Pennsylvania REV-571 Instructions -- Instructions for REV-571 Schedule C-SB — Small Business Exemption provide Pennsylvania businesses with a way to apply for a sales tax exemption. The instructions consist of three parts: Part 1- General Information and Instructions; Part 2- Exemption Eligibility Requirements; and Part 3- Exemption Application. Part 1-General Information and Instructions provides a general overview of the exemption, including information on who is eligible to apply, how to apply, and how to maintain the exemption. Part 2- Exemption Eligibility Requirements outlines the eligibility criteria for the exemption. These include the types of businesses eligible for the exemption, the size of the business, and the types of sales that qualify. Part 3- Exemption Application provides instructions on how to complete the REV-571 Schedule C-SB — Small Business Exemption form. The form must be completed in its entirety and include a copy of the business’s Articles of Incorporation, a copy of the business’s most recent federal income tax return, and other supporting documentation. There are two types of Pennsylvania REV-571 Instructions -- Instructions for REV-571 Schedule C-SB — Small Business Exemption: one for corporations and one for sole proprietors.

Pennsylvania REV-571 Instructions -- Instructions for REV-571 Schedule C-SB - Small Business Exemption

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Pennsylvania REV-571 Instructions -- Instructions For REV-571 Schedule C-SB - Small Business Exemption?

Preparing legal paperwork can be a real stress if you don’t have ready-to-use fillable templates. With the US Legal Forms online library of formal documentation, you can be confident in the blanks you find, as all of them correspond with federal and state laws and are checked by our specialists. So if you need to prepare Pennsylvania REV-571 Instructions -- Instructions for REV-571 Schedule C-SB - Small Business Exemption, our service is the perfect place to download it.

Obtaining your Pennsylvania REV-571 Instructions -- Instructions for REV-571 Schedule C-SB - Small Business Exemption from our library is as easy as ABC. Previously authorized users with a valid subscription need only log in and click the Download button after they find the proper template. Later, if they need to, users can get the same blank from the My Forms tab of their profile. However, even if you are new to our service, signing up with a valid subscription will take only a few moments. Here’s a brief instruction for you:

- Document compliance verification. You should attentively review the content of the form you want and ensure whether it suits your needs and complies with your state law regulations. Previewing your document and looking through its general description will help you do just that.

- Alternative search (optional). If there are any inconsistencies, browse the library using the Search tab above until you find an appropriate blank, and click Buy Now when you see the one you want.

- Account registration and form purchase. Sign up for an account with US Legal Forms. After account verification, log in and select your preferred subscription plan. Make a payment to proceed (PayPal and credit card options are available).

- Template download and further usage. Select the file format for your Pennsylvania REV-571 Instructions -- Instructions for REV-571 Schedule C-SB - Small Business Exemption and click Download to save it on your device. Print it to fill out your papers manually, or take advantage of a multi-featured online editor to prepare an electronic copy faster and more efficiently.

Haven’t you tried US Legal Forms yet? Subscribe to our service now to get any official document quickly and easily every time you need to, and keep your paperwork in order!

