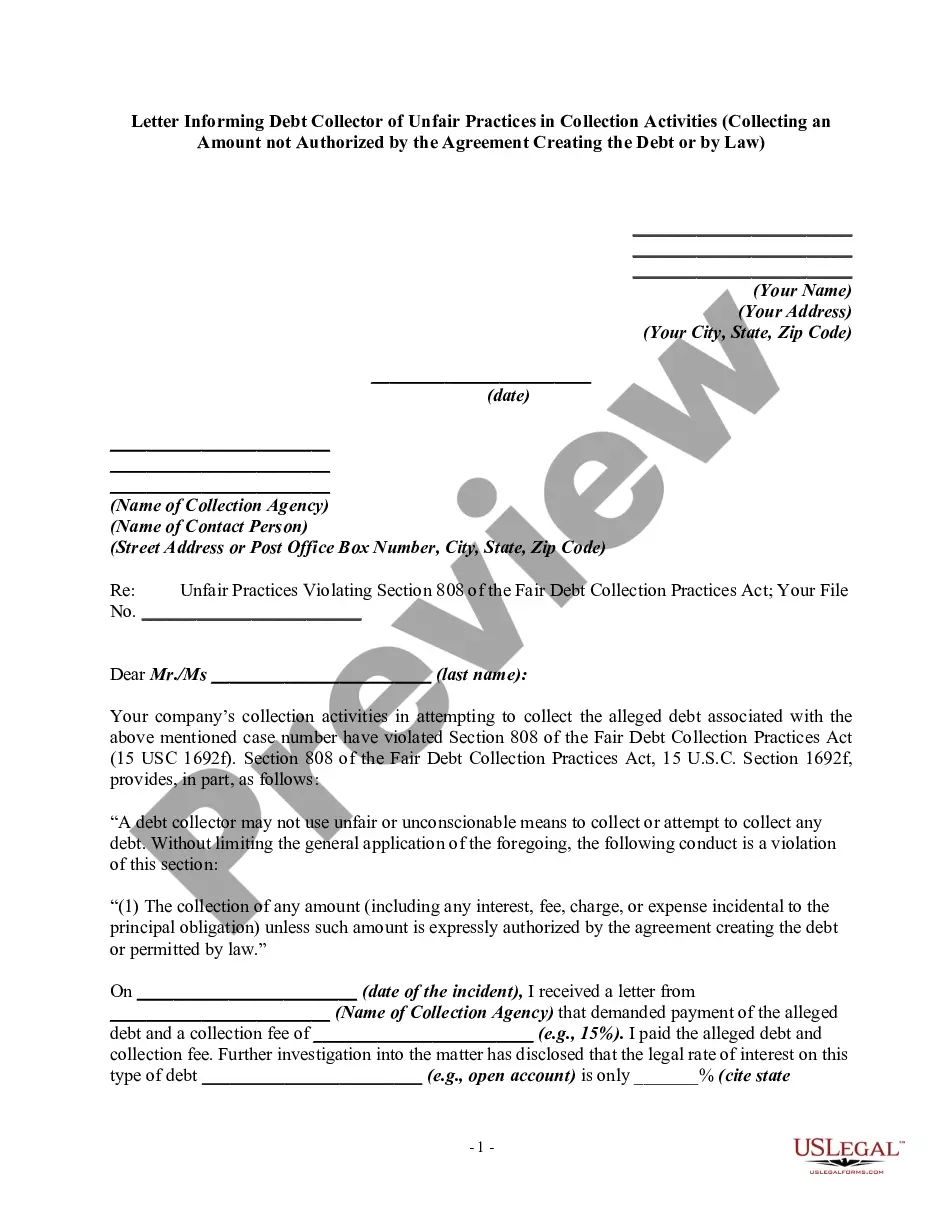

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

New Hampshire Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

If you need to finalize, download, or print legal document templates, utilize US Legal Forms, the largest assortment of legal forms available online.

Make the most of the site’s straightforward and convenient search to find the documents you require.

Various templates for businesses and personal needs are organized by categories and states, or keywords.

Step 4. After identifying the required form, select the Purchase now option. Choose your preferred pricing plan and enter your details to register for an account.

Step 5. Process the transaction. You can use your Visa or MasterCard or PayPal account to complete the purchase.

- Employ US Legal Forms to obtain the New Hampshire Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law with just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Download option to find the New Hampshire Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law.

- You can also access forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the steps outlined below.

- Step 1. Ensure you have selected the form for the correct state/country.

- Step 2. Utilize the Preview option to examine the content of the form. Be sure to read the explanation.

- Step 3. If you are not satisfied with the form, use the Search box at the top of the screen to find alternative versions in the legal form format.

Form popularity

FAQ

If the FDCPA is violated, the debtor can sue the debt collection company as well as the individual debt collector for damages and attorney fees.

If you don't pay a collection agency, the agency will send the matter back to the original creditor unless the collection agency owns the debt. If the collection agency owns the debt, they may send the matter to another collection agency. Often, the collection agency or the original creditor will sue you.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

Not being able to meet payment obligations can make anyone feel anxious and worried, but in most cases, you won't have to worry about serving jail time if you are unable to pay off your debts. You cannot be arrested or go to jail simply for being past-due on credit card debt or student loan debt, for instance.

Remember, debts that cannot be enforced are only protected from court action; the bad debt is still going on your credit report. If you want to settle the debt, you have to negotiate. If the collector cannot produce the agreement, you don't have to pay your dues.

One is to report them to the Financial Consumer Protection Department of the BSP (i.e. email consumeraffairs@bsp.gov.ph or call 632-708-7087). Be sure to document all communications with your debt collectors including text messages and e-mails. If you can, record your conversation with their consent.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

If a creditor waits too long to take court action, the debt will become 'unenforceable' or statute barred. This means the debt still exists but the law (statute) can be used to prevent (bar) the creditor from getting a court judgment or order to recover it.

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

Yes, but the collector must first sue you to get a court order called a garnishment that says it can take money from your paycheck to pay your debts. A collector also can seek a court order to take money from your bank account.