Texas Conventional or Seller Financing

Understanding this form

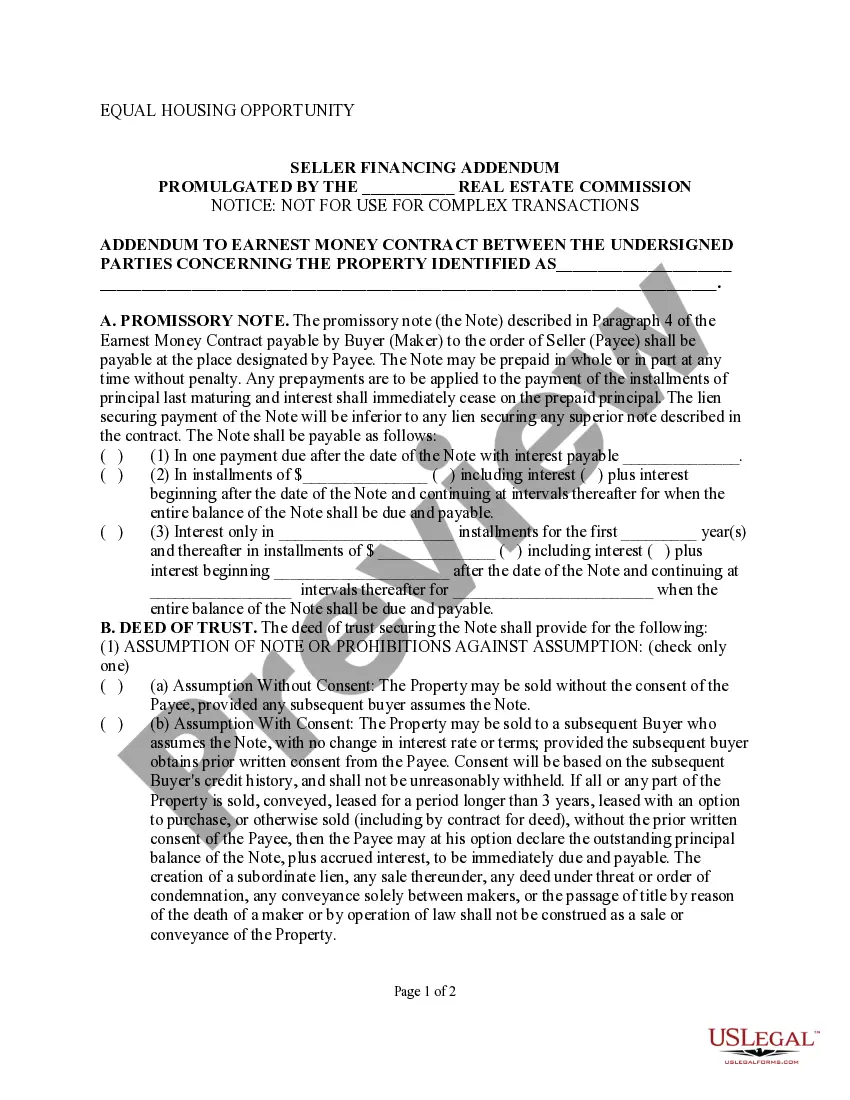

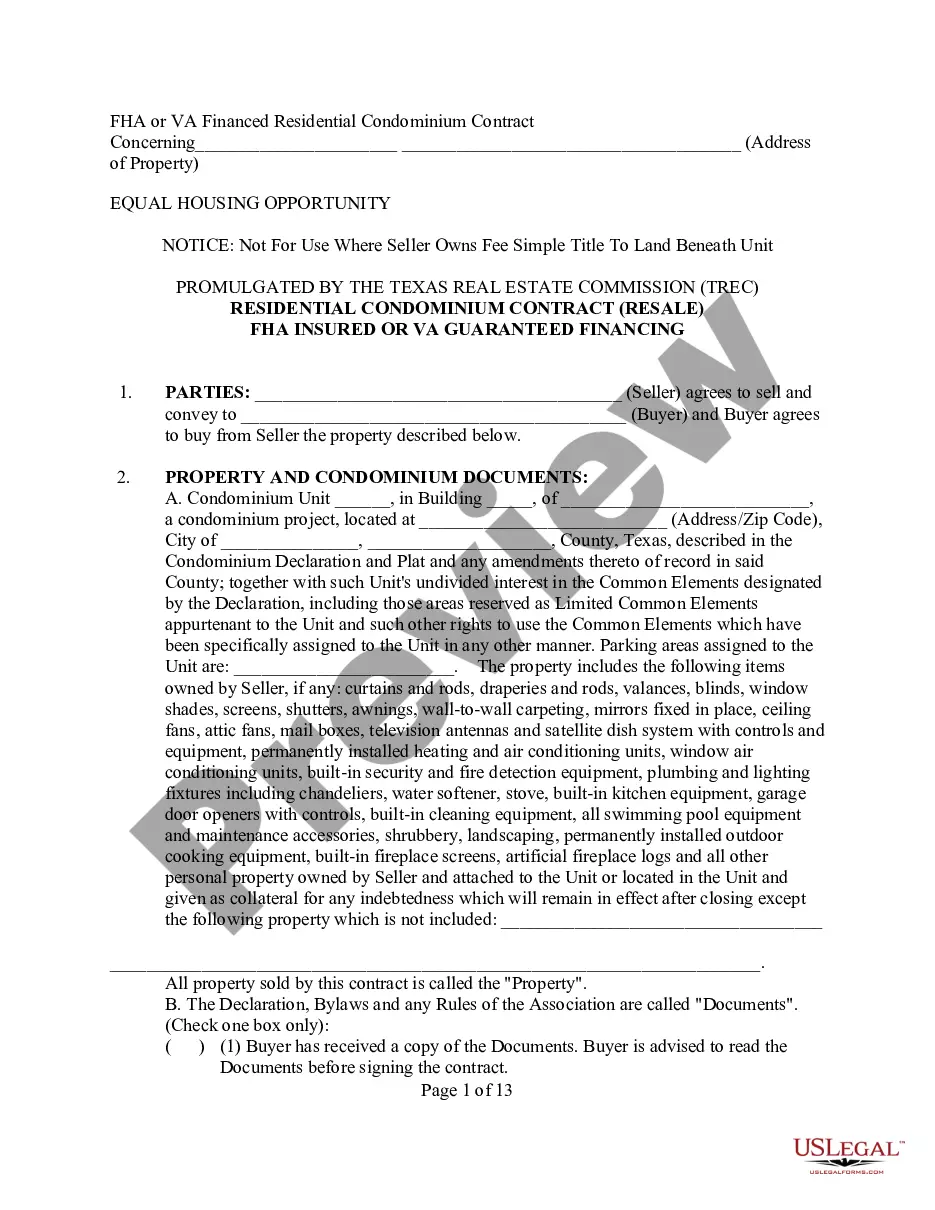

The Conventional or Seller Financing Agreement is a legal document that outlines the terms and conditions under which property is sold using either conventional financing or seller financing options. This form is specifically compliant with Texas law and is tailored for real estate transactions involving condominiums. Unlike standard purchase agreements, this form includes specific clauses related to financing, inspections, and property disclosures unique to seller financing arrangements.

Main sections of this form

- Identification of the parties (Seller and Buyer).

- Detailed description of the property being sold, including any associated condominium documents.

- Sales price breakdown between cash and financing options.

- Specific clauses regarding financing approval timelines and conditions.

- Conditions around title insurance and property inspections.

- Rights and obligations of both Buyer and Seller related to repairs and disclosures.

Common use cases

This form should be used when entering into a real estate transaction for the sale of a condominium in Texas involving financing through a lender or directly with the seller. It is particularly useful when the buyer may seek special financing options or when seller financing is being offered as part of the transaction. This type of agreement ensures clarity regarding the financial terms and the obligations of both parties.

Who can use this document

- Property Sellers who wish to offer financing options for their buyers.

- Home Buyers interested in purchasing a condominium using seller financing or conventional loans.

- Real estate agents and attorneys involved in drafting or executing real estate transactions in Texas.

- Individuals seeking to ensure compliance with Texas real estate laws during a property sale.

How to prepare this document

- Identify and fill in the names of the seller and buyer in the designated sections.

- Provide a thorough description of the condominium unit and its associated documents.

- Enter the sales price and breakdown of cash and financing options.

- Include any necessary checkboxes related to disclosures and receipt of documents.

- Ensure all signatures are obtained from both parties before finalizing the agreement.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, it is advisable to consult with a legal professional to understand any specific requirements for your transaction.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to properly identify the property being sold.

