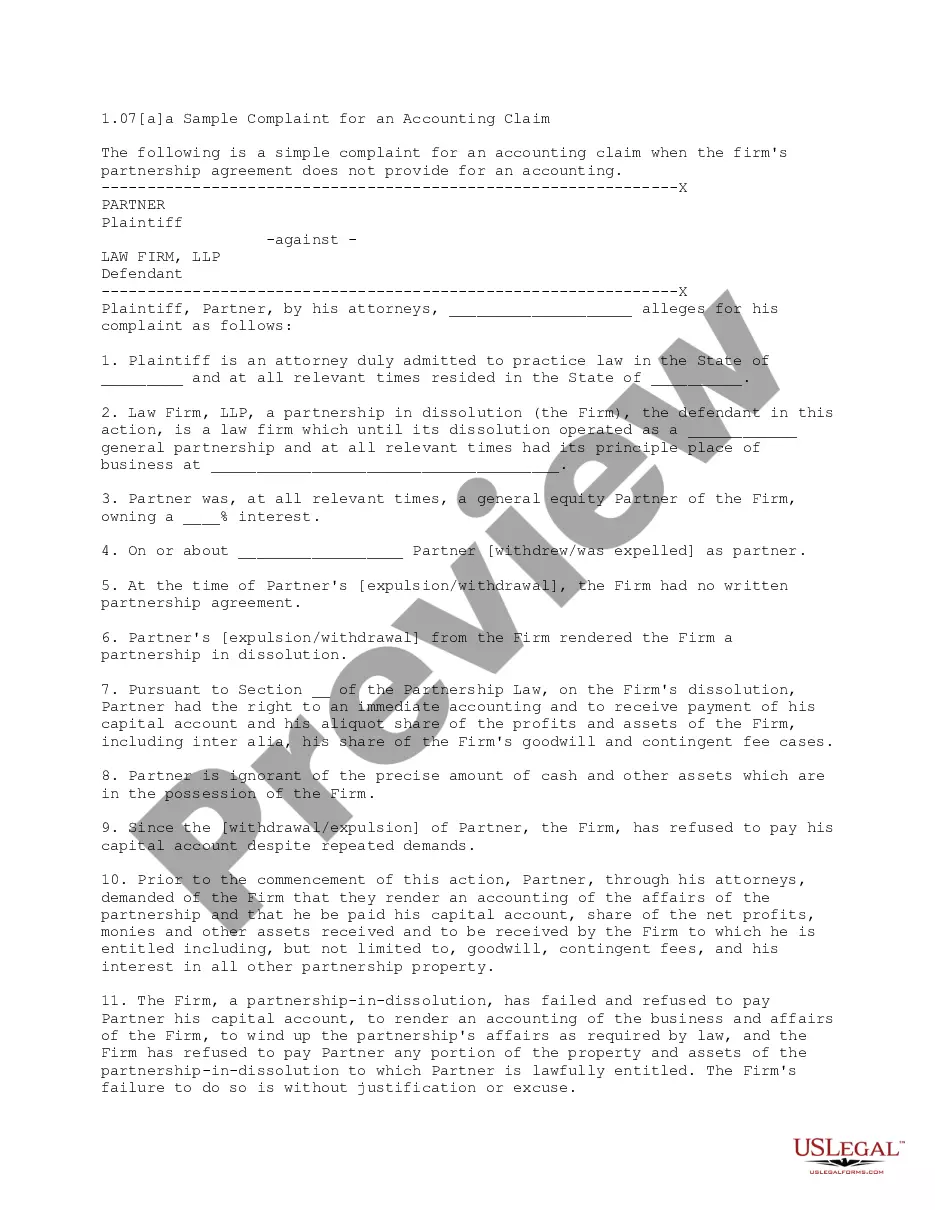

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Pennsylvania Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

If you wish to comprehensive, acquire, or produce legitimate file themes, use US Legal Forms, the largest assortment of legitimate types, which can be found online. Utilize the site`s basic and hassle-free research to find the documents you will need. Numerous themes for enterprise and individual purposes are sorted by groups and states, or keywords. Use US Legal Forms to find the Pennsylvania Alternative Complaint for an Accounting which includes Egregious Acts within a handful of clicks.

When you are previously a US Legal Forms consumer, log in to your profile and click on the Obtain button to get the Pennsylvania Alternative Complaint for an Accounting which includes Egregious Acts. You can even access types you formerly acquired within the My Forms tab of your own profile.

If you work with US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Be sure you have chosen the form for the appropriate metropolis/country.

- Step 2. Take advantage of the Review option to look through the form`s articles. Do not overlook to learn the information.

- Step 3. When you are not satisfied using the form, use the Research discipline at the top of the monitor to find other models of your legitimate form format.

- Step 4. After you have discovered the form you will need, go through the Purchase now button. Pick the rates program you prefer and add your accreditations to sign up for an profile.

- Step 5. Process the transaction. You can use your charge card or PayPal profile to finish the transaction.

- Step 6. Select the formatting of your legitimate form and acquire it on the device.

- Step 7. Complete, modify and produce or signal the Pennsylvania Alternative Complaint for an Accounting which includes Egregious Acts.

Every legitimate file format you purchase is your own forever. You may have acces to every single form you acquired inside your acccount. Click the My Forms area and pick a form to produce or acquire yet again.

Compete and acquire, and produce the Pennsylvania Alternative Complaint for an Accounting which includes Egregious Acts with US Legal Forms. There are thousands of professional and condition-distinct types you may use for your enterprise or individual demands.

Form popularity

FAQ

Under Pennsylvania law, executors have a duty to provide an accounting to beneficiaries. An accounting is a detailed report that outlines the assets, liabilities, income, and expenses associated with the estate, as well as the executor's actions in managing and distributing the estate.

Legally, the executor cannot change the will or refuse payment, but executors can breach their fiduciary duty, as explained below, leaving beneficiaries vulnerable to creditors.

Rule 1065.1. C.S. § 5527.1. Section 5527.1 of the Judicial Code permits a party to seek to acquire title to real property by commencing an action to quiet title if the party has adversely possessed the real property for a period of not less than ten years.

As a beneficiary, you are entitled to review the trust's records including bank statements, the checking account ledger, receipts, invoices, etc. Before the trust administration is complete, it is recommended you request and review the trust's records which support the accounting.

An action in ejectment is required to obtain possession of the property and an action in assumpsit is required to recover the rent. Although not permitted in the court of common pleas, such joinder is permitted by the Rules of Civil Procedure for Justices of the Peace. Pa.

Rule 1066 - Form of Judgment or Order (a) The court shall grant appropriate relief upon affidavit that a complaint containing a notice to defend has been served and that the defendant has not filed an answer, or after a hearing or trial on the pleadings or merits.

Beneficiary designations most often supersede all outside Estate Plans and agreements (including divorce and prenuptial agreements). And don't worry, as long as you're living, your beneficiary doesn't have access to your account unless you've set them up as a cosigner.

The Executor Must Notify All Potential Beneficiaries Bequests of a percentage or share of an estate are typically calculated after debts have been paid and specific bequests have been made.