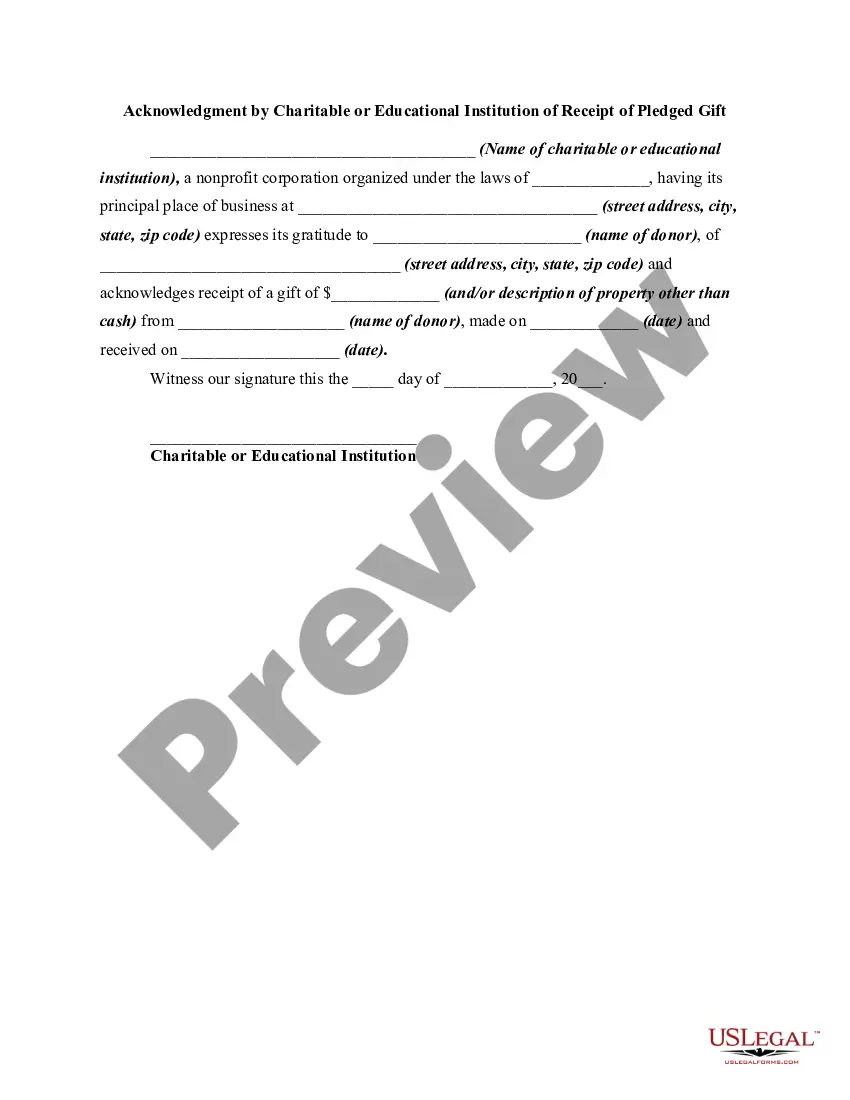

Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Acknowledgment By Charitable Or Educational Institution Of Receipt Of Gift?

Selecting the ideal legal document web template can be a challenge. Clearly, there are numerous templates available online, but how can you locate the specific legal type you require? Utilize the US Legal Forms website. The service provides a vast array of templates, such as the Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift, which can be utilized for business and personal purposes. All of the forms are vetted by experts and comply with state and federal regulations.

If you are already registered, Log In to your account and click the Obtain button to access the Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Use your account to review the legal documents you have previously acquired. Navigate to the My documents section of your account and obtain another copy of the documents you require.

If you are a new user of US Legal Forms, here are some straightforward tips for you to follow: First, ensure that you have selected the correct type for your area/region. You can preview the form using the Review button and examine the form outline to confirm that it is indeed the right one for you. If the form does not meet your requirements, utilize the Search field to find the appropriate form. Once you are confident that the form is suitable, click the Acquire now button to obtain the form. Choose the pricing plan you desire and enter the necessary information. Create your account and complete the purchase using your PayPal account or credit card. Select the file format and download the legal document template to your device. Complete, modify, print, and sign the obtained Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift.

Make the most of US Legal Forms to efficiently acquire the legal documents you need.

- US Legal Forms is the largest library of legal documents where you can find various paper templates.

- Utilize the service to download professionally-crafted documents that adhere to state requirements.

- Access a wide selection of legal forms tailored to your needs.

- Ensure compliance with both state and federal regulations.

- Easily manage your previously acquired legal documents through your account.

- Streamline the process of obtaining legal templates for personal or business use.

Form popularity

FAQ

To give a receipt for a charitable donation, you must create a document that includes the donor's name, the amount donated, and a statement confirming that no goods or services were provided in exchange for the gift. A Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift is a great example of how to format this receipt. By using platforms like uslegalforms, you can easily generate compliant acknowledgment letters that meet all necessary legal requirements.