Form popularity

FAQ

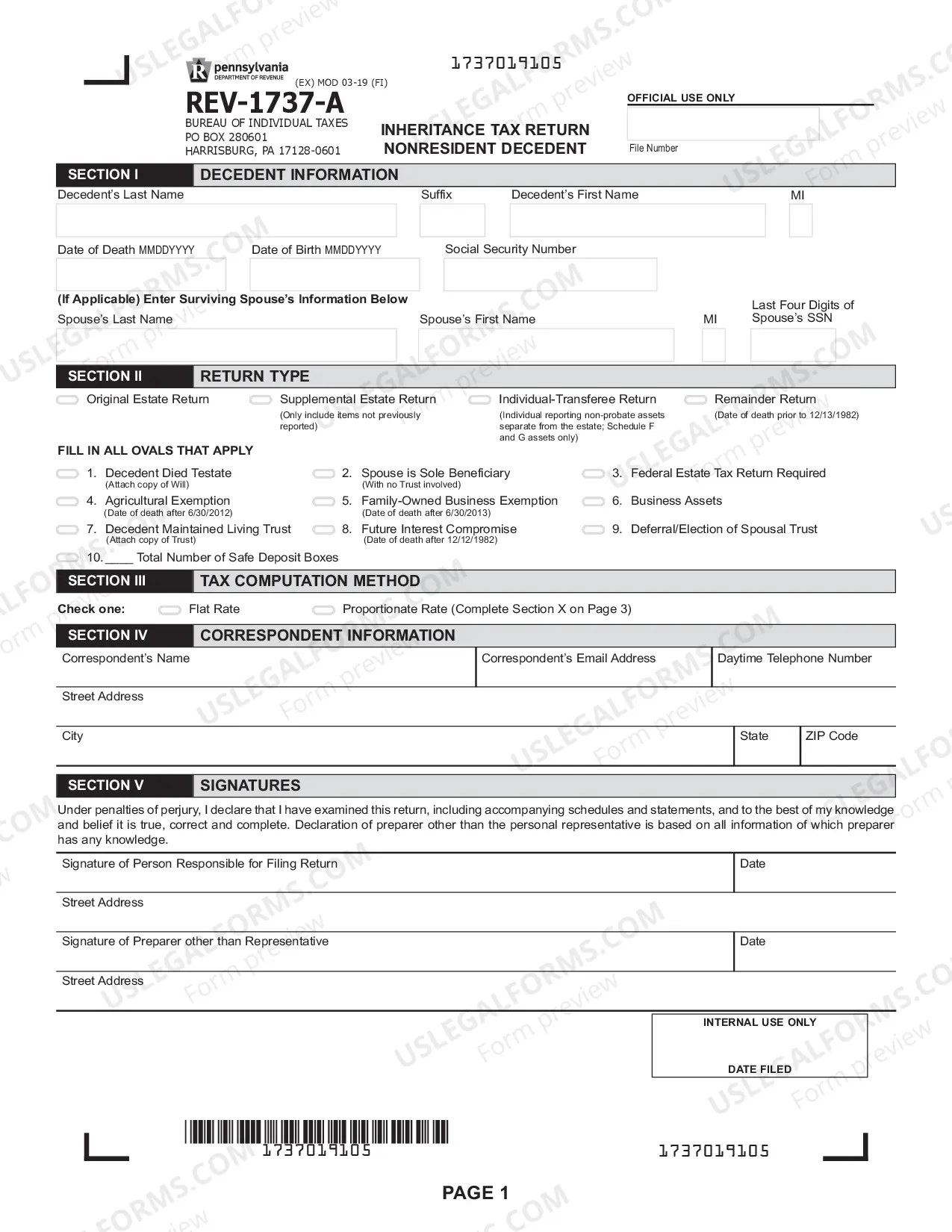

Property owned jointly between husband and wife is exempt from inheritance tax, while property inherited from a spouse, or from a child aged 21 or younger by a parent, is taxed a rate of 0%. Inheritance tax returns are due nine calendar months after a person's death.

