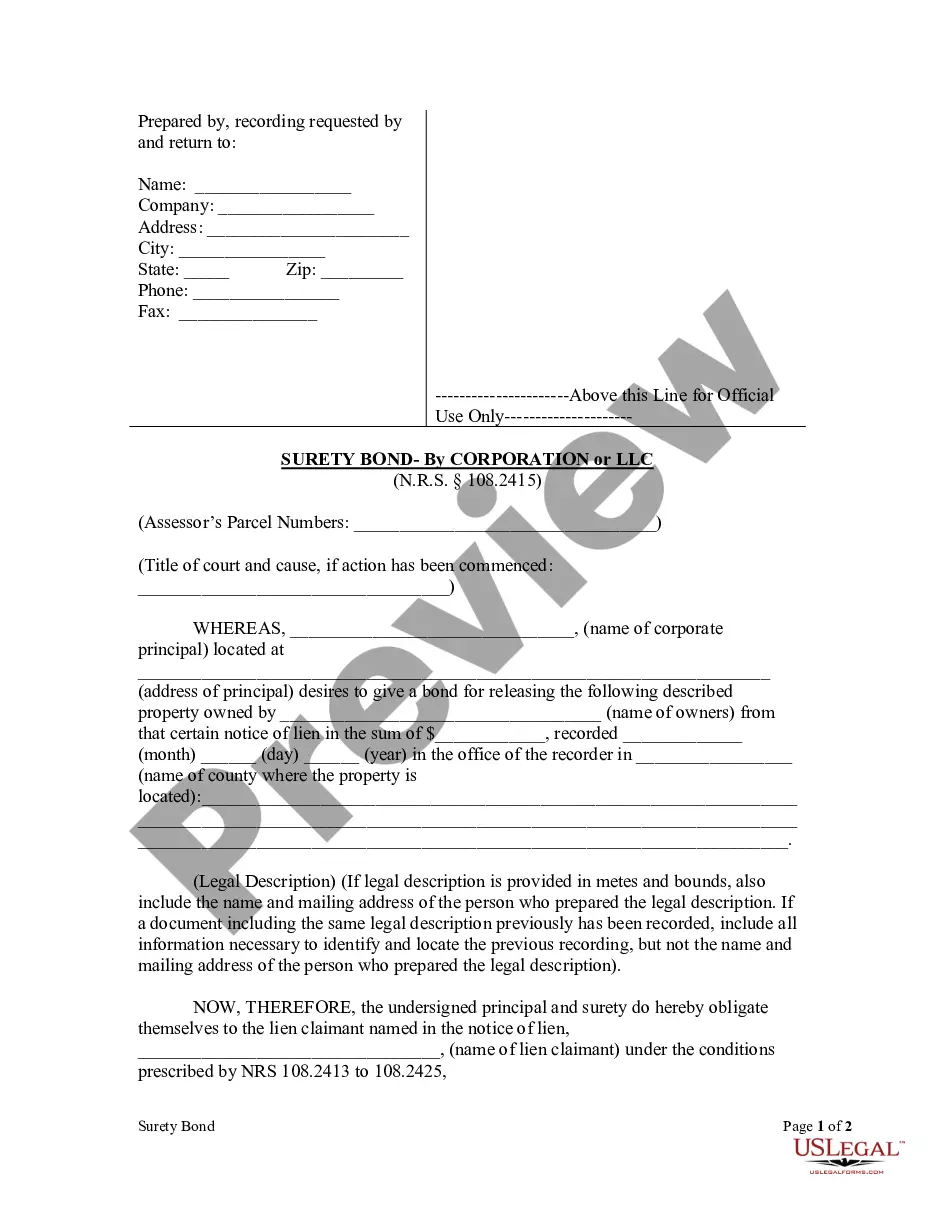

Nevada Surety Bond Form - Individual

Overview of this form

The Surety Bond Form - Individual is a legal document used to remove a mechanic's lien from a property by securing a bond. This bond typically amounts to one and one-half times the lien claim and is essential for property owners or principal contractors in Nevada. It serves to protect the interests of lien claimants while allowing the property owner to resolve disputes without liquidating the property. Unlike other forms of lien release, this surety bond involves a commitment from both the principal and the surety to uphold the bond's conditions.

