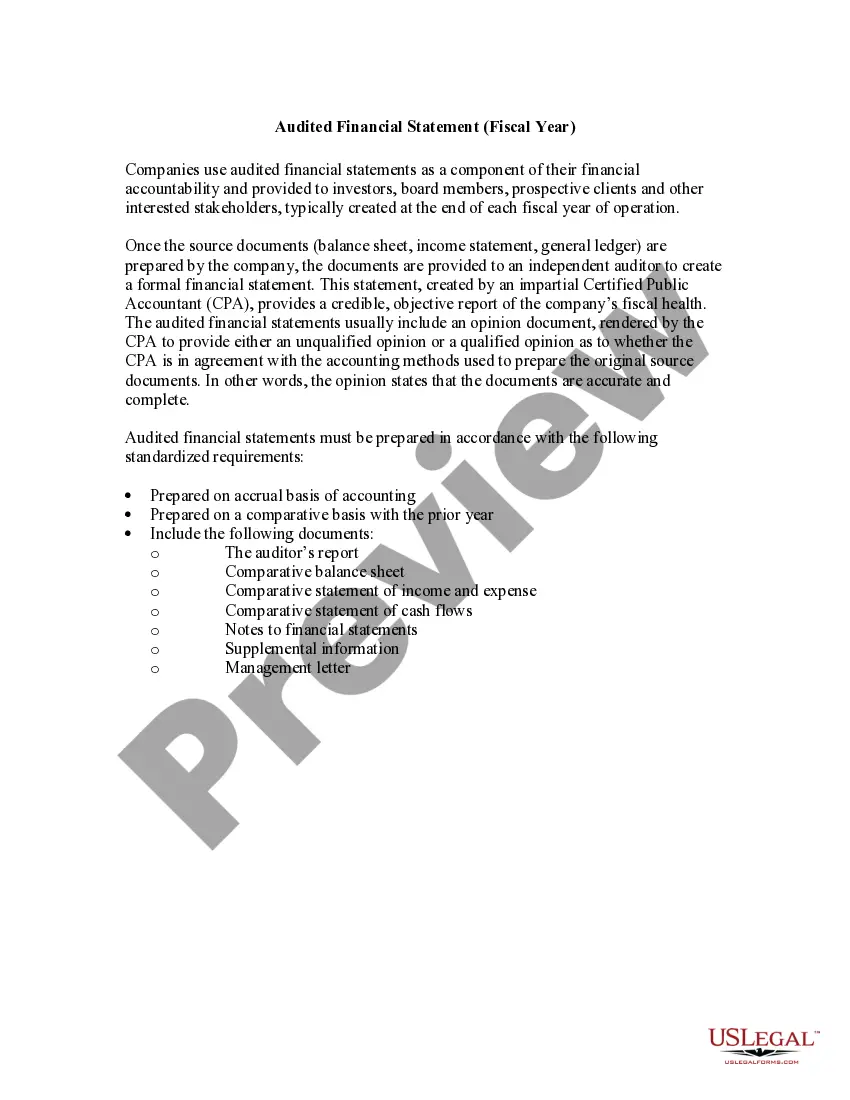

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

South Dakota Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal document templates that you can download or print.

By utilizing the site, you can access thousands of documents for business and personal use, organized by categories, states, or keywords.

You can find the latest versions of documents such as the South Dakota Report of Independent Accountants after Audit of Financial Statements in just a few minutes.

Check the form description to confirm that you have chosen the correct document.

If the document does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you already have a subscription, Log In and download the South Dakota Report of Independent Accountants after Audit of Financial Statements from the US Legal Forms catalog.

- The Download button will appear on every form you view.

- You have access to all the previously downloaded forms from the My documents section of your account.

- If you are using US Legal Forms for the first time, here are simple instructions to help you get started:

- Ensure you have selected the correct form for your city/state.

- Click the Preview button to review the form's content.

Form popularity

FAQ

Different types of entities may need to have their financial reports audited, particularly corporations and nonprofits that exceed revenue thresholds set by state regulations. In South Dakota, those that have registered with the Secretary of State or that meet specific criteria typically require the South Dakota Report of Independent Accountants after Audit of Financial Statements. This compliance ensures transparency and can be beneficial for attracting investors or applying for loans. Consider using USLegalForms to access guidelines and templates for your auditing needs.

Filing audited financial statements depends on various factors, including your business structure and annual revenue. In South Dakota, if your entity meets certain thresholds or requirements, you may need to submit a South Dakota Report of Independent Accountants after Audit of Financial Statements. This report verifies the accuracy of your financials and enhances your credibility with investors and banks. It is advisable to consult with a financial expert to determine your filing obligations.

An independent accountant, often referred to as an auditor, performs financial audits to assess the accuracy of financial statements. They are typically licensed professionals who operate independently, ensuring impartiality in their assessments. Their work culminates in the South Dakota Report of Independent Accountants after Audit of Financial Statements, which serves as a critical resource for stakeholders seeking to understand an organization's financial positioning.

The key difference between an audit and an independent examination lies in their depth and assurance level. An audit offers a higher level of assurance, as auditors conduct extensive testing of financial records. Conversely, an independent examination provides a more limited review, suitable for smaller entities. The South Dakota Report of Independent Accountants after Audit of Financial Statements clarifies these distinctions in its findings.

Yes, an audit is indeed an examination of records and financial accounts aimed at verifying their accuracy. Auditors review various documents and transactions to ensure they align with financial reporting standards. The South Dakota Report of Independent Accountants after Audit of Financial Statements reflects this thorough examination, enhancing trust in the reported figures.

An audit and an examination differ primarily in their scope and purpose. An audit provides a comprehensive evaluation of financial statements, validating their accuracy and compliance. In contrast, an examination tends to be narrower, focusing on specific financial aspects. Understanding this distinction is vital when interpreting the South Dakota Report of Independent Accountants after Audit of Financial Statements.

Writing a financial audit report involves a clear and structured approach. Auditors start by outlining their scope of work and methodologies, followed by presenting the results of their examination. The South Dakota Report of Independent Accountants after Audit of Financial Statements details the auditor's observations and recommendations, making it an essential document for stakeholders.

Independent auditors play a crucial role in ensuring the credibility of financial statements. They examine various financial records to assess their accuracy and adherence to established guidelines. The South Dakota Report of Independent Accountants after Audit of Financial Statements summarizes their findings, providing a transparent view of the organization's financial health.

An independent CPA is typically associated with financial statements when providing an audit, review, or compilation service. This relationship is crucial for ensuring that the financial information remains unbiased and compliant with applicable standards. For a comprehensive understanding, you can review the South Dakota Report of Independent Accountants after Audit of Financial Statements, which outlines the roles and responsibilities of independent CPAs in financial reporting.

The primary reason for a financial statement audit by an independent CPA is to enhance credibility and reliability. Audits reassure investors and stakeholders that financial statements accurately reflect an entity's operations and financial status. The South Dakota Report of Independent Accountants after Audit of Financial Statements further emphasizes the independent assessment's value in building trust and enhancing transparency.