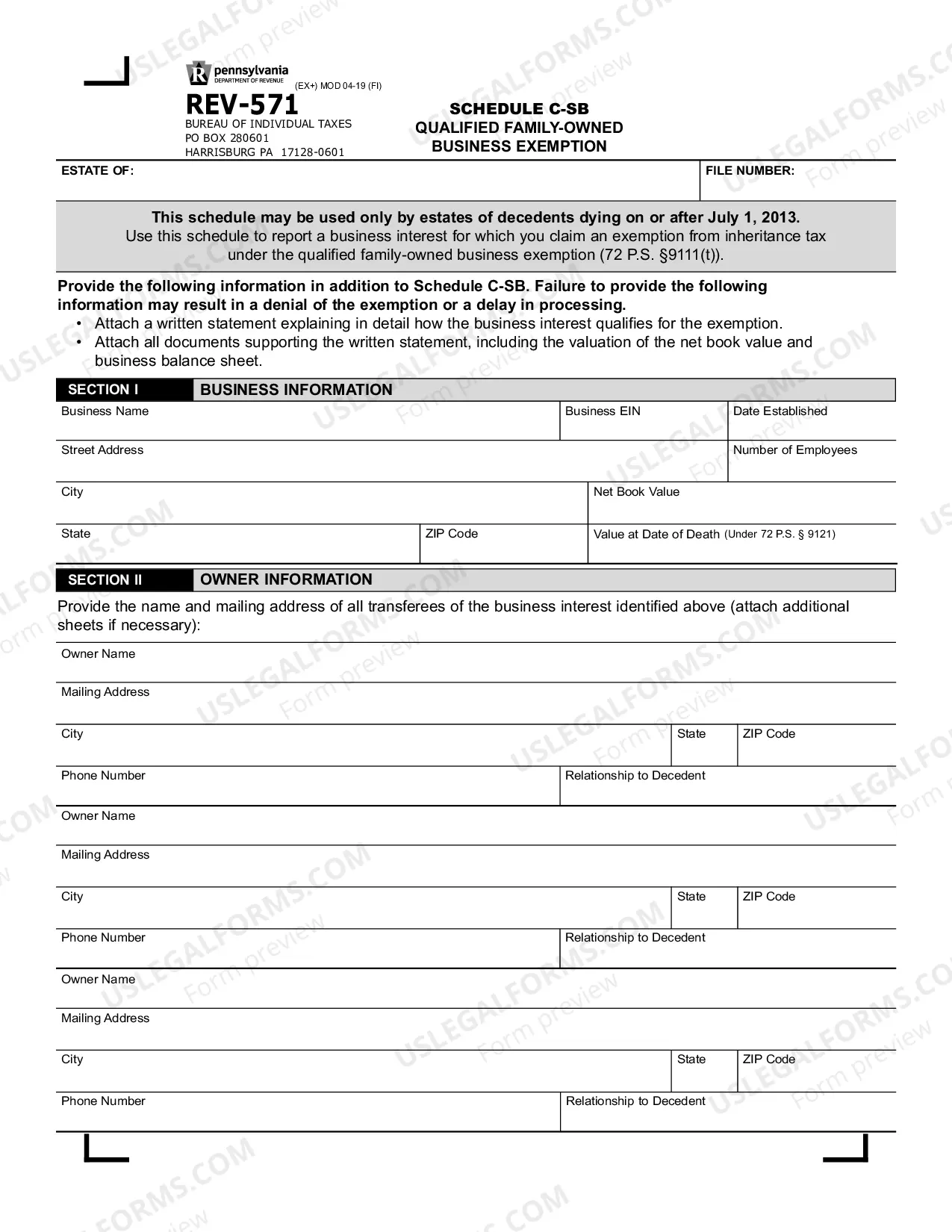

The exemption is limited to ?qualified family-owned business interests?, defined as having fewer than 50 full-time equivalent employees, a net book value of assets less than $5 million dollars, and being in existence for at least five years at the decedent's date of death.

Key takeaways. As of January 1, 2026, the current lifetime estate and gift tax exemption of $12.06 million for 2022 ($12.92 million for 2023) will be cut in half, and adjusted for inflation.

Effective January 1, 2023, the federal gift/estate tax exemption and GST tax exemption increased from $12,060,000 to $12,920,000 (an $860,000 increase). 1 The federal annual exclusion amount also increased from $16,000 to $17,000.

Applying the most recent 8.5% inflation rate, the year 2024 federal estate and gift tax exemption becomes roughly $14,197,333 per person. This becomes $28,394,666 for a married couple.

For 2023, the gift and estate tax exemption is $12.92 million ($25.84 million per married couple). Lifetime gifts that do not qualify for the annual exclusion described above will reduce the amount of gift and estate tax exemption available at death.

PURPOSE OF SCHEDULE Use REV-571, Schedule C-SB to report a business interest for which you claim an exemption from inheritance tax under the qualified family-owned business exemption. NOTE: REV-571, Schedule C-SB must accompany the return if a business interest qualifies for the family-owned business exemption.

Lifetime IRS Gift Tax Exemption Also for 2023, the IRS allows a person to give away up to $12.92 million in assets or property over the course of their lifetime and/or as part of their estate.