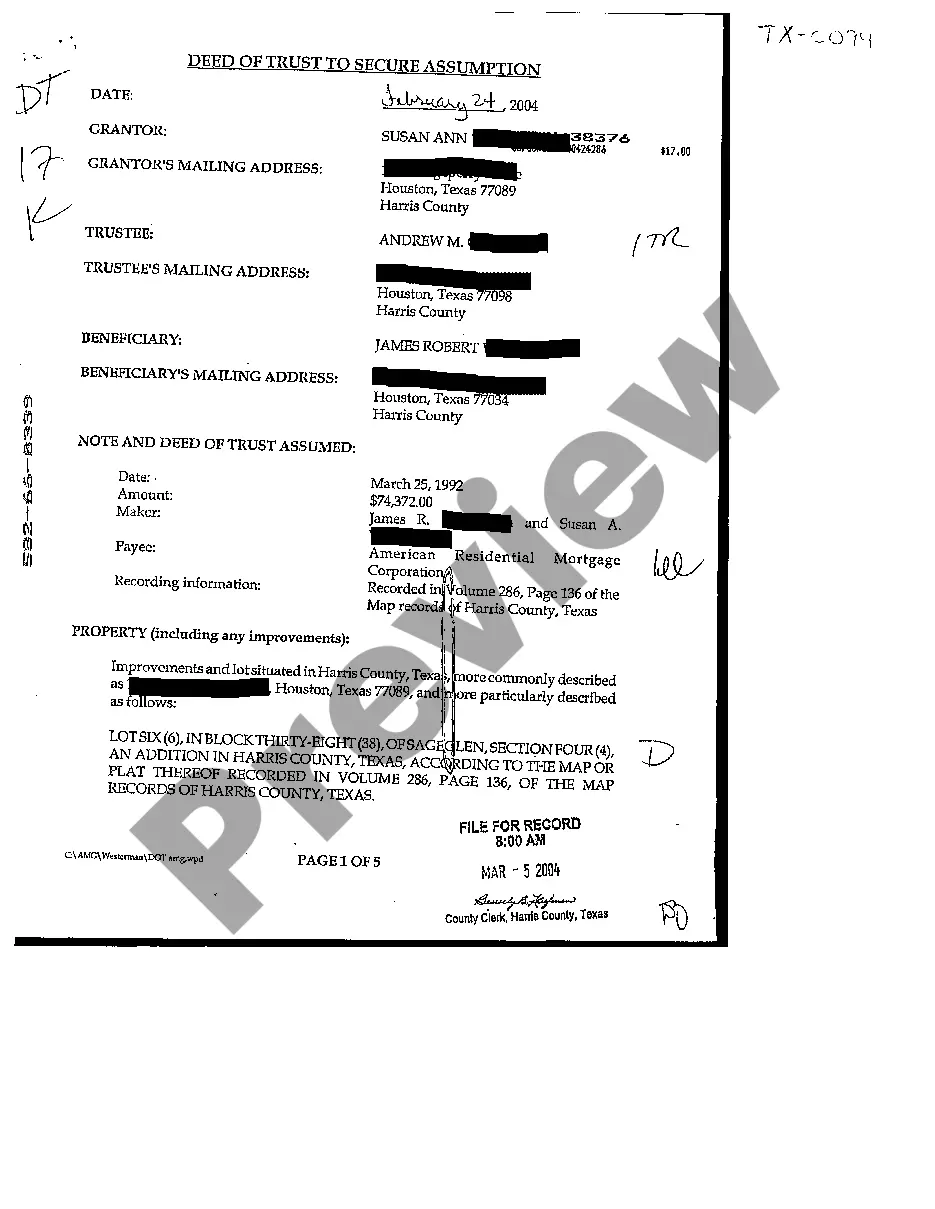

Texas Deed of Trust to Secure Assumption

What this document covers

The Deed of Trust to Secure Assumption is a legal document used in Texas that establishes a trust against a property to secure a loan assumption. This form differs from a traditional mortgage by specifically addressing the responsibilities tied to assuming an existing debt, ensuring that the new borrower is held accountable for the loan.

Main sections of this form

- Identification of Grantor, Beneficiary, and Trustee.

- Details about the property being secured.

- Terms outlining the assumption of the existing note and obligations.

- Provisions regarding the rights and duties of the Beneficiary and Trustee.

- Information about default and possible foreclosure actions.

- Assignment and handling of rental income from the property.

Common use cases

This form is typically used when a buyer wants to assume an existing mortgage on a property in Texas. It is essential in situations where the seller is willing to transfer the property along with the responsibility for the mortgage to the buyer.

Intended users of this form

- Individuals wishing to assume an existing mortgage on a property.

- Property sellers looking to facilitate a smoother sale process by allowing assumption.

- Beneficiaries requiring formal documentation to secure an assumption agreement.

Instructions for completing this form

- Identify the parties involved: Grantor (borrower), Beneficiary (lender), and Trustee.

- Specify the property being conveyed and ensure accurate legal descriptions.

- Detail the terms of the loan assumption, including any liens or restrictions.

- Enter any additional provisions regarding rights and responsibilities.

- Sign and date the deed, ensuring all parties have completed their sections.

Does this document require notarization?

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include accurate property descriptions.

- Not obtaining required signatures from all parties involved.

- Overlooking local zoning laws and regulations that may affect the property.

- Ignoring the implications of any existing liens or obligations.

Why complete this form online

- Convenience of downloading and filling out the form at your own pace.

- Editability allows customization to meet specific needs.

- Access to professionally drafted templates ensures legal compliance.

Looking for another form?

Form popularity

FAQ

The person who owns the property usually signs a promissory note and a deed of trust. The deed of trust does not have to be recorded to be valid.

A deed of assumption is a single deed that includes both the language of a general warranty or other deed along with the acknowledgement that the buyer is taking over the mortgage on the property.

Party information: names and addresses of the trustor(s), trustee(s), beneficiary(ies), and guarantor(s) (if applicable) Property details: full address of the property and its legal description (which can be obtained from the County Recorder's Office)

In real estate in the United States, a deed of trust or trust deed is a legal instrument which is used to create a security interest in real property wherein legal title in real property is transferred to a trustee, which holds it as security for a loan (debt) between a borrower and lender.

Yes, there are key differences between the two. With a deed, you transfer the ownership of the property to one party. In contrast, a deed of trust does not mean the holder owns the property. In an arrangement involving a deed of trust, the borrower signs a contract with the lender with details regarding the loan.

Some owners are put off using solicitors duke to the deed of trust cost. Individuals can write out their own, and use someone else as a witness. However, this may have errors or not be a legally binding document. The investment of getting a deed of trust when buying a property is often worth it in the long term.

The one major difference in some areas between the two is that the security deed is held by the lender whereas a trust deed is usually held by a third party.The mortgage requires a judicial action for foreclosure to take place; while the security or trust deed is a nonjudicial action where no court is involved.

A deed of trust is a written instrument with three parties: The trustor, who is the borrower and homeowner. The beneficiary, who is the lender. The trustee, who is a third party such as an insurance company or escrow management agency that holds actual title to the property in trust for the beneficiary.

The deed of trust to secure assumption is a document that names the spouse who did not receive the house as the beneficiary.If the spouse receiving the house fails to repay the mortgage lender, then the spouse who did not get the house can foreclose on the property just like any other creditor.