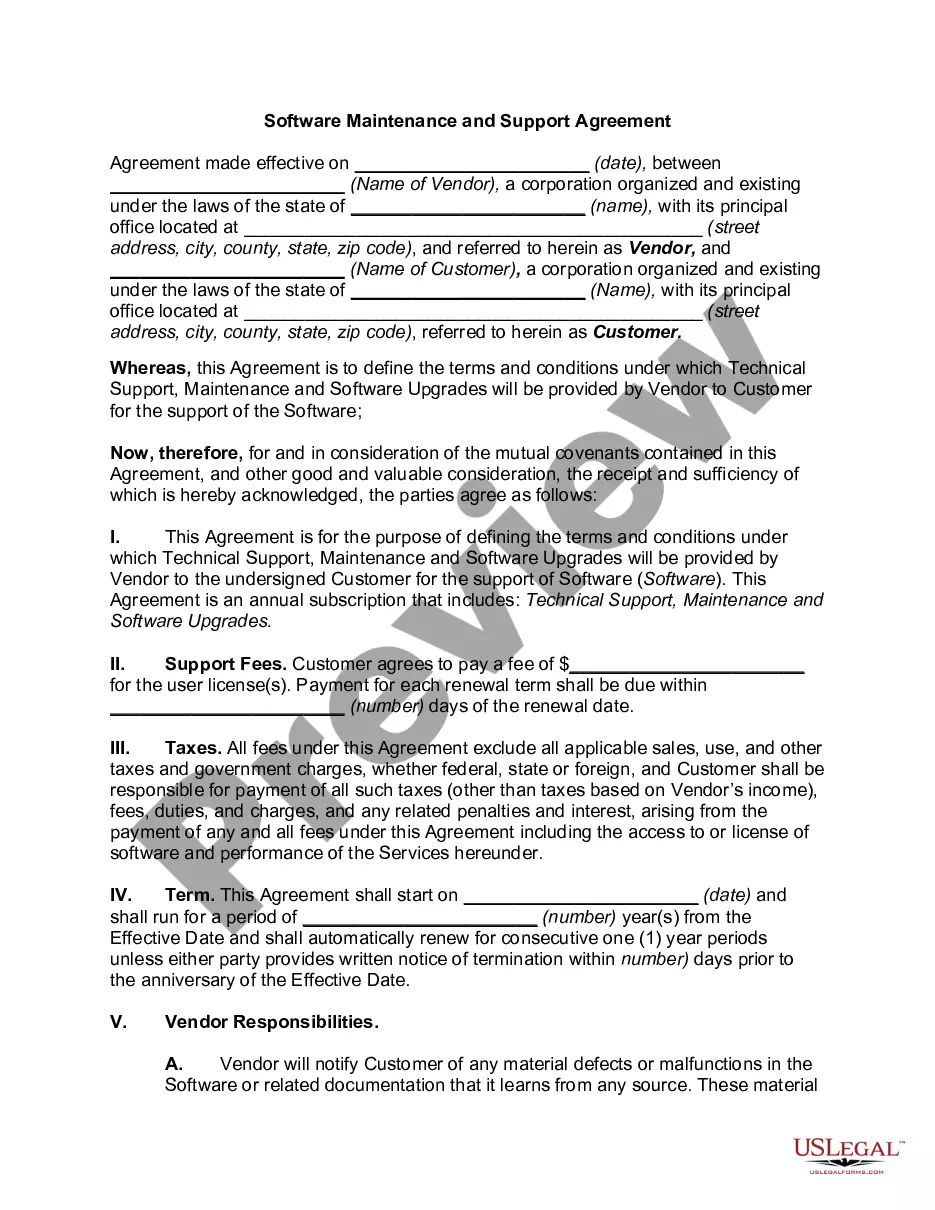

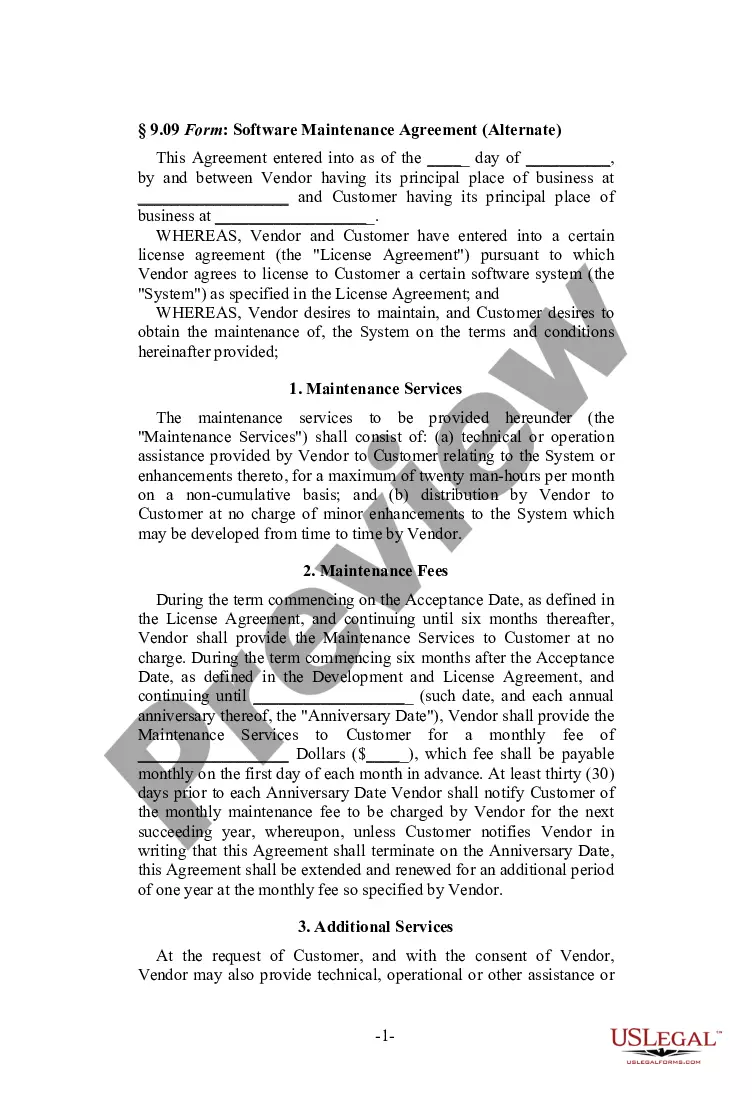

South Carolina Software Maintenance Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Software Maintenance Agreement?

Have you ever been in a circumstance where you frequently require documents for potential corporate or specific functions.

There are numerous legal document templates accessible online, but finding versions you can trust is challenging.

US Legal Forms provides thousands of template forms, such as the South Carolina Software Maintenance Agreement, which are designed to comply with state and federal regulations.

Once you locate the appropriate form, click Buy now.

Choose the payment plan you prefer, enter the necessary information to create your account, and pay for the transaction using your PayPal or credit card.

- If you're already acquainted with the US Legal Forms website and possess a free account, simply Log In.

- After that, you can download the South Carolina Software Maintenance Agreement template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Locate the form you need and ensure it pertains to the correct area/region.

- Use the Review button to inspect the form.

- Read the description to ensure that you have selected the right form.

- If the form does not match what you're looking for, use the Search box to find the form that fits your needs.

Form popularity

FAQ

In the state of South Carolina, any modifications that are made to canned software that are prepared exclusively for a specific customer are considered to be taxable custom programs, not exempt. Sales of digital products are exempt from the sales tax in South Carolina.

Yes. Charges for maintenance agreements (whether optional or mandatory) that are made in conjunction with, or as part of the sale of, computer software sold and delivered by tangible means are includable in "gross proceeds of sales" or "sales price", and, therefore, subject to the tax.

