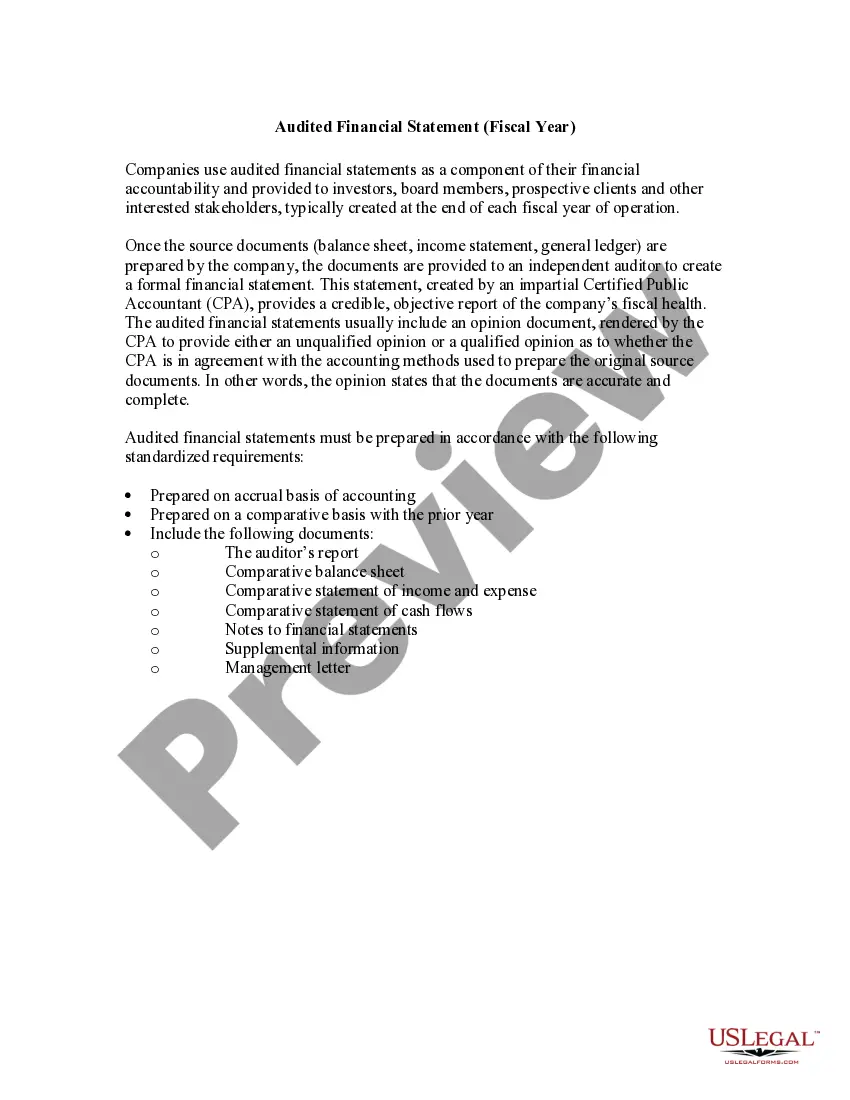

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

Pennsylvania Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

Are you presently located in a venue where you require documents for either business or personal reasons almost every day.

There are numerous legal document templates accessible online, but finding reliable ones isn’t straightforward.

US Legal Forms provides thousands of template forms, including the Pennsylvania Report of Independent Accountants after Audit of Financial Statements, developed to comply with federal and state regulations.

Once you find the correct form, click on Buy now.

Choose the pricing plan you prefer, fill in the required information to create your account, and pay for the order using your PayPal or credit card.

- If you are already acquainted with the US Legal Forms website and have an account, simply Log In.

- After that, you can download the Pennsylvania Report of Independent Accountants after Audit of Financial Statements template.

- If you do not possess an account and wish to start using US Legal Forms, follow these steps.

- Select the form you need and ensure it is for the correct city/state.

- Utilize the Preview button to review the form.

- Examine the details to confirm that you have selected the appropriate form.

- If the form isn’t what you are looking for, use the Search field to find the form that meets your needs and requirements.

Form popularity

FAQ

An independent CPA can assist in preparing the financial statements of a publicly held entity if they remain objective and maintain their independence. This involvement can ensure that the financial reports are accurate and align with regulatory standards. The result is a Pennsylvania Report of Independent Accountants after Audit of Financial Statements, which bolsters the integrity and reliability of the financial information provided.

Management is responsible for preparing and presenting the financial statements of a public company. They must comply with accounting standards and regulatory requirements. An independent CPA will audit these statements and provide a Pennsylvania Report of Independent Accountants after Audit of Financial Statements, which is essential for maintaining investor confidence.

The management of an organization is ultimately responsible for the preparation of audited financial statements. They ensure that the statements are accurate and adhere to applicable accounting principles. The independent CPA then reviews these statements and provides a Pennsylvania Report of Independent Accountants after Audit of Financial Statements, which adds an extra layer of accountability.

Yes, a CPA can prepare personal financial statements to reflect an individual's financial position accurately. However, if the CPA conducts an audit of those statements, they must issue a Pennsylvania Report of Independent Accountants after Audit of Financial Statements to ensure transparency. This report assures the user that the CPA's work meets necessary standards.

The purpose of an independent CPA firm audit is to provide an objective assessment of the financial statements' accuracy and compliance with accounting standards. This process culminates in a Pennsylvania Report of Independent Accountants after Audit of Financial Statements, which serves as a vital tool for investors and regulators. An audit enhances transparency and helps businesses identify areas for improvement.

Yes, a CPA must maintain independence in both fact and appearance when offering services such as audits and reviews. This principle ensures the integrity of the financial statements and builds trust in the Pennsylvania Report of Independent Accountants after Audit of Financial Statements. Independence safeguards against conflicts of interest and promotes objectivity, which is critical for the users of the report.

The primary purpose of the independent review is to provide a level of assurance about the accuracy of financial statements without conducting an exhaustive audit. This process helps increase confidence among stakeholders, such as investors and creditors. An independent review can streamline the path to obtaining a Pennsylvania Report of Independent Accountants after Audit of Financial Statements when comprehensive scrutiny is necessary for regulatory or financial purposes.

An independent financial review involves a CPA assessing financial statements without conducting a full audit. The goal is to provide a moderate level of assurance to stakeholders about the accuracy of the financial data presented. This type of review can be beneficial for businesses looking to build credibility while also considering the costs associated with a full audit. A Pennsylvania Report of Independent Accountants after Audit of Financial Statements may follow this process when a more in-depth analysis is needed.

Independently reviewed financial statements are documents that have undergone an evaluation by a CPA or independent reviewer, ensuring accuracy and compliance. This process provides a report that conveys a level of trust and assurance, although it is not as detailed as an audit. Many businesses use these statements to support their financial health and might later require a Pennsylvania Report of Independent Accountants after Audit of Financial Statements for further validation.

An audit is a thorough examination of financial statements conducted by a CPA, while an independent review is a less extensive evaluation. Audits provide a high level of assurance, often resulting in a Pennsylvania Report of Independent Accountants after Audit of Financial Statements. In contrast, independent reviews offer limited assurance and focus on key financial aspects without comprehensive testing.