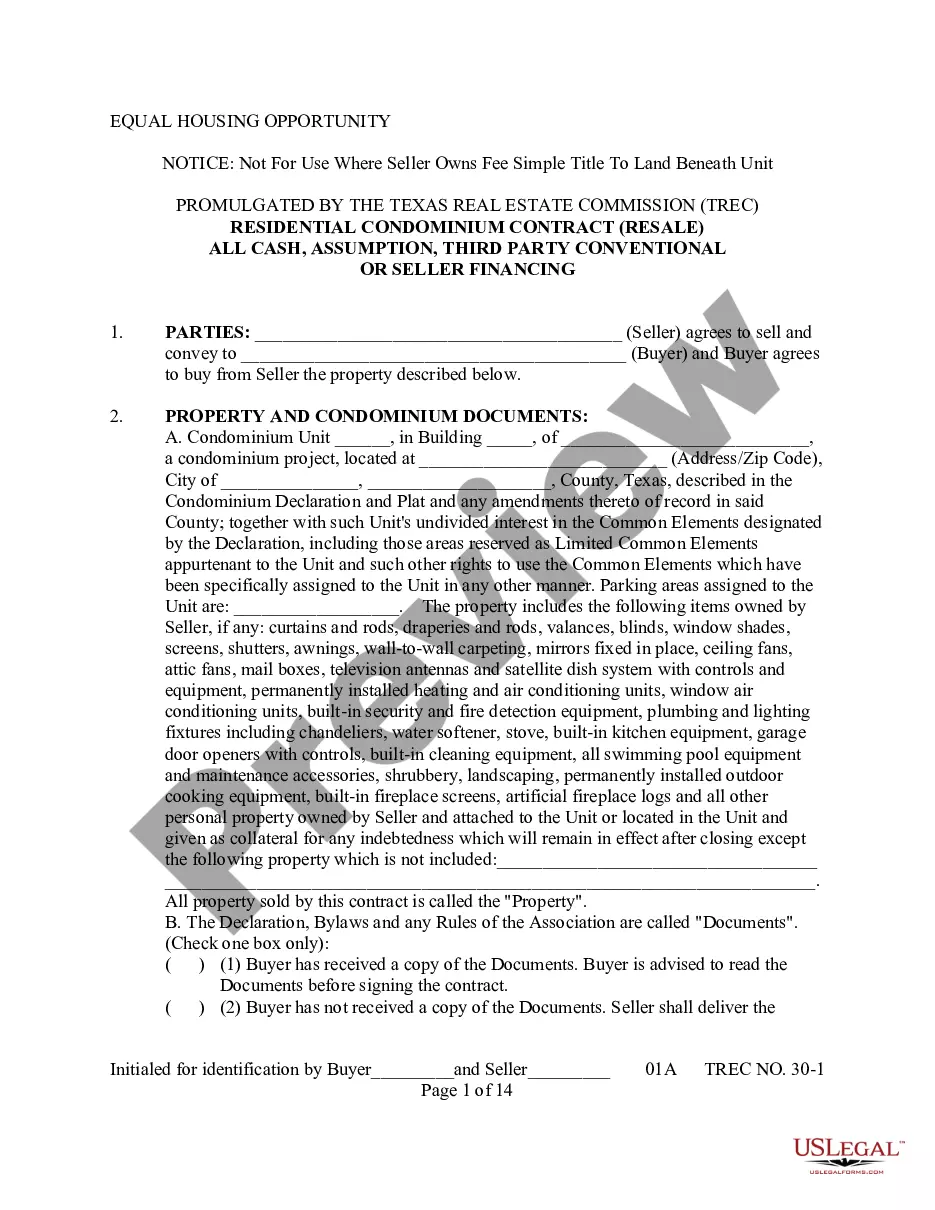

The Financing Agreement is a legal document used in Texas for the sale of condominium units. This form outlines the agreed-upon financing terms between a seller and a buyer, ensuring proper compliance with local real estate laws. It is tailored specifically for resale transactions of condominium properties and includes provisions related to FHA-insured and VA-guaranteed loans, making it distinct from other financing agreements.

