The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

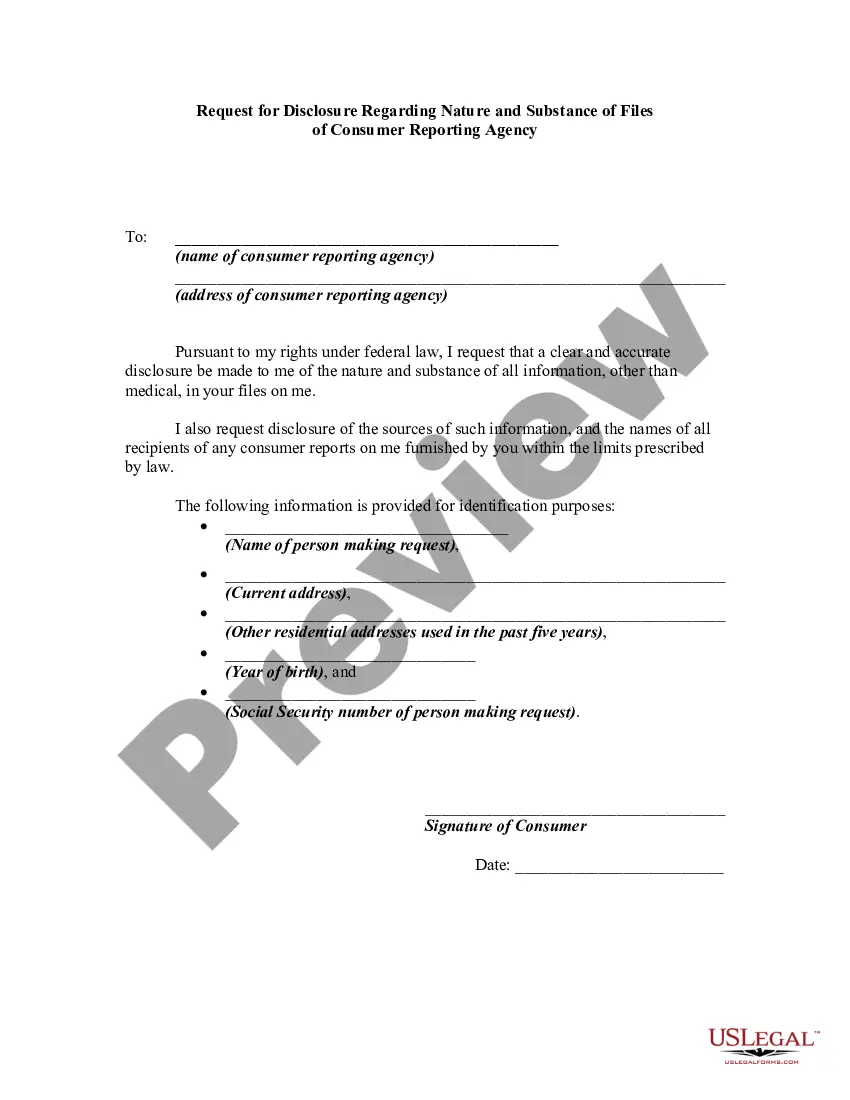

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

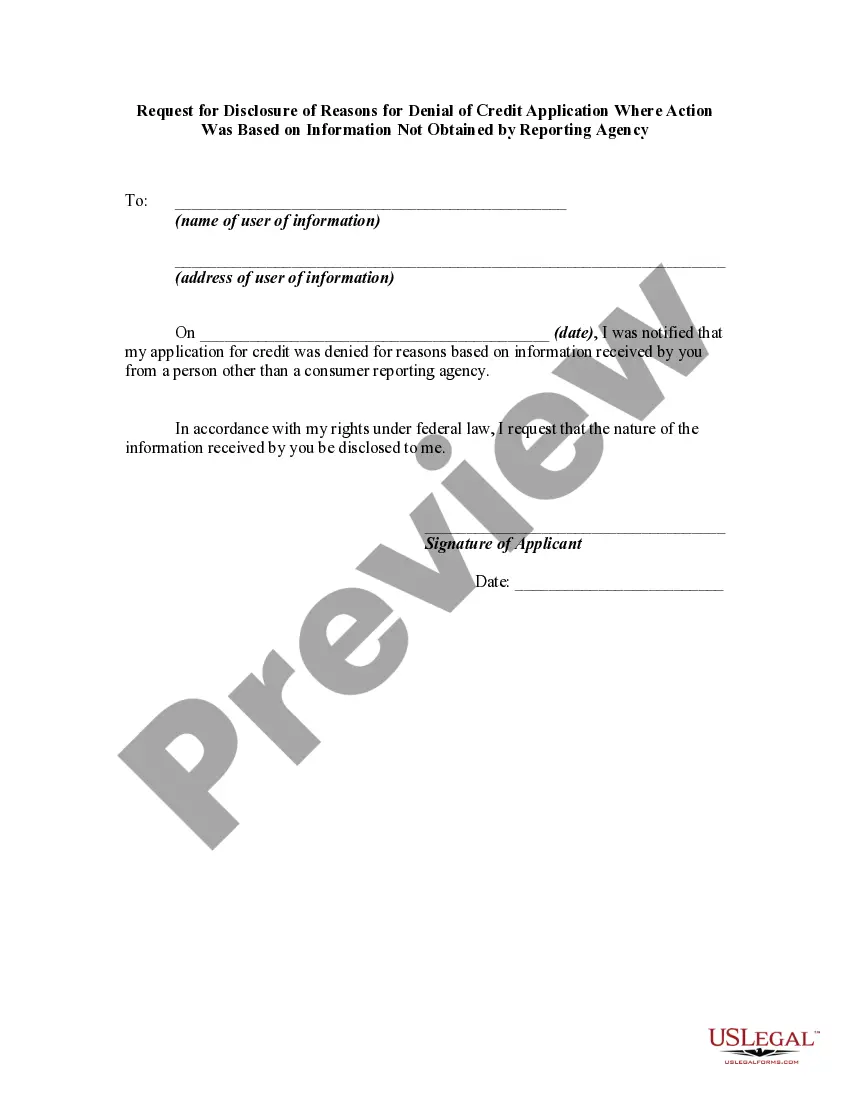

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

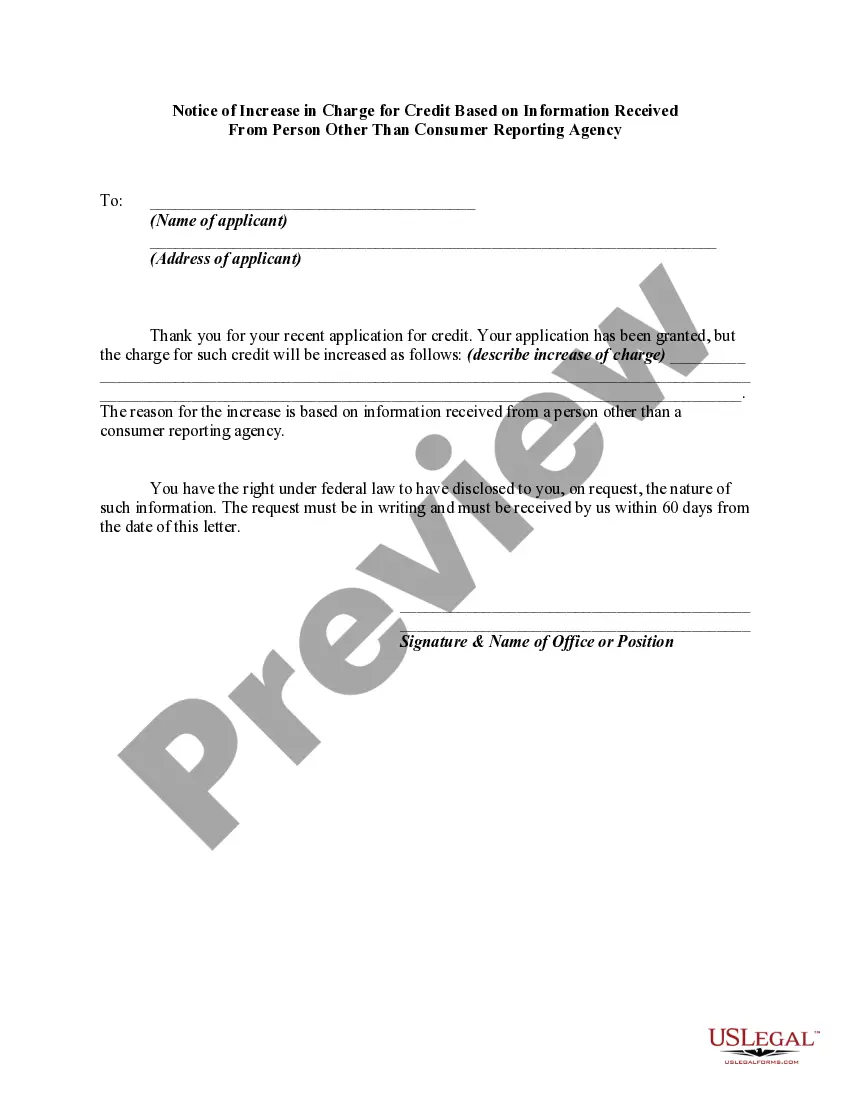

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

New Hampshire Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Increasing Charge For Credit Regarding Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

US Legal Forms - among the largest libraries of legitimate varieties in the USA - provides a wide array of legitimate record themes you can acquire or print. Making use of the site, you can find a huge number of varieties for company and person reasons, sorted by groups, suggests, or key phrases.You can find the most recent models of varieties much like the New Hampshire Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency in seconds.

If you currently have a membership, log in and acquire New Hampshire Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency in the US Legal Forms library. The Acquire switch will appear on every single kind you see. You get access to all earlier delivered electronically varieties from the My Forms tab of your respective bank account.

If you wish to use US Legal Forms the first time, listed below are basic recommendations to get you started out:

- Be sure you have chosen the best kind to your town/area. Click on the Review switch to analyze the form`s information. Browse the kind explanation to actually have selected the correct kind.

- If the kind does not satisfy your requirements, make use of the Look for area on top of the display screen to get the one which does.

