Pennsylvania Satisfaction, Cancellation or Release of Mortgage Package

About this form package

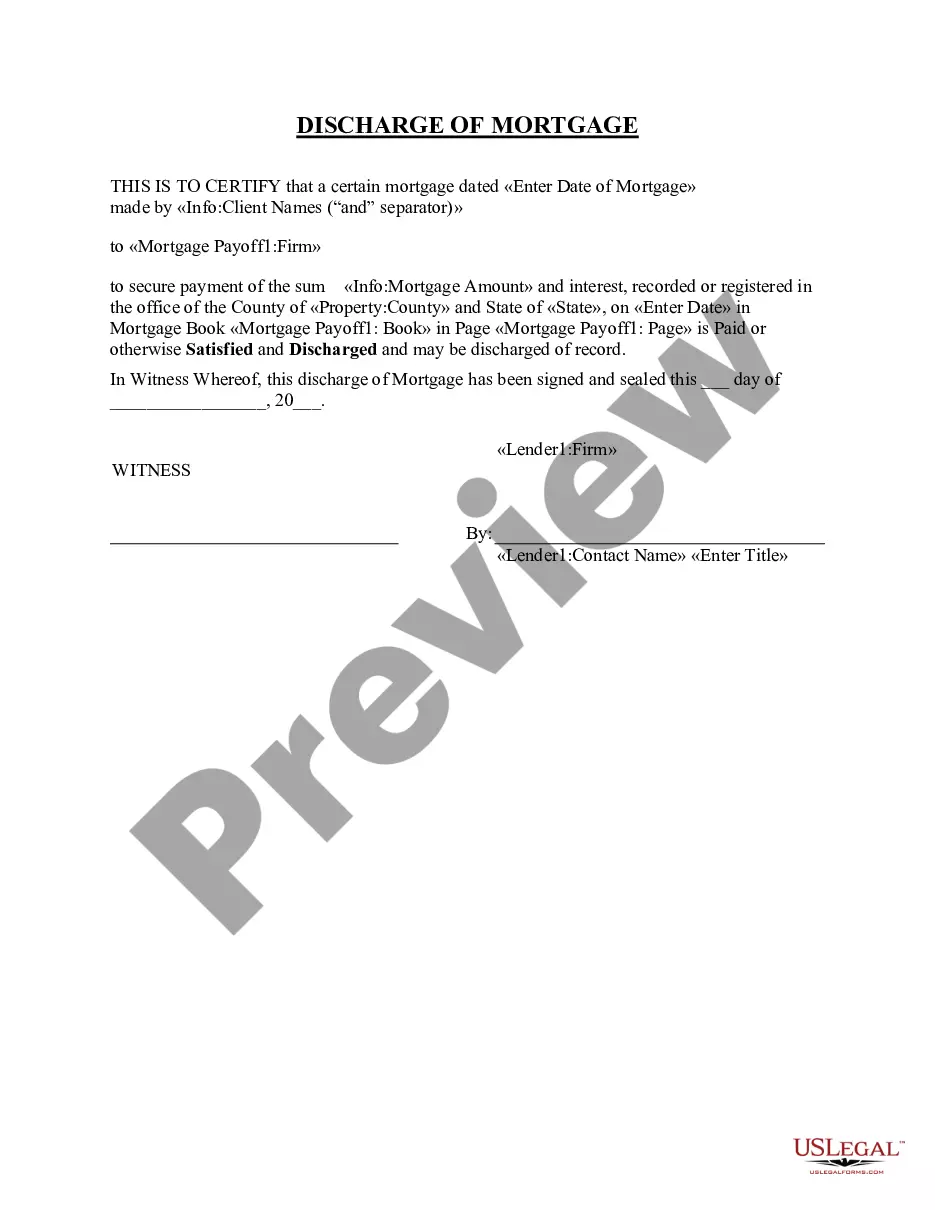

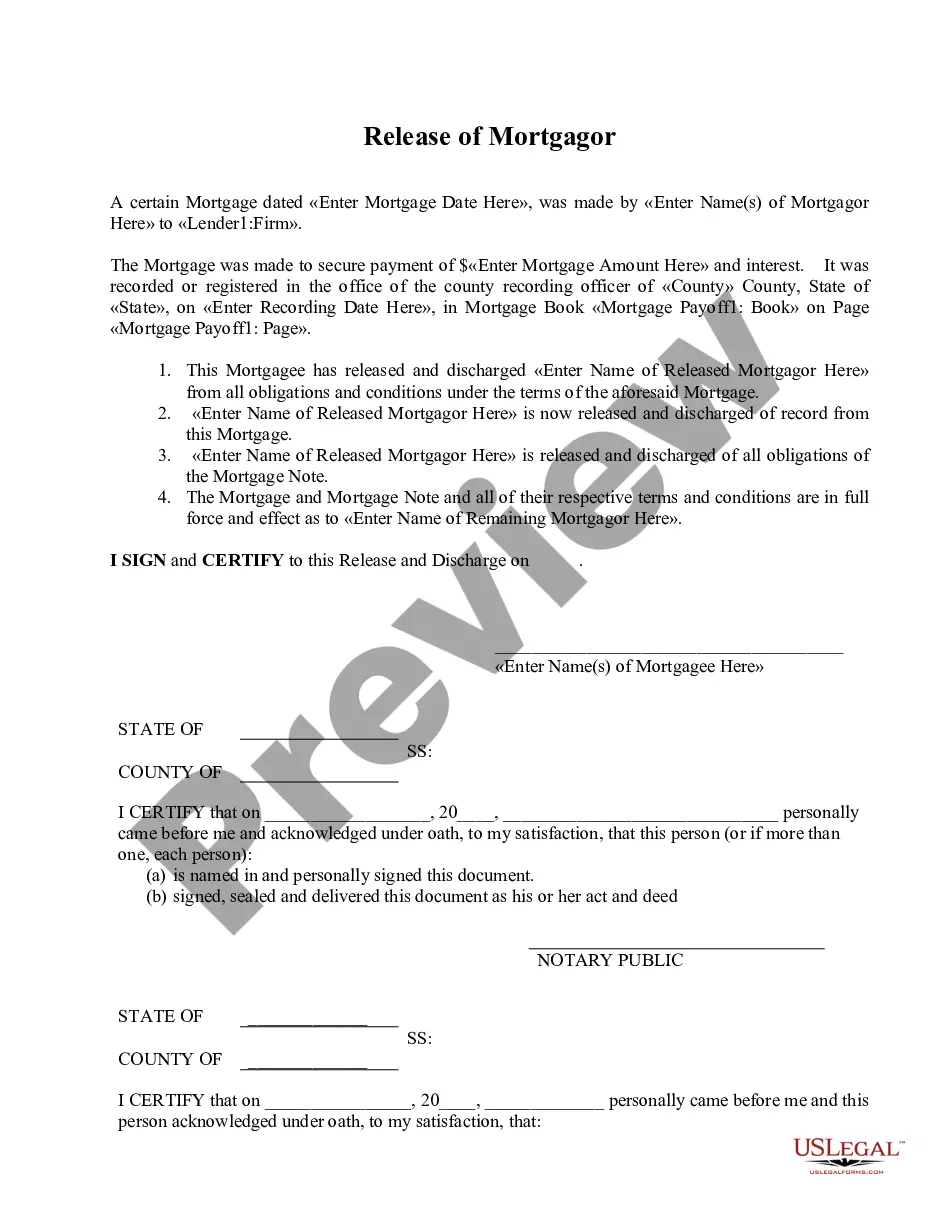

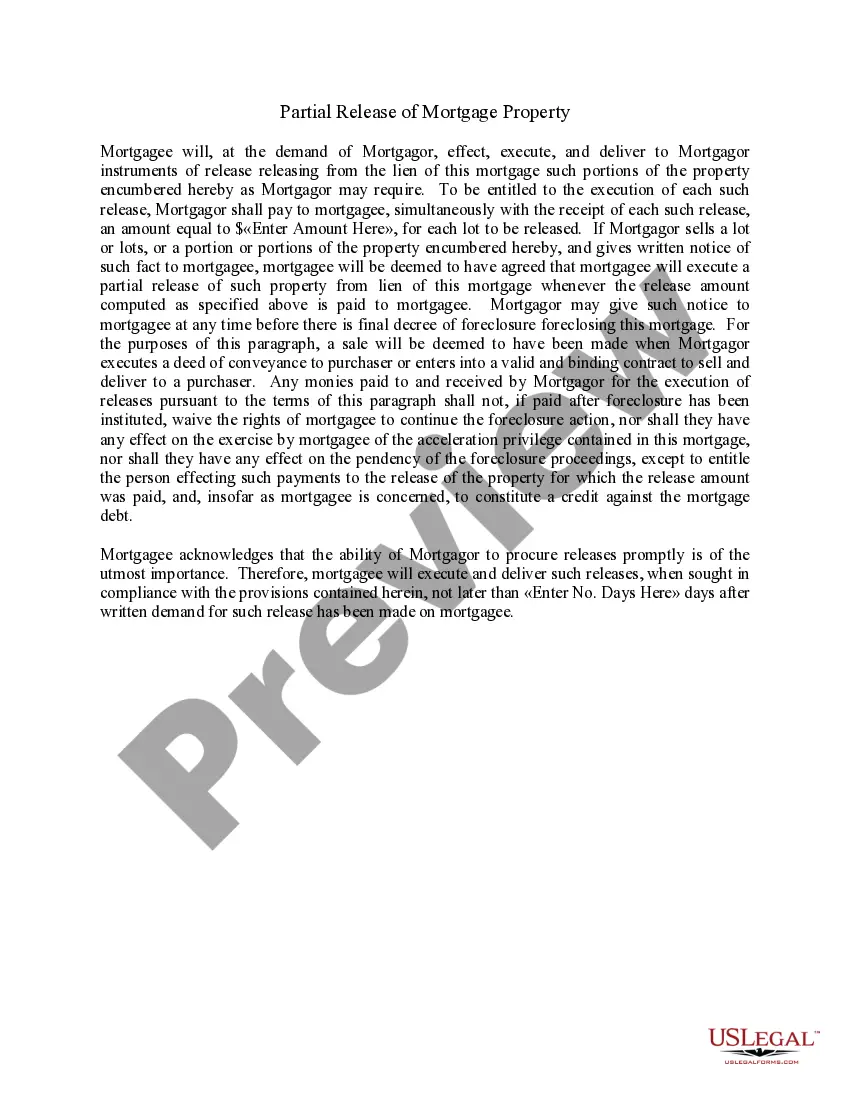

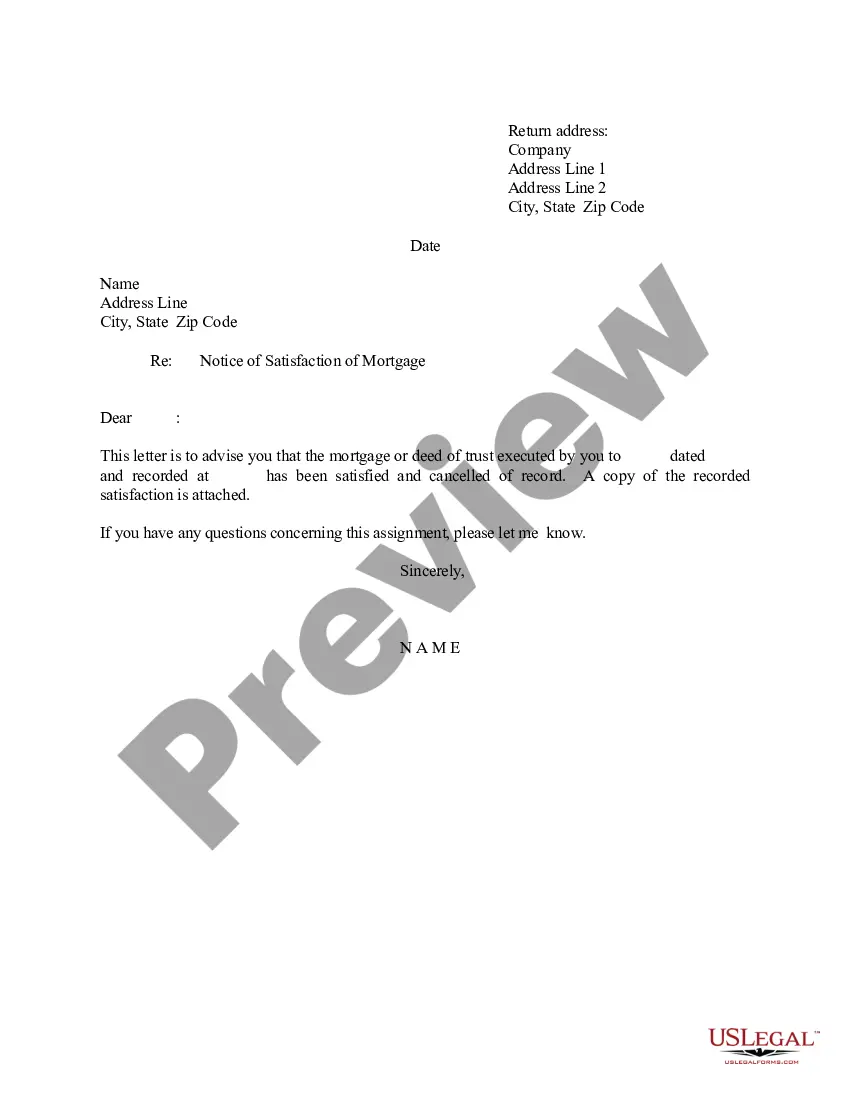

The Pennsylvania Satisfaction, Cancellation or Release of Mortgage Package includes the essential forms and letters necessary to release a mortgage in Pennsylvania. This package is designed to simplify the process of clearing a mortgage, allowing property owners to formally remove the obligation from their records. Unlike other legal packages, this one specifically focuses on mortgage satisfaction and complies with Pennsylvania laws, ensuring that all documents meet local requirements.

Documents contained in this package

When to use this form package

This form package is useful in the following situations:

- When a mortgage has been paid off and the borrower needs to confirm satisfaction.

- If the property owner wishes to release a deed of trust.

- When preparing to sell or transfer the property and ensuring that there are no outstanding mortgage claims.

Who should use this form package

- Property owners in Pennsylvania who have repaid their mortgage.