Form components explained

- Identification of the parties involved in the transaction.

- Description of the property being sold, including all associated features and fixtures.

- Details about the financing terms, including loan types (FHA, VA), sale price, and earnest money requirements.

- Provisions regarding the delivery and acceptance of condominium documents and resale certificates.

- Clauses outlining responsibilities for repairs, closing procedures, and possession after closing.

When to use this document

This Financing Agreement should be used when a buyer is purchasing a condominium unit and financing the purchase through an FHA or VA loan. It is essential in situations where documentation of financing conditions is necessary to comply with Texas real estate laws. This form protects both the seller's and buyer's interests during the transaction process.

Who should use this form

- Buyers seeking to finance their purchase of a condominium in Texas.

- Sellers of condominium properties who want to ensure compliance with state regulations.

- Real estate agents facilitating transactions involving condominium sales.

How to complete this form

- Identify and fill in the names of the seller and buyer.

- Provide a detailed description of the property, including the condominium unit number and address.

- Specify the sales price and other financing details, including the loan type and earnest money deposit.

- Check the appropriate boxes regarding the receipt of condominium documents and resale certificates.

- Ensure all parties sign and date the form to finalize the agreement.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, it's advisable to check with local regulations or consult a legal professional for any specific requirements regarding notarization of real estate transactions in Texas.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to accurately describe the property details can lead to disputes.

- Not specifying payment terms clearly may result in misunderstandings.

- Overlooking the necessity of obtaining the required condominium documents before closing.

Benefits of using this form online

- Convenience of downloading the form instantly and filling it out at your own pace.

- Editability to customize the agreement to suit specific needs.

- Access to reliable templates drafted by licensed attorneys, ensuring legal compliance.

Quick recap

- The Financing Agreement is essential for outlining financing terms in a condominium sale.

- It is specifically tailored to comply with Texas laws and regulations.

- Both buyers and sellers must understand their obligations under the contract.

- Completing the form accurately helps avoid legal issues during the transaction.

Looking for another form?

Form popularity

FAQ

640 to 700: Business loan providers generally consider a credit score that falls somewhere between 640 and 700 to be goodbut not excellent. Generally, the minimum credit score for SBA and term loans is around 680.

What credit score do I need to get a business loan? You will usually need a score of at least 500 to secure a business loan, such as a short-term loan or line of credit.

Bad credit small-business loans are available from alternative sources, like online lenders. If your credit isn't great, getting a loan from a bank or credit union may be difficult. Borrowers with poor credit are considered riskier, so available loans will likely be more expensive as a result.

Lender land loans. Community banks and credit unions are more likely to offer land loans than large national banks. USDA Rural Housing Site loans. SBA 504 loans. Home equity loan. Seller financing.

Do I need to be licensed by the Department? Yes, the Texas SAFE Act requires an individual to be licensed prior to taking a residential mortgage loan application or offering or negotiating the terms of a residential mortgage loan.

A: Land loans will typically have a shorter term than home loans. Instead of a 30-year term like you would see for a mortgage, the loan could be as little as a few years.This is calculated by dividing the amount of the loan by the property's value or purchase price, whichever is lower.

A land loan is financing that allows you to purchase a plot of land. As with a home mortgage, you can obtain a land loan through a bank or a lender, who will evaluate your credit history and the value of the land to determine if you're an eligible buyer.That makes land loans a riskier transaction for a lender.

Invoice financing. Online Loans. Equipment Financing. SBA loans. Merchant Cash Advance. Business line of credit. Commercial Real Estate Loans. Microloans.

The Heritage Difference. If you're looking to buy land for hunting, recreation, an ag operation or just a place to retire on, there's one name in Texas to know. Heritage Land Bank is the right financing partner for anyone buying rural land in Texas. In fact, nobody knows Texas better.