- If you are satisfied with the shape, validate your choice by simply clicking the Purchase now switch. Then, opt for the rates prepare you want and offer your references to sign up on an bank account.

- Procedure the deal. Make use of your charge card or PayPal bank account to finish the deal.

- Choose the formatting and acquire the shape on your device.

- Make modifications. Complete, change and print and sign the delivered electronically New Hampshire Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency.

Every single design you included in your money lacks an expiration day and is also your own property for a long time. So, if you would like acquire or print an additional backup, just proceed to the My Forms area and then click in the kind you will need.

Obtain access to the New Hampshire Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency with US Legal Forms, probably the most substantial library of legitimate record themes. Use a huge number of specialist and status-certain themes that fulfill your organization or person needs and requirements.

Form popularity

FAQ

For employers, it is a big picture snapshot of how a potential candidate handles their responsibilities. "Credit reports indicate whether or not you're responsible," financial expert John Ulzheimer, formerly of FICO and Equifax, tells Select. "And, they also indicate if you're in financial distress.

Lenders may use your credit report information to decide whether you can get a loan and the terms you get for a loan (for example, the interest rate they will charge you). Insurance companies may use the information to decide whether you can get insurance and to set the rates you will pay.

Your credit report will allow the lender or service provider to assess your application in a fair and objective manner. In general, people with good track records of payment may receive lower interest rates or more services than those with poor payment track records.

Along with many other pieces of information, potential lenders, and creditors ? including credit card companies, mortgage lenders and auto lenders ? may use your credit scores and credit history to help make lending decisions. These companies want to know how likely you are to pay the money they lend back as agreed.

It also includes personal identifying information that helps to verify that the information in the report is yours. Your credit report does not include your marital status, medical information, buying habits or transactional data, income, bank account balances, criminal records or level of education.

The Dodd-Frank Act also amended FCRA to require disclosure of a credit score and related information when a credit score is used in taking an adverse action or in risk-based pricing. On December 21, 2011, CFPB restated FCRA regulations, named Regulation V (12 CFR Part 1022).

While the general public can't see your credit report, some groups have legal access to that personal information. Those groups include lenders, creditors, landlords, employers, insurance companies, government agencies and utility providers.

If the disputed information is wrong or can't be verified, the company is required by law to delete or change the information. It also has to notify all of the credit reporting companies to which it provided the wrong information, so the credit reporting companies can update their files with the correct information.