Key parts of this document

- Principal information: Includes the name, company, address, and contact details of the principal providing the bond.

- Property details: Specifies the property being bonded, including ownership and legal description.

- Bond sum: Details the amount of the bond, typically one and one-half times the lien amount.

- Notary section: Requires notarization to validate the signatures on the bond.

- Surety information: Includes the surety corporation and its attorney in fact who executes the bond.

Situations where this form applies

This Surety Bond Form - Individual is necessary when a property owner or principal contractor wishes to lift a mechanic's lien from their property without having to immediately pay the claimed amount. This form is applicable in situations where disagreements over payment for work on the property have led to a lien being imposed and the owner seeks to preserve their right to contest the validity of the lien while offering a bond as security.

Who can use this document

- Property owners in Nevada facing a mechanic's lien on their property.

- Principal contractors who have been issued a lien by subcontractors or suppliers.

- Surety corporations providing bonds for the release of lien claims.

- Real estate professionals assisting clients in resolving liens.

How to prepare this document

- Identify the parties: Fill in the name and address of the principal providing the bond.

- Specify the property: Provide the legal description and ownership details of the property affected by the lien.

- Enter bond amount: Calculate and input the bond amount, which should equal one and one-half times the lien claim.

- Signatures: Ensure the principal and surety representatives sign the form and include their printed names.

- Notorization: Have the completed form notarized to validate the signatures.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately describe the property, which can lead to validation issues.

- Neglecting to obtain necessary signatures or failing to complete the notary section.

- Incorrectly calculating the bond amount based on the lien claim.

- Submitting the form without ensuring all required information is complete.

Why use this form online

- Convenience: Access and fill out the form at any time without needing to visit a legal office.

- Editability: Easily make changes as needed before finalizing the form.

- Reliability: Forms are created and reviewed by licensed attorneys to ensure compliance with current legal standards.

Looking for another form?

Form popularity

FAQ

Write the name of the obligor, or project owner, on the line preceded or followed by are held and firmly bonded to. Write the amount of money at issue in the bond on the line designated for the bond amount. Sign the bond in the presence of a notary public and have the bond notarized.

California requires qualifying individuals who are NOT owners of the business to purchase and file the $12,500 Bond of Qualifying Individual. To be considered an owner, the individual must own 10% or more of the business equity.

Insured are both forms of financial guarantee. They are designed to protect a person or a business in the event of something going wrong. However, they are not the same thing. Being bonded is not insurance.

A Bond of Qualifying Individual is required if the license is qualified by a Responsible Managing Employee (RME). A Bond of Qualifying Individual is required if the license is qualified by a Responsible Managing Officer (RMO) who does not own at least 10% of the voting stock of the corporation.

Being bonded means that a bonding company has secured money that is available to the consumer in the event they file a claim against the company. The secured money is in the control of the state, a bond, and not under the control of the company.

Individual sureties are natural persons as opposed to corporations and limited liability companies who offer to bind themselves on bid, performance, and payment bonds.

If your job requires working with a lot of cash or valuables, your employer may ask that you be bonded. Bonding is a type of insurance for the employer. It protects business owners from employee theft and also compensates the employer in cases of property loss caused by an employee.

You will need to be bonded if your state or municipality requires it. In addition, if your business frequently performs services in customer's homes or on the premises of other businesses, you should strongly consider getting bonded to protect your customers and your business's financial health.

Background Check A criminal history is a red flag for surety companies because it lessens a person's trustworthiness. Drug convictions, acts of violence and theft are all examples of criminal activity that can hurt your chances of getting bonded.