The PA Charitable Solicitation Act regulates how charities can solicit donations in Pennsylvania. It requires organizations to register and maintain transparency regarding their fundraising activities. Understanding this act is essential for nonprofits to ensure compliance and to provide proper acknowledgments, such as a Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift, to their donors.

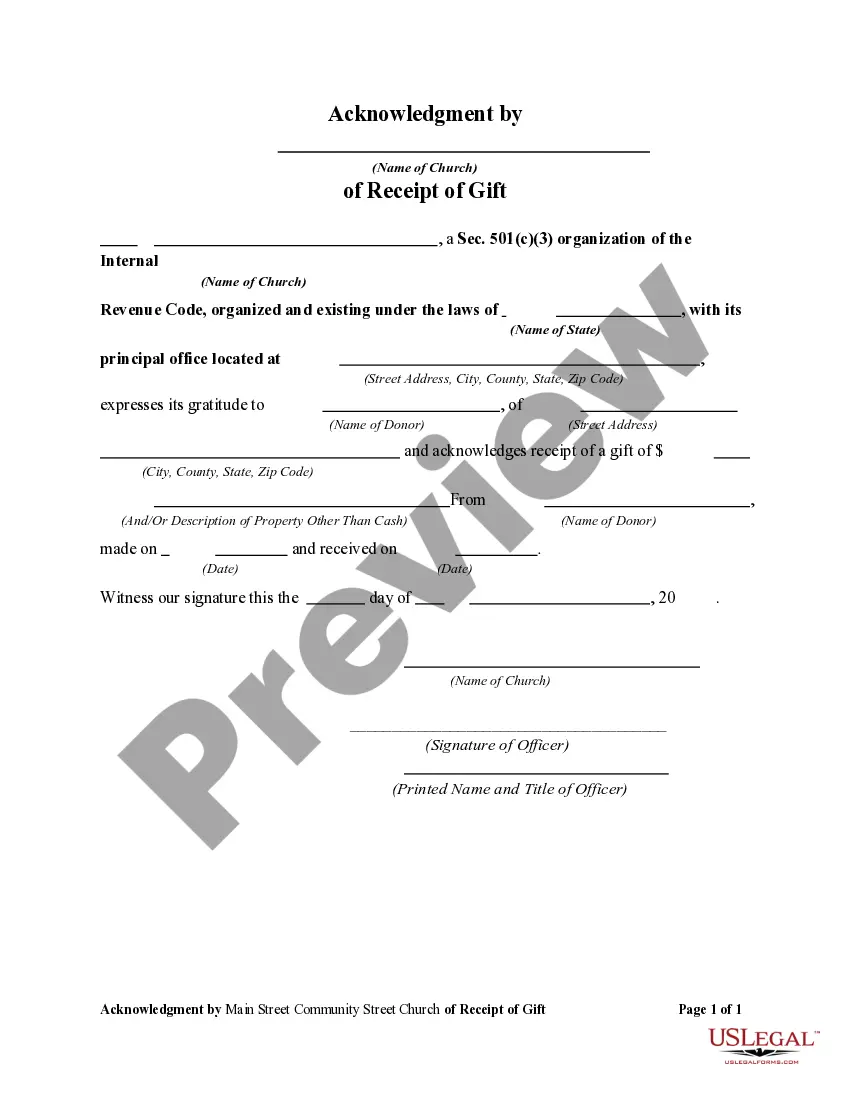

To acknowledge receipt of a donation, you should send a written confirmation to the donor as soon as possible. A Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift should include key details such as the date of the donation, the donor's name, and a statement expressing gratitude. This acknowledgment not only strengthens relationships with donors but also fulfills legal requirements for charitable organizations.

A written acknowledgment for a charitable contribution typically includes the name of the donor, the amount of the gift, and the name of the charitable organization. For example, a Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift may state, 'Thank you for your generous donation of $100 to our organization. Your support helps us continue our mission.' This document serves as a formal recognition of the donation and is essential for tax purposes.

To write a receipt for a charitable donation, start by including the organization's name, address, and tax-exempt status. Next, provide the donor's name, the date of the donation, and a detailed description of the gift. Highlight that this document serves as a Pennsylvania Acknowledgment by Charitable or Educational Institution of Receipt of Gift, which the donor can use for tax purposes. Utilizing platforms like uslegalforms can help streamline this process, ensuring that you meet all legal requirements.

To be considered contemporaneous with the contribution, a written acknowledgment must be received by the donor by the earlier of: The date on which the donor files his or her individual federal income tax return for the year of the contribution; or. The due date (including extensions) of the return.

We recommend sending either a donation acknowledgment letter or a donation thank you letter every time a donor gives. This lets you express gratitude for donors' support, share your progress and future goals, and ensure they know you received their gift.

A 501(c)(3) donation receipt is a written acknowledgment provided by a nonprofit organization to a donor for a tax-deductible donation. It includes specific information required by the IRS to confirm the tax-exempt status of the organization and the deductible amount of the donation.

Any donations worth $250 or more must be recognized with a receipt. The charity receiving this donation must automatically provide the donor with a receipt. As a general rule a nonprofit organization should NOT place a value on what is donated (that is the responsibility of the donor).

Acknowledgement refers to a formal declaration before an official that one has executed a particular legal document.