In the state of South Carolina, any modifications that are made to canned software that are prepared exclusively for a specific customer are considered to be taxable custom programs, not exempt. Sales of digital products are exempt from the sales tax in South Carolina.

South Carolina Digital products are not taxable in South Carolina. Digital products are not specifically included in the definition of tangible personal property.

Charges for renewals of warranty, maintenance or similar service contracts for tangible personal property are subject to the sales and use tax, unless otherwise exempt under the law.

Service fees for the installation of software are subject to sales tax. Moreover, charges for software maintenance services including delivery of updates for prewritten software are generally taxable. However, maintenance contracts that only provide support services for canned software are not taxable.

If a business purchases a digital good (only digital goods, NOT digital automated services or remote access software) for business purposes, then the purchase is exempt from sales tax.

Traditional Goods or Services Goods that are subject to sales tax in South Carolina include physical property, like furniture, home appliances, and motor vehicles. Prescription medicines, groceries, and gasoline are all tax-exempt.

Sales tax is imposed on the sale of goods and certain services in South Carolina. The statewide sales and use tax rate is six percent (6%). Counties may impose an additional one percent (1%) local sales tax if voters in that county approve the tax. Generally, all retail sales are subject to the sales tax.

In the state of South Carolina, any modifications that are made to canned software that are prepared exclusively for a specific customer are considered to be taxable custom programs, not exempt. Sales of digital products are exempt from the sales tax in South Carolina.