- Not providing complete financial information or timelines for financing approvals.

- Overlooking necessary checks regarding the documents related to the condominium.

- Forgetting to include signatures or date the agreement correctly.

Advantages of online completion

- Convenient access to a legally compliant agreement that can be downloaded and filled out at any time.

- Editable formats allow users to customize the document to suit specific transaction needs.

- Reliability stemming from templates prepared by licensed attorneys familiar with Texas real estate laws.

Looking for another form?

Form popularity

FAQ

Owner financing can be a good option for buyers who don't qualify for a traditional mortgage. For sellers, owner financing provides a faster way to close because buyers can skip the lengthy mortgage process.

Texas no longer allows owner-financing under last year's Texas House Bill 10 the SAFE Act unless the seller has a license. SAFE (which stands for Secure and Fair Enforcement for Mortgage Licensing Act) was passed in order to comply with a federal law of the same name.

Instead, the recommended method to provide seller financing is using a Warranty Deed, Promissory Note and Deed of Trust. Texas Property Deeds, all documents are prepared by a Texas licensed attorney Board Certified by the Texas Board of Legal Specialization in Residential Real Estate Law.

Advantages of buying an owner-financed home In a seller-financed transaction there are no closing costs such as loan origination fees, discount points and mortgage insurance premiums. Because you won't have to wait for bank approvals, closing can happen much quicker than with traditional financing.

Interest rates for seller-financed loans are typically higher than what traditional lenders would offer. The seller takes on some risk by holding financing, and he or she may charge a higher interest rate to offset this risk. It's not uncommon to see interest rates from 4% to 10%.

Owner financing can be a good option for buyers who don't qualify for a traditional mortgage. For sellers, owner financing provides a faster way to close because buyers can skip the lengthy mortgage process.

For sellers, owner financing provides a faster way to close because buyers can skip the lengthy mortgage process. Another perk for sellers is that they may be able to sell the home as-is, which allows them to pocket more money from the sale.

Owner Financing Example Over the course of the loan, the buyer makes monthly payments of $426 and is responsible for property tax and insurance payments. At closing, the buyer receives title to the home that is subject to a mortgage held by the seller.