- Individuals or corporate lenders looking to release a mortgage.

- Real estate agents or attorneys assisting clients with mortgage releases.

Instructions for completing these forms

- Review each form included in the package to understand requirements.

- Identify the correct form based on whether the lender is a corporate entity or an individual.

- Complete the Satisfaction Piece of Mortgage or Letter of Notice to Borrower with accurate details.

- Sign all forms in the presence of a notary public if notarization is required.

- Submit the completed forms to the appropriate recording office as instructed.

Notarization guidance for this package

Notarization is required for one or more forms in this package. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to notarize the Satisfaction Piece of Mortgage as required by law.

- Not providing complete or accurate information in the forms, leading to potential rejections.

- Neglecting to send the recorded satisfaction to the borrower in a timely manner.

Advantages of online completion

- Convenient access to all necessary forms in one package.

- Edit and complete forms on your computer, saving time and ensuring accuracy.

- Reliably drafted by licensed attorneys, ensuring compliance with legal standards.

Looking for another form?

Form popularity

FAQ

Unless you're a cash buyer, no mortgage = no home purchase. And because the mortgage application process puts a borrower's finances under the microscope, it's not uncommon for buyers to have their financing fall through after they get the initial go-ahead from a lender.

While it's rare, the short answer is yes. After your loan has been deemed clear to close, your lender will update your credit and check your employment status one more time.Even if you left your job for another job with equal pay, your loan could still be denied, or delayed, depending on the type of loan you have.

The time it takes to close on a house, and get your mortgage loan application approved, usually runs anywhere from 30 50 days. Signing the paperwork on closing day can take up to an hour or more depending on whether there are any problems.

The lender has no right of rescission. Once you have signed loan documents, you have entered into a binding contract, and the lender is legally bound to honor those signed documents. The right of rescission is a separate form giving you three days in which you can back out of the transaction without penalty.

1Take possession of all the papers.2Get an NOC.3Get your CIBIL report updated.4Get the lien withdrawn.5Get an encumbrance certificate.

When you close on your loan, the loan becomes final and the money is disbursed. When you close on your home, you become its legal owner. These two things usually happen at the same time. So on your closing date, your mortgage loan becomes final and you get the keys to your new home.

Buyers do not legally own their new property until their mortgage funds. Sellers have not legally sold their property until funding. Typically, this is not a problem since dry closings, by state practice or lender preference, are usually funded quickly, within 24 to 48 hours.

Until the lender tells you that you are "clear to close" you may have outstanding conditions to address, including a potential secondary credit review.Most but not all lenders check your credit a second time with a "soft credit inquiry", typically within seven days of the expected closing date of your mortgage.

Do not check up on your credit report. Do not open a new credit. Do not close any credit accounts. Do not quit your job. Do not add to your credit cards' credit limit. Do not cosign a loan with anyone.